Wall Street is awash with stock analysts, publishing reports and recommendations by the score every day. It’s a flood of information whose sheer volume makes it difficult to sort the wheat from the chaff. For investors, finding the best analysts – and following their stock commentary and picks – is a clearly viable trading strategy. Finding the analyst to follow is the trick.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

TipRanks has the information you need. The database of Wall Street analysts is regularly updated, and the analysts themselves are ranked by several factors, including the accuracy of their recommendations and their average returns. You can find the very best of the analysts – and TipRanks follows the data on more than 6,000 professional financial experts – at the Top 25 Analysts page. It’s a ‘Who’s Who’ of the very best in the financial world.

Today we’ll follow 5-star analyst Terry Tillman, ranked #6 overall in the database. Tillman is a tech sector analyst with SunTrust Robinson. He has 224 stock ratings, of which 179 have successfully brought a positive return. This gives him an 80% success rate – and that average return is 38.9%. It’s clear now why Tillman is so highly rated. Let’s take a look at three of his recent Buy recommendations.

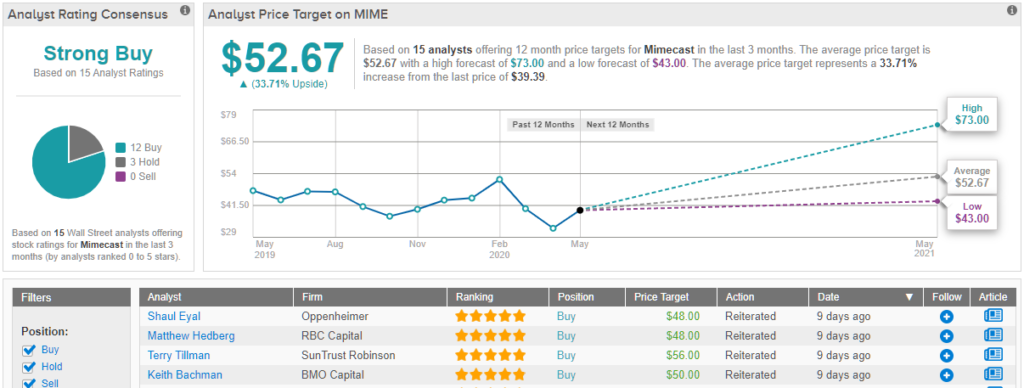

Mimecast, Ltd. (MIME)

We’ll start with Mimecast, a cloud-based cybersecurity firm specializing in email management and protection systems. The company offers archiving, continuity, and security services designed to promote the safety of business email.

The company’s recent quarter showed strong sequential growth and beat expectations by a wide margin. The report, for fiscal 2020 Q4, showed total revenue of $114.2 million, up 24% year-over-year, and a net gain of 1,200 new customers, giving a global customer base of 38,100. Full year revenue was up 25% from fiscal 2019.

Tillman is generally impressed with Mimecast’s performance, and more so with its future prospects. He writes of the company, “The broader impact of the crisis is expected to be reflected in downsell and churn especially as customers request shorter billing periods while others seek to extend payment terms – the company expects net revenue retention to be between 106% – 107% for the year…”

Mimecast added, “We continue to believe the company should benefit from a variety of growth levers in increasing expansion sales, Office 365 customer adoption, and solid sales execution in the mid-market and enterprise but also understand the near-term risks associated with the current COVID-19 outbreak.”

In line with is upbeat comments, Tillman gives MIME a Buy rating and a $56 price target. This target implies a 42% upside potential for the stock in the coming 12 months. (To watch Tillman’s track record, click here)

The Wall Street view of MIME is in general agreement with Tillman’s. Of 15 recent reviews, 12 are Buy and 3 are Hold, giving the stock an analyst consensus rating of Strong Buy. Shares are priced at a discounted rate of $39.39, and the average price target of $52.67 suggests a one-year upside of 34%. (See Mimecast stock analysis on TipRanks)

Upland Software (UPLD)

Next up is another software company. Upland offers software solutions for issues common to most businesses, including contact center and customer experience management, document automation and security, enterprise sales, and project management. The company has worked hard to expand its product offerings, and has a track record of acquiring smaller cloud software competitors – and adding their products to Upland’s own line.

Upland has reported three quarters in a row of sequential gains. For Q1 20202, earnings were up 5% sequentially and an impressive 35% year-over-year. Revenues, at $48.5 million, grew 53% yoy.

Upland has not forgotten its own reputation management during the coronavirus crisis. The company is offering a free webinar for customers, on increasing productivity in remote work situations. While not impacting the company’s bottom line, it’s a fine example of turning a difficult situation to advantage.

Even though UPLD has underperformed in recent months, Tillman sees this stock as a Buy opportunity. In a nod to the crisis, he has lowered his price target from $56 to $46 – but even at the lower level, his target suggests an upside of 51%.

Supporting his view of the stock, Tillman writes, “Upland is halting M&A activity in the near term while focusing on go-to-market enhancements and supporting current pipeline. While M&A has served as a meaningful catalyst we believe the increased focus on GTM and product integration could be positive for organic growth in the long-term. Additionally, we are encouraged by the high level of customer expansions and major account adds in 1Q.”

The analyst consensus rating on UPLD a Strong Buy, and it is unanimous. The stock has received no fewer than 7 Buy ratings in recent weeks. The current trading price is $30.43, and the average price target of $43 indicates room for 41% upside growth this year. (See Upland stock analysis on TipRanks)

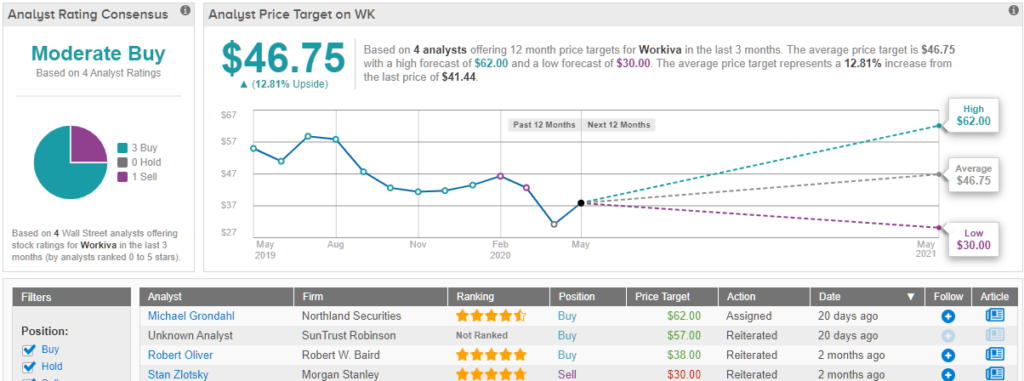

Workiva, Inc. (WK)

Third on our list here is Workiva, a provider of cloud-based business data analysis software. The company’s products permit real-time collections, management, and reporting of data, and is used for accounting, compliance, finance, and risk management.

Workiva’s recent quarterly earnings and stock performance have shown a pattern opposite to the companies above. The company has consistently reported net losses in its quarterly reports, although the magnitude of the losses has been decreasing since Q3 2019. In the most recent quarter, Q1 2020, the EPS loss came in 52% better than expected, while revenue beat the forecast by 4%.

At the same time the company has been reporting consistently net losses, share price has performed in line with the broader markets. WK is only down 14% since the current collapse-and-rally cycle began, which is comparable to the S&P loss of 12%.

Looking into Workiva’s recent quarterly, Tillman is impressed. He notes, “We believe solid 20%-plus top-line growth in 1Q20, large deal metrics and revenue retention offer a window into solid sustained growth post COVID-19. [We have] raised profit and CF assumptions for 2020.”

In line with this rosy outlook, Tillman rates the stock a Buy. His $57 price target indicates confidence in a one-year upside potential of 37%.

Overall, the Street is more cautious here than Tillman. The analyst consensus rating, a Moderate Buy, is based on 3 Buys and 1 Sell. Shares are priced at $41.50, while the average target of $46.75 implies a 13% upside. (See Workiva stock analysis on TipRanks)

To find Terry Tillman’s ratings and price targets, click here.