When Meta needed to build out its AI infrastructure at an unprecedented scale, it didn’t turn to the traditional giants of the tech world – it chose Arista Networks (ANET). The company’s journey from a networking upstart to an AI infrastructure powerhouse tells a compelling story about where the real value lies in the artificial intelligence revolution. Even after an 83% surge in the last year, I am bullish on ANET stock as I believe there is still a long way to go before shares of the company reach fair value.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Arista Networks Is Dominating

Over the last decade or so, I’ve watched Arista methodically dismantle Cisco’s (CSCO) dominance in high-speed networking. The numbers tell the story: from a modest 3.5% market share in 2012, Arista now commands 33.2% of the high-speed networking market. Even more telling, they’ve captured 45% of the crucial 100G/200G/400G switch port segment, where AI workloads demand maximum performance. Cisco, the former giant, has seen its share in this vital segment shrink to just 20%.

With this sector only likely to grow as the adoption and sophistication of these systems build out over time, the future looks bright for the sector, but I’d say especially so for Arista. However, growing market share isn’t just about taking business from competitors. A $70 billion total addressable market (TAM) by 2028 shows how ANET is expanding and reshaping the entire industry.

Recent releases from Arista underscore the scale of this transformation, with 54 new platforms launched, including ground-breaking AI networking solutions, 800G optics, and advanced WAN routing systems. Six major software releases also delivered over 600 new features. What makes the story particularly compelling from my perspective is how the company has become indispensable to the world’s largest technology companies. Most notably, they’ve done so while maintaining independence and avoiding over-concentration.

Arista Reporting Impressive Financials

I’m encouraged to see the company’s Q3 2024 results validate my bullishness. Revenues climbed 20% since last year to $1.8 billion. More impressively, it is doing so with industry-leading 64.6% gross margins and 49.1% operating margins.

But what particularly excites me is Arista’s diversification. Its revenue mix shows a thoughtful balance of 40-45% coming from Cloud and AI titans, 35-39% from enterprise and financial sectors, and 20-25% from service providers and tier-2 cloud companies. I think the enterprise opportunities are particularly compelling when considering that Arista has penetrated only 20% of Fortune 500 companies – representing an enormous untapped market.

Geographically, while the U.S. market clearly dominates with 81.7% of revenue, its growing presence in EMEA (10.6%) and APAC (7.7%) presents major opportunities as AI technology continues to grow around the world.

I See Plenty of Potential Ahead for Arista

Looking ahead, I see two massive growth catalysts for Arista. First, its campus networking initiative is projecting $750 million in revenue by 2025. Interestingly, Gartner recently recognized Arista as a Customers’ Choice in Enterprise Wired and Wireless LAN Infrastructure, which validates its progress in this segment. Second, its AI back-end networking opportunity, also targeting $750 million in revenue by 2025, leverages the firm’s leading position in high-performance networking.

In addition, the firm’s forward guidance of 15-17% growth maintains a pattern of conservative targets that have been consistently exceeded. At the same time, the slight projected decline in margins to 43-44% also reflects investments in R&D (11-12% of revenue) used to maintain a technological edge.

Even ANET’s corporate governance impresses me. CEO Jayshree Ullal has reduced emissions by 60% in five years. In addition, the company’s board composition of 77% independents with 50% gender and ethnic diversity suggests forward-thinking management, making them a standout among Fortune 1000 companies with both a female CEO and CFO.

Identifying Risks for Arista Networks

While I am bullish on ANET stock, there are still risks that need to be considered. For starters, Cisco remains formidable with deep enterprise relationships. In addition, supply chains require constant management, and cloud provider spending can be lumpy. Nevertheless, operational metrics and consistent execution show Arista’s ability to navigate these challenges while maintaining industry-leading performance.

Furthermore, with a price-to-earnings (P/E) ratio of 48.8x, some would-be investors might see Arista shares as rather expensive. However, I see a company aggressively expanding the addressable market with technological leadership and consistent execution that justifies a premium valuation. To me, the shift towards 800G and accelerating infrastructure buildout should create the ideal conditions for growth.

Is ANET a Buy, According to Analysts

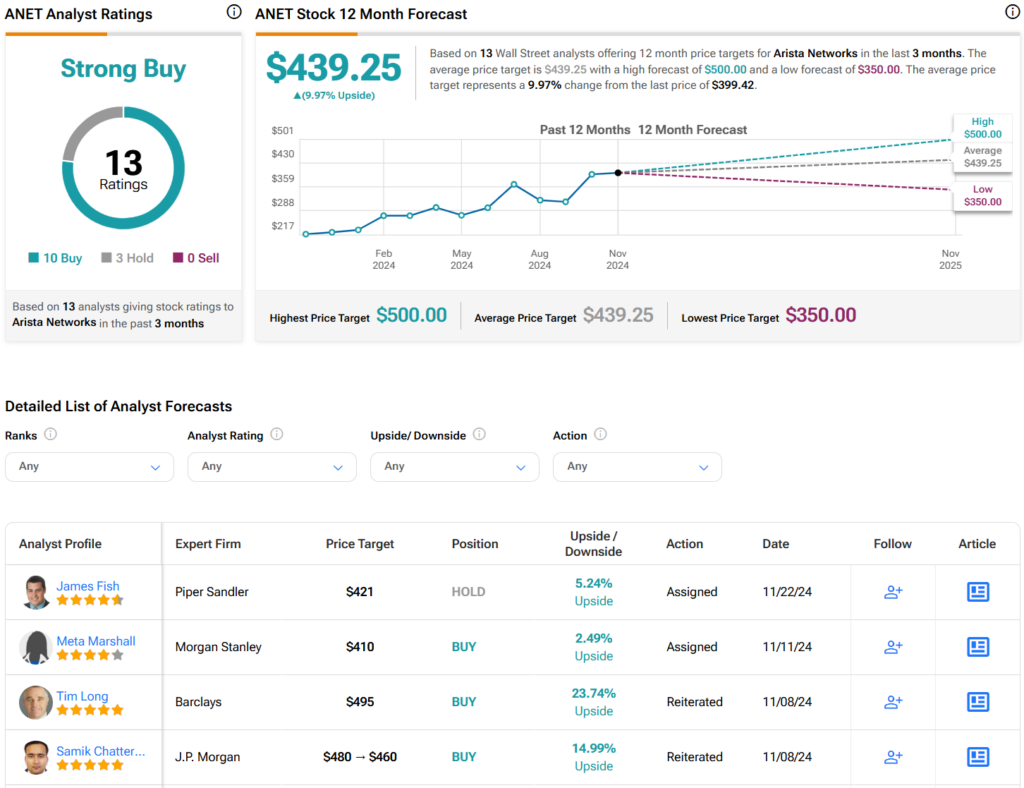

Turning to Wall Street, analysts seem to agree with my bullish view and have a Strong Buy consensus rating on ANET stock based on 10 Buys, three Holds, and zero Sells assigned in the past three months, as indicated by the graphic below. Furthermore, the average ANET price target of $439.25 per share implies 10% upside potential.

Arista Networks Is One to Watch

For investors looking to capitalize on the AI infrastructure boom, I think Arista offers something rare: a company that’s not just riding the wave but helping define its shape. Its demonstrated ability to capture and retain relationships with the world’s most sophisticated technology customers, combined with massive untapped potential in the broader enterprise market, creates a unique growth proposition. At current valuations, I suggest that the market appears to be undervaluing both its established strengths and expanding opportunities.

This is why I’m strongly bullish on Arista Networks. The company is not just participating in the AI revolution – it is dominating. For investors looking to capture the real value in AI infrastructure, I think Arista offers a clear technological advantage, with the financial strength and operational excellence to exploit it fully. Despite the inevitable risks of an emerging market, I think Arista will be one to watch for the foreseeable future.