Finding the right stocks is crucial for market success, but the real challenge lies in spotting them.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

This is no easy task. The stock market constantly churns out vast amounts of raw data, fueled by millions of traders exchanging billions of shares every day. For most investors, navigating this overwhelming flow of information can feel impossible without the time or expertise to sift through it all.

This is where the TipRanks Smart Score comes in. It’s a tool designed to provide an impartial and data-driven look at the market, using AI-powered natural language algorithms to collect and collate the stock market data – and to use that data to rate every stock according to a set of factors that are known predictors of future outperformance. Those ratings are given on a simple scale of 1 to 10, with the ‘Perfect 10’ indicating stocks that deserve a closer look. It’s a simple, clear, and objective guide that investors can use in their stock picking.

That guide is even clearer when it lines up with recommendations from Wall Street analysts. These professional stock experts bring human experience and intuition to the field of stock picking, and they build their careers on the quality of their analyses. So, when they align with the Smart Score, investors know they’re getting the best of two viewpoints – both natural and artificial intelligence.

Against this backdrop, we’ve opened up the TipRanks database to find two stocks that have earned the top-scoring ‘Perfect 10’ as well as ‘Strong Buy’ ratings from the analysts. The data shows that they are poised for growth, with double-digit upside potential; here are the details.

Schlumberger Limited (SLB)

First on our list today is Schlumberger Limited, one of the energy industry’s major names in oilfield services. This company is, at heart, an engineering firm, offering oil and gas exploration and production firms the skill and expertise they need in a wide range of areas, including drilling, hydraulic engineering, wastewater disposal, and pollutant control. These are all niche fields, requiring highly specific technical knowledge, and Schlumberger brings them to the oil patch, both onshore and offshore.

In addition to its oilfield services, Schlumberger is looking toward the future, and working to bring new sectors of the energy industry to life. The company has a strong stance in digital technology, and its applications to oil and gas extractions with an emphasis on scaling to fit the needs of any customer. Schlumberger is also working on AI tech, with an eye toward building autonomous operations in active oil and gas fields. And finally, Schlumberger has active projects in both new energy systems, to facilitate the transition away from fossil fuels, and in decarbonization, to facilitate a cleaner and more sustainable energy industry.

These operations, and more, brought Schlumberger a top line of $9.14 billion in the second quarter of this year, the last period reported. This revenue figure was up ~5% year-over-year, and beat the forecast by $50 million. At the bottom line, Schlumberger’s non-GAAP earnings-per-share came to 85 cents, 2 cents per share better than had been anticipated. In another important metric, the company generated $1.44 billion in cash flow from operations, with a free cash flow of $776 million.

Schlumberger shares have picked up positive coverage from Evercore analyst James West, who sees the company as fundamentally strong, particularly in its core areas of work, and believes that the stock is undervalued. Laying out this position, West writes of Schlumberger, “The company continues to see strength within international and offshore markets with the expectation that SLB’s breadth and diversity will continue to support revenue growth and margin expansion and we believe the fundamentals are in place to support long-term resiliency through the cycle and we don’t see any near-term headwinds that would disrupt its pipeline through 2025. This coupled with its strong backlog provide further support for its growth and margin expansion initiatives… At current valuation levels, shares of SLB are severely undervalued.”

These comments back up the analyst’s Outperform (Buy) rating, while his $74 price target implies that a one-year gain of 77% lies ahead for SLB. (To watch West’s track record, click here)

Overall, this stock’s Strong Buy consensus rating is based on 14 Wall Street reviews, that include a lopsided split of 13 Buys to 1 Hold. The shares are priced at $41.81 and their $65.77 average price target suggests an upside of 57% in the next 12 months. (See SLB stock forecast)

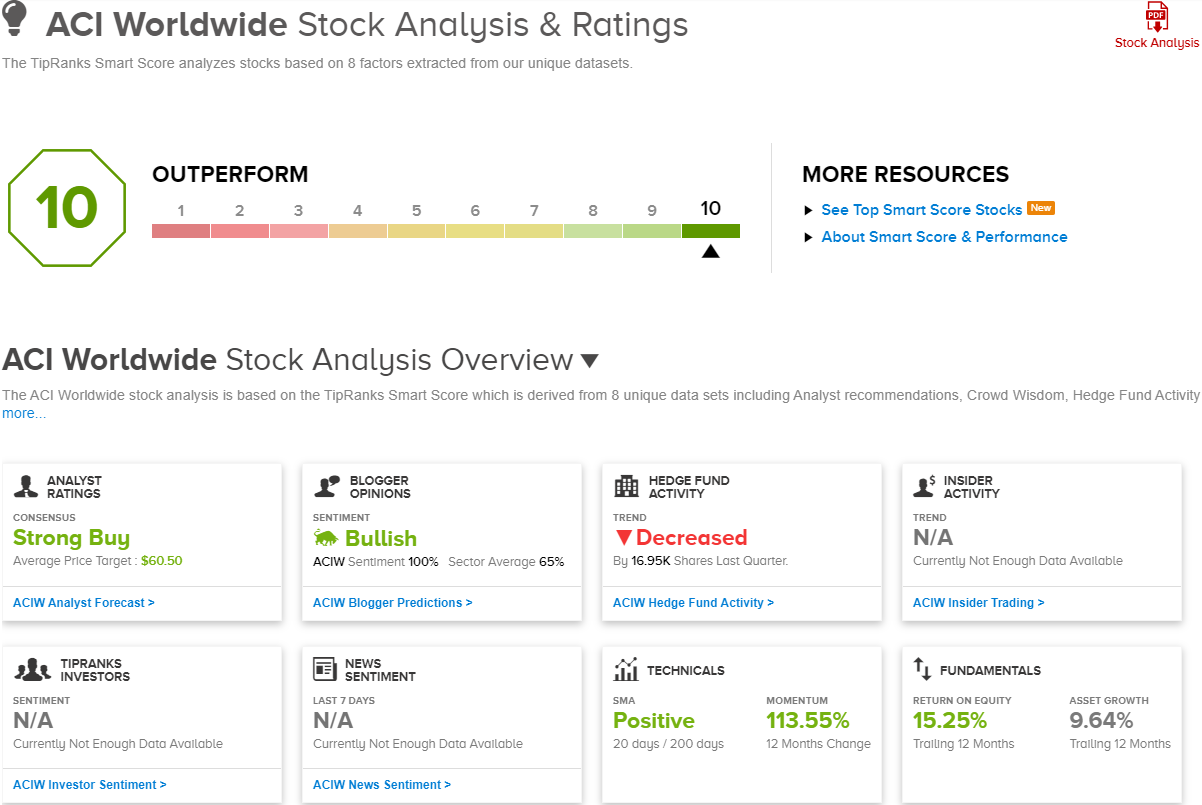

ACI Worldwide (ACIW)

Next on our Perfect 10 list, ACI Worldwide is a leader in the field of real-time online payment solutions tailored for banks, retailers, and billers. The company enables its customers to better process and manage their digital payments, present and process their bills and receivables, and to manage the risk and fraud factors inherent in digital transactions. ACI’s platforms have helped more than 80,000 brands meet the challenges of commerce and payments in the modern world.

The Florida-based company employs around 4,000 people and has operations in 23 countries. ACI processes some 25 billion cloud transactions every year, along with more than 225 billion consumer transactions. The company generated $1.45 billion in total revenue last year, for a 5% year-over-year gain, and boasted $1.1 billion in annual recurring revenue for 2023.

Turning to the more recent financials, we see that ACI’s last reported quarter, 2Q24, had a top line of $373 million, up more than 15% y/y and more than $23 million ahead of the forecasts. The company’s bottom line for the quarter was an EPS of 29 cents, by GAAP measures, 22 cents per share better than had been expected.

We should note that the company’s management is active in supporting the stock, and in June of this year the Board authorized a new, $400 million buyback program for common stock shares. This authorization includes the $65 million left over from the previous buyback program. As of mid-June, when the company authorized the buyback, ACI’s 2024 stock repurchases had totaled 3 million shares for $106 million.

Canaccord Genuity’s Joseph Vafi covers this stock and takes a bullish stance. Vafi particularly likes management’s ability to execute a sound strategy, and notes the company’s commitment to supporting the share price through buybacks. Summing up, the 5-star analyst writes, “Management’s goal over the medium term is to continue to drive HSD organic growth by focusing on key initiatives like the new payments hub, banks mid-tier expansion, and RTP, along with Speed-pay and merchant value-added services. Management is prioritizing investments in these areas while largely maintaining its capital allocation framework with an emphasis on share buybacks. The board authorized a new $400M share buyback program. Given the strong execution we have seen since Tom Warsop took over as CEO and the focused approach the company is taking, we believe the roadmap the company has laid out is reasonable and achievable.”

Following from this, Vafi – who is rated among the top 3% of Wall Street’s analysts by TipRanks – gives ACIW a Buy rating with a $60 price target that shows his confidence in a gain of 22% over the coming months. (To watch Vafi’s track record, click here)

While ACI Worldwide only has 5 recent analyst reviews, the 4 to 1 split favors Buys over Holds for a Strong Buy consensus. The shares are currently trading for $49.16 and the $60.50 average target price indicates a one-year upside of 23%. (See ACIW stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.