It’s another day of huge gains for Intel (NASDAQ:INTC), with shares up by 13% in Tuesday’s session, sending the stock to a new all-time high.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The latest uptick came off the back of reports the company has been in discussions with Apple about producing chips for its devices. According to Bloomberg, Apple has held early talks with both Intel and Samsung regarding the manufacture of primary processors for U.S. devices.

While the talks are still preliminary and don’t represent confirmed orders, if these discussions lead to an agreement, it would give Apple an additional supplier alongside its long-standing relationship with Taiwanese giant TSMC. A potential partnership with Intel would represent a significant breakthrough for the US chipmaker in the AI landscape. Although TSMC continues to lead the industry, securing even a small portion of Apple’s leading-edge demand could materially improve Intel’s foundry economics.

Tuesday’s gains represent another leg up in what has been an astounding run. Intel stock has now surged by 194% year-to-date, with the shares gathering steam following the company’s recent Q1 results and guide, which exceeded Street expectations.

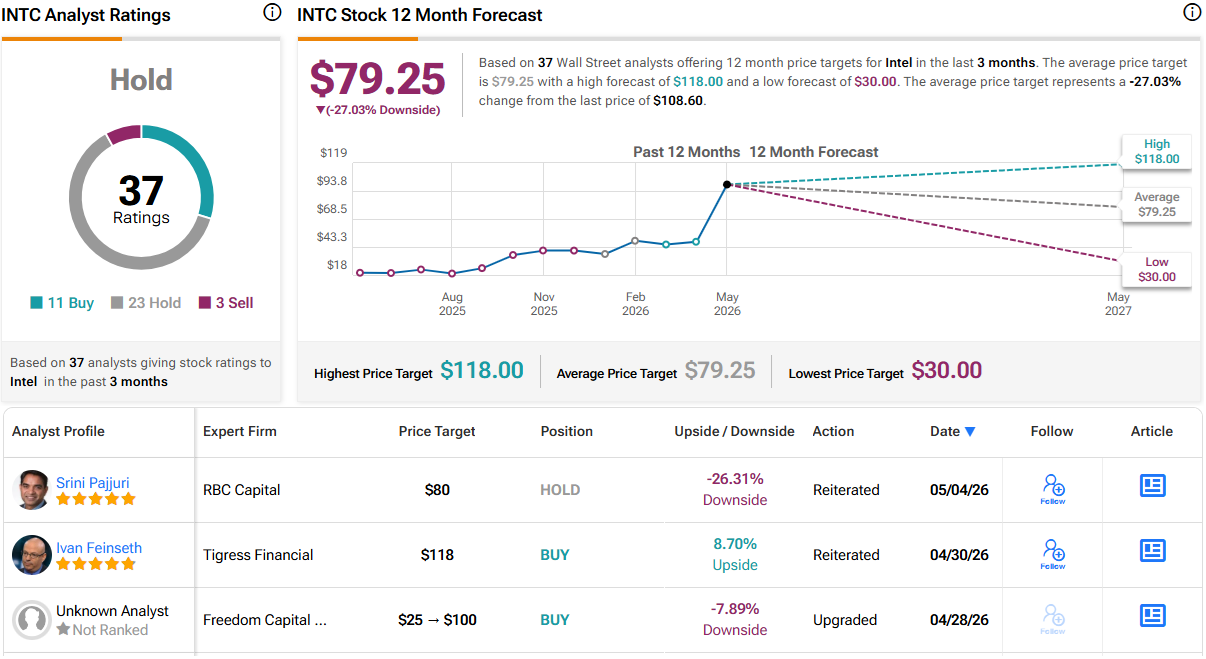

Against this backdrop of bullish sentiment, RBC’s Srini Pajjuri, an analyst ranked among the top 2% on Wall Street, points to highlights from a recent investor call with Intel’s CVP of IR, John Pitzer.

The company expects to see strong, broad-based demand for server CPUs continuing throughout the year, with product mix “driving further ASP tailwinds.” CPU density is also “increasing on a secular basis,” boosted by Agentic AI workloads and distributed inferencing. Beyond its x86 business, Intel is targeting additional upside through ASICs, its foundry services, and advanced packaging.

Specifically on the latter, advanced packaging is increasingly viewed as a “multi-billion dollar opportunity,” with revenue expected to begin ramping in the second half of 2027, potentially including contributions from Alphabet. In the Client business, management remains upbeat on the second half of 2026 despite a softer PC market, helped by relatively lean customer inventory levels. That said, gross margin commentary was more cautious, reflecting continued pressure from rising component costs.

All told, while Pajjuri liked what he heard, he’s not getting on board the Intel train just yet, noting: “We walked away comfortable with Intel’s near-term prospects but maintain Sector Perform due to valuation.”

That Sector Perform (i.e., Neutral) rating is backed by a price target of $80, suggesting the stock is now overvalued by 26%. (To watch Pajjuri’s track record, click here)

Pajjuri’s objective closely matches the Street’s average price target, which lands at $79.25, a figure pointing toward 12-month losses of 27%. On the rating front, based on a mix of 23 Holds, 11 Buys and 3 Sells, the analyst consensus rates the stock a Hold. (See Intel stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.