The coronavirus epidemic, and the economic and society lockdowns put in place to combat it, have body-slammed the financial world; the S&P 500 is still down 13% even after a 5 week rally, while oil prices are stuck in a doldrums, with Brent trading at just $30 and WTI at $25. Corporate earnings season has been grim, and some 120 S&P companies have rescinded their 2020 guidance while others have canceled dividend payments or stock buybacks.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

So, investors are confused; they aren’t seeing the usual signals that indicate what the market may do, and opinions are deeply divided on whether we’ll see a true rally or a long-term bear cycle.

Writing from Wells Fargo, head of equity strategy Chris Harvey has come down on the bearish side, but with a caveat. “A near-term equity market pullback should not be unexpected – but we believe selloffs will be much shallower than those in the recent past,” he says, and goes on to add, “There still is substantial uncertainty, and the path forward is not set in stone. Market participants are deciphering shades of gray and for now we are accepting of data that is merely less bad.”

Looking at possible ways forward, Harvey expects that the ‘shallower’ selloff will find support from dividend stocks. He’s predicting that the equity market’s current upward trend has pushed the dividend future contract up towards $50. He does not expect dividend stocks to falter in CY20; they are the logical defensive move for investors seeking to remain in the market while protecting their income stream.

Harvey’s colleagues at Well Fargo are extrapolating from his general stance, and applying it to individual stocks. In a series of reports, the firm’s stock analysts outlined some low-cost, high-return dividend stocks that investors need to consider – and also one that may be too risky to try. We’ve pulled the details from the TipRanks database, so let’s find out what makes these stock moves so compelling.

Energy Transfer LP (ET)

We’ll start in the energy sector, where strong dividends are common. The collapse of oil prices – America’s WTI benchmark dipped into negative territory for the first time ever on April 20 – hurt the industry, but there is still some resilience there. Energy is a non-negotiable requirement in modern society, and there is always current demand for hydrocarbon products. Energy Transfer, a midstream company, is well positioned to take advantage of hydrocarbon demand; it controls pipelines, terminals, and storage tanks for both crude oil and natural gas in 38 states. The company operates mainly in the Texas-Oklahoma-Louisiana and Midwest-Appalachian regions.

ET finished 2019 with a solid earnings report, beating both the EPS and revenue expectations while growing both metric year-over-year. Heading into Q1, the company had also increased its distributable cash flow by 2%, to $1.55 billion, an excellent signal for dividend investors. The company will report Q1 this evening, and the outlook is for 32 cents EPS, down 15.7% sequentially. At the same time, the revenue forecast is looking at a 6.8% yoy increase to $14.02 billion.

The cash flow is likely to be the more important figure, as far as investors are concerned. ET has been keeping up reliable payments for the last eleven years, and the current quarterly dividend, of 30.5 cents, is set for payment on May 19. The current payout ratio is high but still affordable – and even if earnings drop to the expected 32 cents, the company will still be able to cover the dividend payment. And at 16%, the dividend yield is simply stellar – far higher than the 2% average among S&P listed companies.

Analyst Michael Blum reviewed this stock for Wells Fargo, and took a clearly bullish position. Blum rates ET shares a Buy, with a $12 price target that suggests an impressive 59% upside potential for the coming year. (To watch Blum’s track record, click here)

Supporting his stance on ET, Blum looks to the long-term and writes, “[H]ydrocarbon use will [not] dramatically decrease within the next ten years (and beyond) and thus, [we are] not concerned with obsolescence risk for its pipeline assets. The company would consider renewable investments if they met ET’s return thresholds. However, to date, returns for renewable projects are below that of midstream.”

Overall, the analyst consensus on ET is a Moderate Buy, based on 13 recent reviews. The breakdown among those reviews skews positive, with 8 Buys versus 5 Holds. Shares are selling for $7.64, and the average price target of $11.85 implies an upside of 55%. (See ET stock analysis on TipRanks)

MPLX LP (MPLX)

Staying in the energy industry, we’ll look at MPLX. This company was spun off of Marathon Petroleum in 2012, to handle the oil giant’s midstream operations. Marathon still holds a controlling interest in MPLX, which in turn owns and operates assets in pipelines, terminals, inland river shipping, and refineries. MPLX operates in both the petroleum and natural gas midstream segments.

MPLX has a seven-year history of growing its dividend, and the current payment of 68.75 cents per quarter is due out on May 15. Annualized, the dividend comes to $2.75 and gives a yield of 16%. Compared to current interest rates, which have been slashed to the bone in an attempt to counter the economic hit from the coronavirus shutdowns, this yield is a clear attraction for investors.

The dividend is supported by a cash-rich business model. MPLX generated $4.1 billion in net cash during calendar year 2019, and returned $2.8 billion to shareholders through dividends and buybacks. The company has reduced its capital spending for 2020 to compensate for reduced income during the 1H20 economic downturn. The company a heavy net loss for Q1, of $2.7 billion, but still was able to generate $1 billion net cash.

Michael Blum, quoted above, also cast his gaze on MPLX. He wrote, “We entered 2020 with a defensive mindset… We continue to expect near-term volatility as crude storage fills and WTI oil prices likely head lower… the sector is technically oversold, which should create long-term buying opportunities for investors that have the wherewithal to step in… for investors with a bit more risk appetite, [MPLX] appears attractive on a multi-year time horizon…”

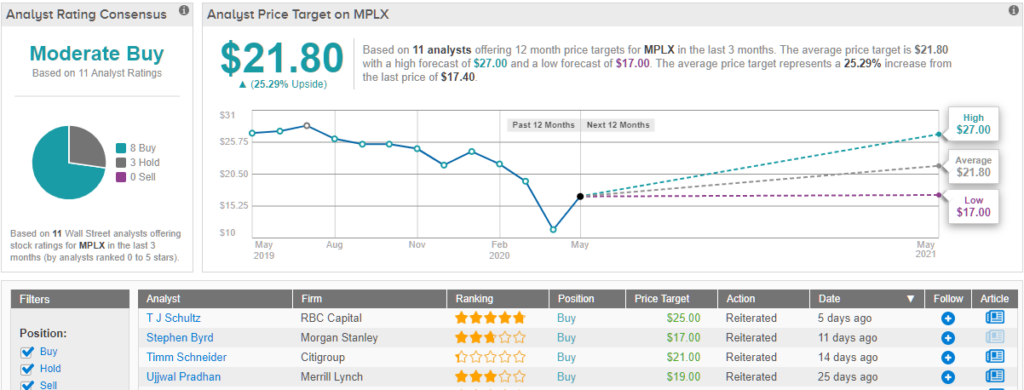

In line with this stance, Blum gives MPLX a Buy rating. His $24 price target implies a strong upside potential here of 38%.

For the most part, Wall Street appears to agree with Blum on MPLX. The stock has received 11 recent reviews, of which 8 are Buys and 3 are Holds, making the analyst consensus rating a Moderate Buy. Shares are currently trading for $17.72, while the average price target of $21.80 suggests a one-year upside potential of 23%. (See MPLX stock analysis on TipRanks)

Bain Capital Specialty Finance (BCSF)

The world of business development companies (BDCs) has long sparked the interest of investors. These companies invest capital into the business world, earning their own profits on the returns. Bain has $105 billion in assets under management, in real estate, venture capital, and both private and public equity. Current economic conditions have hit Bain hard, as many of the company’s portfolio assets are underperforming due to the coronavirus shutdowns.

Despite volatile earnings, Bain is maintaining its dividend. The 41-cent dividend is sustainable at current earnings levels, and has been held steady for the past six quarter – but the payout ratio of 93% indicates that there is not much slack here. The yield, however, is 15.6%, so for investors willing to shoulder the risk, the reward may be substantial.

Well Fargo analyst Finian O’Shea sees too much risk here to justify the possible reward. The analyst points out that BCSF has started process to open up a rights offering, putting common stock at a discount. This is a move to raise new capital fast, and shows softness in the stock’s position. O’Shea writes, “…this is the first of what the market speculates as a wave of below-NAV issuance in the BDC industry. We don’t see a big wave noting BCSF was more leveraged, at 1.72x net including revolvers as of 12/31 – so there was not a lot of mark to market leeway.”

To this end, O’Shea rates the stock a Sell, predicting it will underperform in the coming year. In line with this, O’Shea cut the price target by nearly half, to $9.50, suggesting an 11% downside from current levels. (To watch O’Shea’s track record, click here)

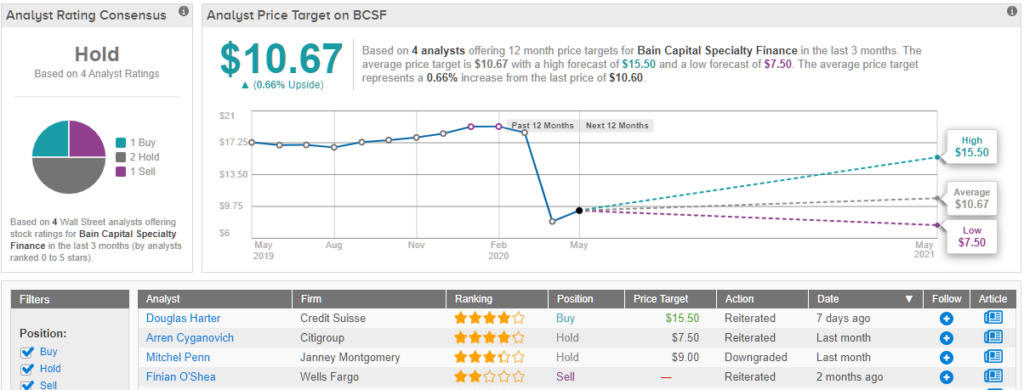

The Wall Street analyst corps, generally, are cautious on this stock. The consensus rating, a Hold, is based on a single Buy along with 2 Holds and 1 Sell. The upside is also modest; the average price target of $10.67 indicates room for just 0.66% growth from the $10.60 share price. (See Bain Capital stock analysis on TipRanks)

To find good ideas for dividend stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.