For those pining for the year’s early bull run to pick up steam again, take heed. One well-known investing sage thinks that is completely unlikely to happen.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Billionaire investor Leon Cooperman thinks the S&P 500 is about to slip by 22% from here while also anticipating the US economy gets dragged down into a recession.

“I think QT, Fed tightening, the high price of oil, or maybe a strong dollar — some combination of these four things creates a recession, and the final bottom of the market will be about 35% below the 4,800 peak,” the chairman and CEO of Omega Advisors elaborated.

However, that’s not to say Cooperman has been throwing out the baby with the bath water. In his portfolio, and accounting for a big chunk at that, there are names that over the past year have outperformed the market by a wide margin. By holding on to them, Cooperman evidently thinks that while bad times are coming, these stocks will keep on delivering.

With this in mind, we dipped into the TipRanks database and pulled up the details on two Cooperman-owned stocks. Do the Street’s cadre of stock experts also think these are worth picking up right now? Let’s take a closer look.

Fiserv, Inc. (FISV)

We’ll start with Fiserv, a leading fintech company that offers financial services and payment solutions. The firm provides merchants and financial institutions with cutting-edge tech tools to facilitate and oversee financial transactions. Services also include account processing systems, customer management and online banking, risk compliance instruments, and data analytics, amongst others. These solutions are used by more than 10,000 customers across the globe and in major industries such as banking, insurance, telecommunications and healthcare.

It’s a model that has served the company well in recent times, as was evident in the latest quarterly statement – for 4Q22. Revenue rose by 8% year-over-year to $4.36 billion, edging ahead of consensus by $10 million. At the other end of the scale, adj. EPS rose 22% y/y, from $1.57 in 4Q21 to $1.91 in 4Q22, while meeting Street expectations.

There was promising stuff in the outlook too. For 2023, the company is calling for organic revenue growth between 7% and 9% and adjusted earnings per share between $7.25 to $7.40, above Wall Street’s $7.28 forecast.

The Street liked the results, sending shares higher in the aftermath of the release. In fact, investors have been propping up the shares over the past year. The stock has posted 12-month gains of 19%, far outpacing the S&P 500’s 8% loss.

Cooperman must think that FISV stock will keep on outperforming. Almost 9% of his portfolio is taken up by FISV shares. Specifically, he holds 1,030,600 shares, currently worth just over $118.6 million.

Tigress Financial’s Ivan Feinseth is also a big fan of Fiserv. Laying out the bull case for the fintech company, the 5-star analyst writes: “FISV’s industry-leading position, asset strength, agility, and new product launches will continue to drive accelerating growth. FISV continues to benefit from online and in-store payments growth, and it is one of the leading companies driving new payment technologies and the secular shift to electronic payments. FISV will continue to grow within a growing market and increasingly penetrate a growing client base through ongoing new product development and strategic acquisitions to expand its product and services portfolio.”

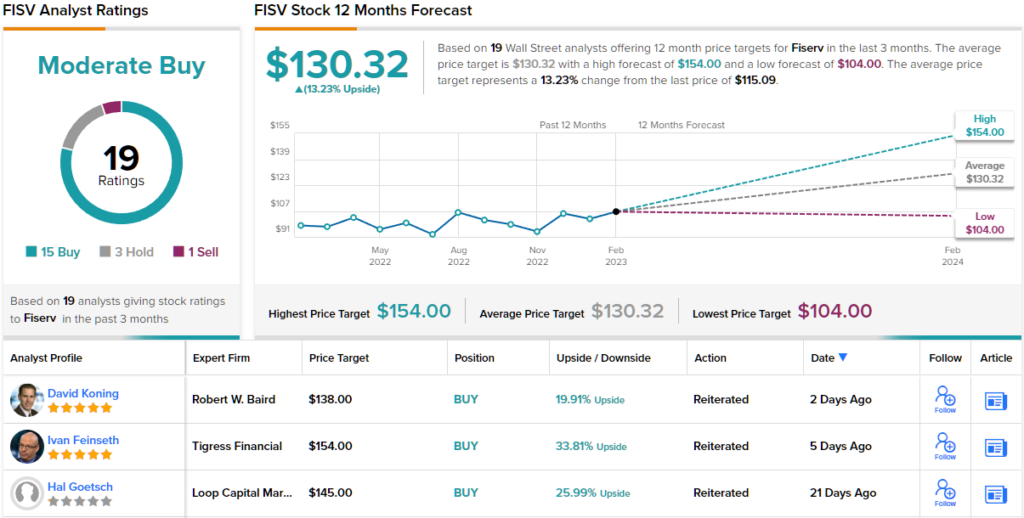

These comments form the basis for Feinseth’s Buy rating on FISV, while his $154 price target makes room for 34% share growth in the year ahead. (To watch Feinseth’s track record, click here)

Most on the Street agree with Feinseth; FISV’s Moderate Buy consensus rating is based on 19 reviews, breaking down to 15 Buys, 3 Holds, and 1 Sell. The current trading price is $115.09, and the $130.32 average price target implies a one-year upside of ~13% from that level. (See Fiserv stock forecast)

The Cigna Group (CI)

The next Cooperman-endorsed stock is Cigna, a global health services company. This large-cap provides insurance and health services to a whole range of customers, including businesses, families and individuals. In fact, Cigna is one of the health industry giants, and one of the world’s biggest health insurers.

Some numbers tell the story nicely; The company saw out 2022 with almost 190 million total customer relationships and total revenues for the year were $180.5 billion. The health insurance industry is expected to keep on expanding over the coming years, making Cigna well-positioned to benefit from the growing demand for health insurance.

The company recently delivered a solid report to close out 2022. Q4 revenue hit $45.75 billion, in-line with Street expectations while adj. EPS of $4.96 bettered the analysts’ $4.87 forecast.

However, the outlook came in a bit soft; for the full year, the company sees adjusted revenues of at least $187 billion vs. consensus at $190.20 billion.

The shares trended down post-earnings and have underperformed so far this year. Nevertheless, zoom out a bit and you find that over the trailing twelve months, the shares have significantly outperformed the broader market – having appreciated by 25% over the period.

This blue chip also pays a regular dividend. It currently yields 1.68% – more or less the same as the S&P average – but given the company only recently increased the payout by 10%, further increases could be forthcoming in the years ahead.

As for Cooperman’s involvement, he owns 450,000 shares, which make up almost 9% of his portfolio. At the current share price, these are worth more than $131 million.

Covering the stock for J.P. Morgan, analyst Lisa Gill believes momentum is “set to carry into 2023.” Looking ahead, the 5-star analyst writes, “While recession remains a concern given CI’s exposure to the Commercial market, management noted that an uptick in dis-enrollment is baked into 2023 guidance. We are also encouraged by strong performance within Evernorth (the subsidiary that provides pharmacy, care, and benefit solutions) reflecting substantial new client wins (Centene PBM contract), customer retention returning to historical levels in the upper-90% range, and with specialty pharmacy a key long-term tailwind.”

“We believe CI deserves to trade above its historical multiple given the growth opportunity within specialty and biosimilars, in particular, coupled with continued strong growth in the health plan business,” Gill went on to add.

To this end, Gill rates CI shares an Overweight (i.e. Buy) backed by a $370 price target. The implication for investors? Upside of ~28% from current levels. (To watch Gill’s track record, click here)

Elsewhere on the Street, the stock garners an additional 7 Buys and Holds, each, for a Moderate Buy consensus rating. The forecast calls for one-year returns of ~21%, considering the average target stands at $352.33. (See Cigna stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.