ASML Holding (ASML) has a monopoly in the most critical part of chip manufacturing, but that strength is already reflected in the stock. The company supplies the extreme ultraviolet (EUV) and deep ultraviolet (DUV) lithography equipment used to manufacture the advanced semiconductors that power artificial intelligence (AI), cloud, and computing workloads. This gives it a position few can challenge. That dominance justifies a premium, but with the stock trading at a rich revenue multiple, much of the semiconductor supercycle is already reflected in the price.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

ASML stock rallied recently, fueled by an AI-driven supercycle and heavy investments in the memory sector. I have a neutral view, as current pricing assumes a multi-year wafer-fab-equipment (WFE) upcycle, with little margin for cyclical pauses, project delays, or geopolitical setbacks.

ASML Holding’s EUV Monopoly Is Powerful

ASML Holding’s competitive moat lies in selling advanced EUV and DUV systems, along with service and upgrades, to top-tier logic and memory companies, such as Taiwan Semiconductor Manufacturing Company Limited (TSMC) (TSM) and Intel (INTC). That monopoly has translated into rising revenue and strong margins, with ASML generating about €32.7 billion, or approximately $36 billion, in total net sales in 2025. It now forecasts sales between €36 billion and €40 billion, roughly $39–44 billion in 2026, higher than prior indications, signaling confidence in demand.

However, EUV’s strategic importance does not shield ASML Holding from semiconductor cycles. Management has indicated plans to produce at least 60 Low Numerical Aperture (NA) EUV systems in 2026 for cutting-edge nodes, with at least 80 Low NA EUV units targeted for 2027, provided customer demand and execution are met. Any delay in tool deployment could make orders shift over time, which matters for a stock trading at a supercycle multiple.

Bookings, Backlogs, and Customer Concentration

Recent results show solid but not explosive bookings relative to the surge in the share price. ASML reported Q3 2025 net sales of €7.5 billion, or about $8.8–8.9 billion, with net bookings of about €5.4 billion, or around $6.3–6.4 billion, including roughly €3.6 billion or about $4.2–4.3 billion in EUV. In Q1 2026, revenue increased to €8.8 billion, or around $10.3–10.4 billion, suggesting that customers are positioning for higher volumes even as near-term bookings remain fairly unstable.

Customer concentration heightens risk, as the bulk of demand for leading-edge tools comes from a handful of mega-customers, including TSMC, Samsung (SSNLF), and Intel. Each of these companies faces its own strategic and macro uncertainties. If any of these giants readjust their capex, ASML’s bookings and backlog trajectory can change significantly.

High-Quality Growth at a Supercycle Multiple

ASML is valued as a long-term growth stock, trading at roughly 46x trailing earnings and 13x EV/revenue, with valuations reflecting a premium compared to regular cyclical equipment manufacturers. Financial models suggest roughly 30% upside, prompted by sustained growth in WFE spending.

High WFE multiples are driven by strong AI demand, high-bandwidth memory, and geopolitical reshoring of fabs in the U.S. and Europe. Yet, these valuations face risks from a likely cyclical digestion. While a supercycle in AI demand remains likely, historical trends suggest the path for high-multiple stocks like ASML could be more volatile than their current pricing implies.

The Geopolitics Concern

ASML Holding’s DUV systems have historically seen strong demand from Chinese fabs upgrading mature-node capacity in response to global supply chain shifts. Yet, China’s share of ASML revenue fell from 36% in Q4 2025 to 19% in Q1 2026, with management guiding an average of 20% of total sales for 2026.

At the same time, strong AI-driven demand in other regions, such as the U.S., Europe, and Asia, alongside continued mature-node investments, is expected to offset China-related constraints over time. However, this geographic shift introduces new operational risks. As major foundries like TSMC, Samsung, and Intel expand production into Arizona, Texas, and Germany to reduce regional dependence, they face higher construction costs and a more fragmented talent pool.

Nevertheless, varying government subsidies and construction delays can stall these projects. Since ASML’s EUV systems are so complex, any delay in construction affects ASML’s ability to get paid. While the big picture for AI looks good, investors face a bumpy ride because politics, not just market demand, now influences the timeline.

What Is the Market’s View?

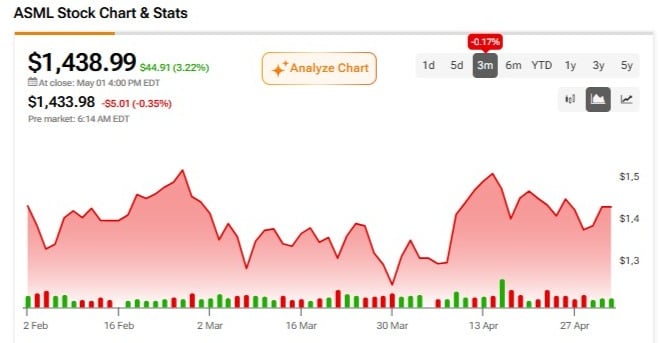

On TipRanks, ASML Holding has a Strong Buy consensus rating. Based on five Wall Street analysts’ ratings over the past three months, the breakdown is five Buys, 0 Holds, and 0 Sells. The average 12-month ASML price target on TipRanks is $1,791.40, implying a 24.49% upside from the last price of $1,438.99.

The highest price target is $1,971.00, while the lowest is $ 1,650.00. Broader data on TipRanks also assigns ASML an outperform Smart Score of 10, emphasizing that quantitative and qualitative signals line up in the stock’s favor.

Final Thoughts

ASML Holding is a crucial pillar of the global semiconductor industry because it holds a near-monopoly on the EUV technology required to manufacture advanced AI chips. Because of this unique position, the company is likely to see its profits grow steadily over the long term as it remains indispensable to the entire supply chain.

However, investors are paying a high premium for ASML stock, leaving little room for error if the company faces construction delays, political issues, or a temporary industry slowdown. While long-term investors may still see gains, those buying now should recognize that much of the future growth is already priced in, making patience through pullbacks more prudent than chasing rallies.