The AI boom is reshaping parts of the tech industry, and one of the clearest examples is in the data center space. A growing number of high-end operators are shifting toward leasing capacity, opening up infrastructure to support AI and high-performance computing workloads.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

That shift is being driven by surging demand for AI computing power, with leasing providing a more predictable and recurring revenue stream than other uses of that infrastructure.

Chardan analyst Bill Papanastasiou, who ranks among the top 1% of Wall Street analysts, has been tracking the trend closely, and sees meaningful upside for the right players.

“We believe that there is a significant re-rate opportunity for companies with high quality power assets that are able to execute on tight delivery timelines amidst a global shortage of readily available power (McKinsey estimates that the United States will be faced with a 15+ GW shortfall in the next five years). Companies that are able to attract a diverse and credit-worthy tenant base will likely see benefits cascade into a relatively lower cost of capital and superior valuation to direct peers if they can prove out their respective execution strategies,” Papanastasiou opined.

With that in mind, Papanastasiou has zeroed in on two data center stocks he sees pushing higher from here. We dug into the TipRanks database to gauge just how much upside Wall Street is assigning to these names.

Riot Platforms (RIOT)

First up, Riot Platforms started out as a bitcoin miner – but nowadays the company has diversified into power distribution and data center leasing. The company has four data center facilities, two in Texas and two in Kentucky, as well as electrical engineering facilities in Colorado and Texas; the electrical engineering facilities manufacture the custom switchgear and other necessary infrastructure that supports the data center operations. Riot’s Rockdale data center, in Texas, has over 700 megawatts of capacity and is one of the largest such facilities in North America.

The electrical equipment business is handled through Riot’s fully owned subsidiary ESS Metron. Owning this subsidiary gives Riot a distinct advantage, allowing the company to keep its ancillary systems ‘in house;’ data centers make high demands for advanced electrical equipment, so having a ready source, while expanding its data center operations, is invaluable.

In an important development earlier this year, Riot officially branched into data center service leasing. In January, the company signed a 10-year agreement, worth $311 million, with the chip maker AMD. The agreement is for the lease of 25 megawatts of critical IT load at the Rockdale data center. Riot followed this agreement with the announcement of a 112-megawatt infrastructure development at the Corsicana facility, to be dedicated for data center tenants.

For Chardan’s Bill Papanastasiou, the key points here are Riot’s solid base for expanding the data center business, and its success in securing a quality ‘first tenant.’ He writes of the stock, “RIOT is well-positioned on its strategic pivot towards AI/HPC workloads given access to 1.7GW of power capacity in Texas (with a clear line of sight to full energization by year-end). In our view, this represents one of the most attractive portfolios in the peer group on account of scale and degree of power certainty (fully approved with long-lead items secured and an in-house engineering division to facilitate with the buildout). RIOT has also secured a high-quality anchor tenant, which should help obtain project financing at a low cost of capital. RIOT’s financial positioning remains strong with a ~$1.5B in total liquidity (inclusive of the Bitcoin treasury) that will be gradually tapped to fund capex and operations.”

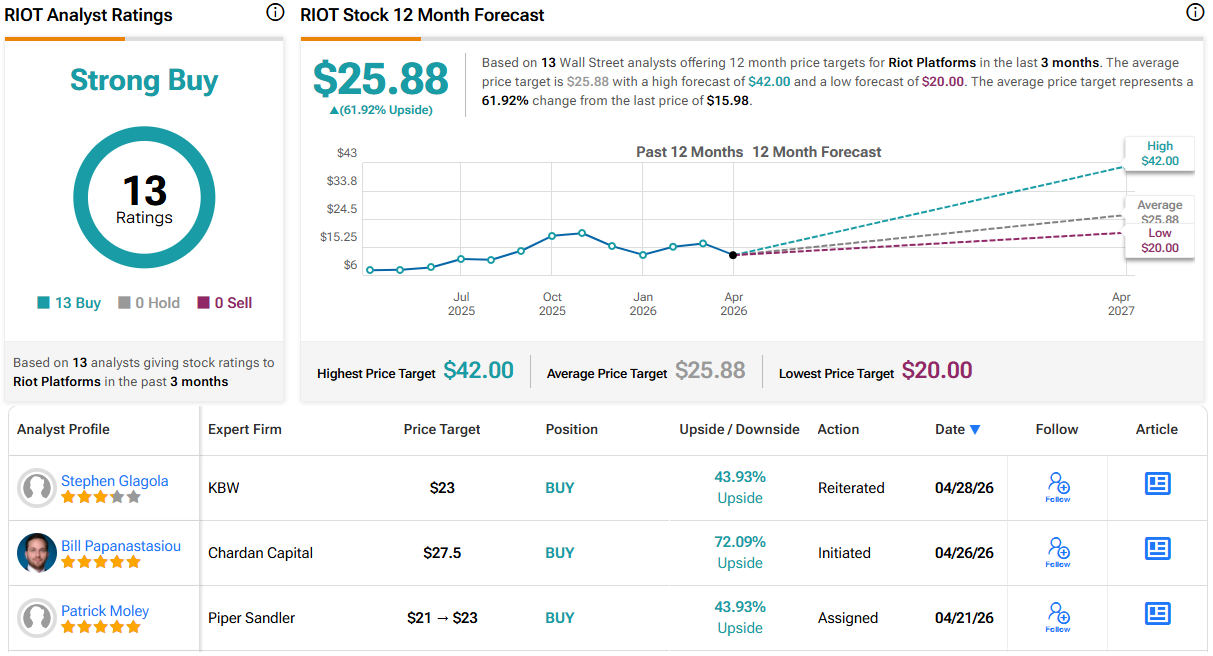

The 5-star analyst goes on to rate RIOT shares as a BUY, with a $27.50 price target that implies a one-year upside potential of 72%. (To watch Papanastasiou’s track record, click here)

All 13 recent analyst reviews here are positive, giving RIOT a unanimous Strong Buy consensus rating. The shares are trading for $15.98, and their $25.88 average price target suggests that this stock will gain 62% by this time next year. (See RIOT stock forecast)

Galaxy Digital (GLXY)

The second Chardan pick we’re looking at is Galaxy Digital, a firm that handles financial services and investment management related to data center infrastructure, digital assets, and blockchain technology. The company has a digital assets platform designed to link the traditional finance sector with the digital economy and includes a data center segment that aims to provide the ‘cutting-edge AI and high-performance computing (HPC) infrastructure’ that is in increasing demand across the digital landscape.

Some numbers show the scale of Galaxy’s business. The company has $9 billion in assets on its platform as of this past March 31 and more than 1.6 gigawatts of approved capacity at the data center campus. That campus, called Helios, is located in Dickens County, Texas, and sprawls across more than 1,500 acres. We should note that Texas, one of the fastest-growing state economies in the US, has been highly successful in attracting data center businesses.

The Helios data center campus is based on adaptable and scalable infrastructure supply to meet the needs of any customer. The facility design is optimized for maximum performance in the areas in high demand: AI capability and high-performance computing, with large workloads and high throughput.

For potential customers, Galaxy offers a variety of services. These include access to an impressively large array of digital asset products; investment solutions for the digital age; and the latest in AI- and HPC-capable data center tech. All of these combine in a mutually supporting loop, based on mastering the needs of digital finance.

Galaxy has just released its 1Q26 results. The $10.2 billion in revenue was down 23% year-over-year but beat the estimates by $1.30 billion. The EPS loss in the quarter, 49 cents per share, marked a strong year-over-year improvement and was 44 cents per share better than had been forecast.

Turning to Papanastasiou again, we find the Chardan expert taking an upbeat view of this company. He writes, “In our view, Galaxy offers investors broad exposure to the emerging digital assets ecosystem through a diversified offering of financial services reinforced by long-standing thought leadership in identifying emerging and/or compelling opportunities. The company has also developed a robust AI/HPC data center infrastructure business that is set to generate stable, predictable cash flows to bolster the top line in the near-term and could become a leading revenue stream while providing downside protection from the volatility and lumpy business activity from the digital assets business. With 830 MW available to be contracted and a robust pipeline to +3.4GW, we think the stock is sitting at an attractive entry point.”

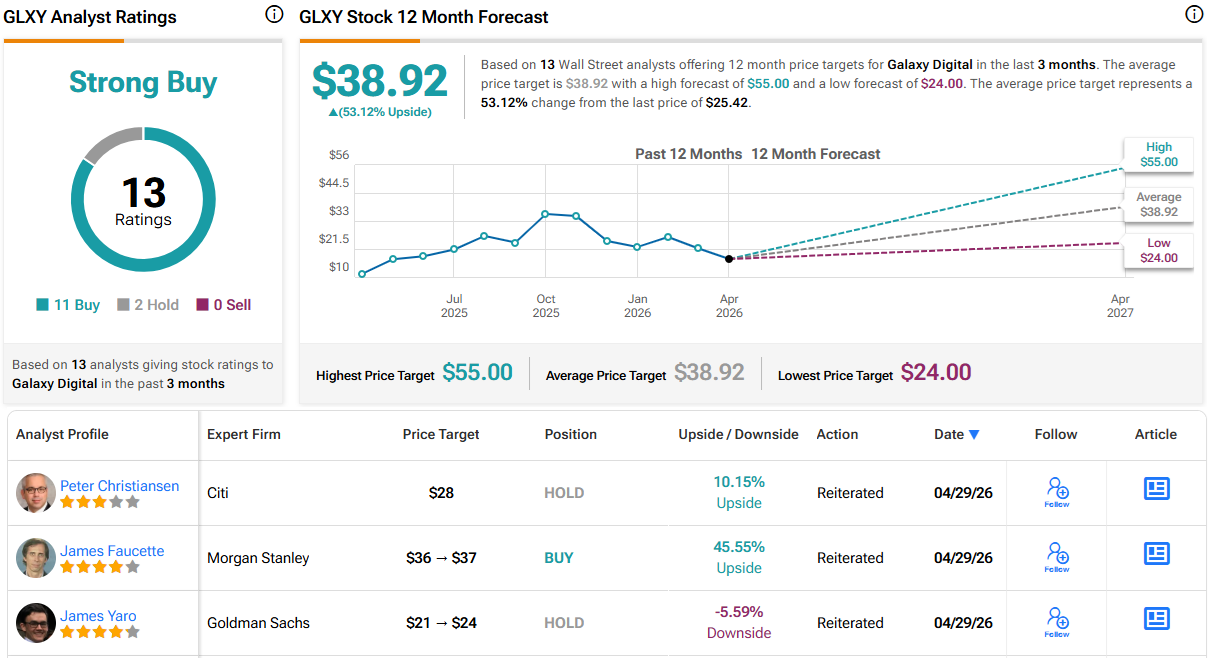

Papanastasiou follows those comments with a Buy rating, as well as a $35 price target that points to a 38% upside by this time next year.

Overall, GLXY holds a Strong Buy consensus rating, based on 13 recent reviews that include 11 Buys and 2 Holds. The stock is priced at $25.42, and its $38.92 average target price suggests that it will gain 53% on the one-year horizon. (See GLXY stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.