Super Micro Computer (NASDAQ:SMCI) is grabbing the headlines on Wednesday, and this time it is for all the right reasons. The stock is up by 15% following the release of the AI server maker’s fiscal third quarter results.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company has been a controversial name on Wall Street largely due to ongoing corporate governance issues. Additionally, in March, US prosecutors charged co-founder Yih-Shyan “Wally” Liaw with allegedly diverting billions of dollars’ worth of Nvidia-based servers to China in violation of US export control laws. However, the stock now appears positioned to deliver its strongest day in the last 15 months.

In the quarter, revenue came in at $10.2 billion, up 121.7% year-over-year, but falling shy of expectations by $2.25 billion. Management put the shortfall down to customers not yet having the necessary power and networking infrastructure in place for cloud deployments. Despite this, the company remains confident in a rapid ramp in rack-scale AI solutions and ongoing momentum in AI infrastructure demand.

The miss does not seem to have bothered investors who saw plenty else to like. Adjusted gross margin reached 10.1%, exceeding analysts’ expectations of 6.75%. Gross margin stood at 9.9%, compared to 6.3% in 2Q26 and 9.6% in 3Q25. At the bottom line, the company delivered an adj. EPS of $0.84, surpassing estimates by $0.22.

For the fourth quarter, the company guided for net sales in the range of $11 billion to $12.5 billion, at the midpoint above the consensus estimate of $11.16 billion.

Scanning the results, Rosenblatt’s Kevin Cassidy, an analyst ranked among the top 1% on Wall Street, notes that although revenue has increased by more than 2.5x over the past two years, gross profit has risen by only about 60%, thereby “creating a disparity between the company’s revenue growth profile and its recent stock performance.”

But looking ahead, management anticipates its “One-Stop Shop” DCBBS (Data Center Building Block Solutions) to contribute more than 20% of gross profit over the long term by enabling faster and more reliable AI factory deployments. Cassidy believes a higher contribution from DCBBS, along with a growing mix of software and services, should support gross margin expansion and improve visibility into profitability. “Consequently,” the 5-star analyst said, “we see a clear path for gross margins to climb back above 10%, returning toward the low-teens average seen from FY22–FY24.”

On the legal side, the stock has now recovered its losses following the U.S. Attorney’s indictment related to alleged export control violations. While legal affairs could weigh on sentiment in the near term, Cassidy thinks downside risk “appears limited” as the company plans to file its 10-Q and does not expect any financial restatements.

All told, driven by SMCI’s “technology leadership, robust order backlog, access to the AI supply chain, and the market’s insatiable demand for AI compute,” Cassidy reiterated a Buy rating on the shares and raised his price target to $40 (from $32), implying the stock will gain 24% in the months ahead. (To watch Cassidy’s track record, click here)

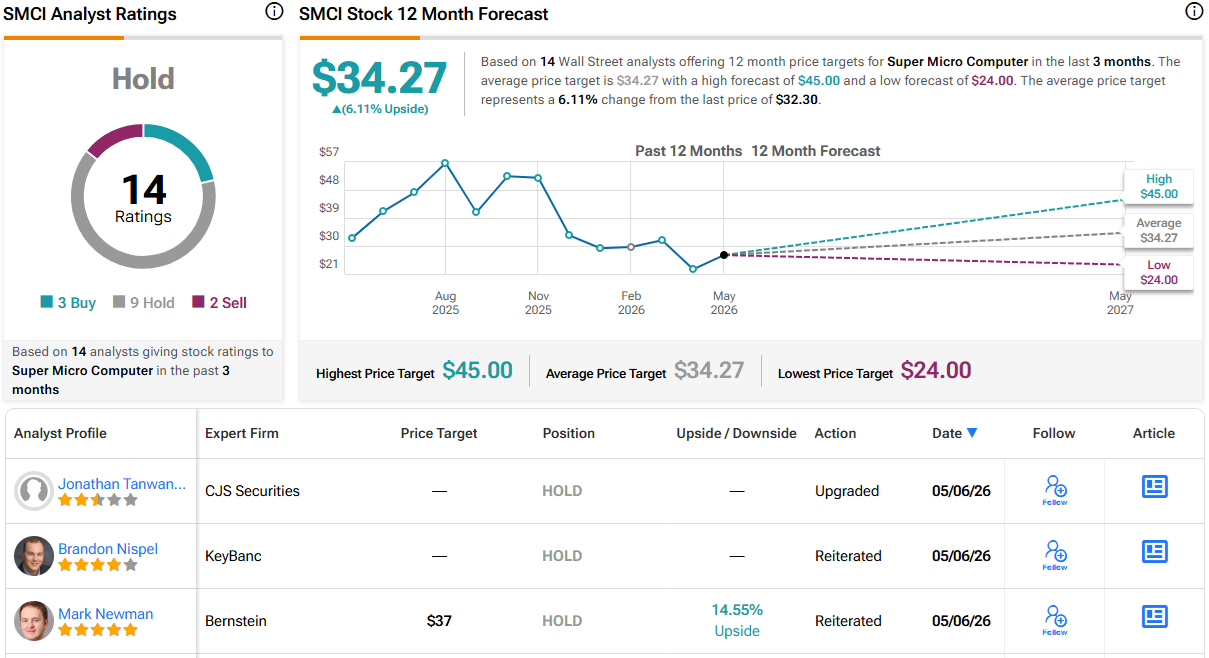

2 other analysts are bullish on SMCI’s prospects, yet with an additional 9 Holds and 2 Sells, the analyst consensus rates the stock a Hold. The average target clocks in at $34.27, making room for one-year gains of 6%. (See SMCI stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.