The March inflation showed an annualized CPI of 3.5%, the highest in six months, but there’s still debate on whether or not this deals a blow to the thesis that inflation is coming down. Yes, prices remain high, but the pace of increase is on a downward slope – even when we count March’s headline number. Common wisdom says that the Federal Reserve is still on track to lower interest rates later this year – although perhaps not as quickly as had previously been hoped.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The real key, according to a note from investment bank Jefferies, is that interest rates are not likely to start rising again – and rate stability is almost as good as cuts when it comes to the business scene. Companies want predictability in pricing, and they’ll have that in a stable rate environment.

Moving from this to look at the commercial real estate (CRE) segment and its reaction to current conditions, Jefferies analyst Peter Abramowitz says, “With the Fed signaling that inflation is close to under control, we believe the pieces appear to be in place for a recovery to begin in 2H24. First, and most importantly, is an expected stabilization and/or decline in interest rates… Regardless of how many rate cuts, we believe perceived stabilization in rates is the most important factor in thawing the investment sales market, as better visibility in financing costs will enable buyers/sellers to begin more confidently underwriting real estate values again.”

To that end, Abramowitz has pinpointed two CRE services stocks that investors should pick up right now. We’ve used the TipRanks database to find out what the rest of the Street has to say about these picks. Let’s take a closer look.

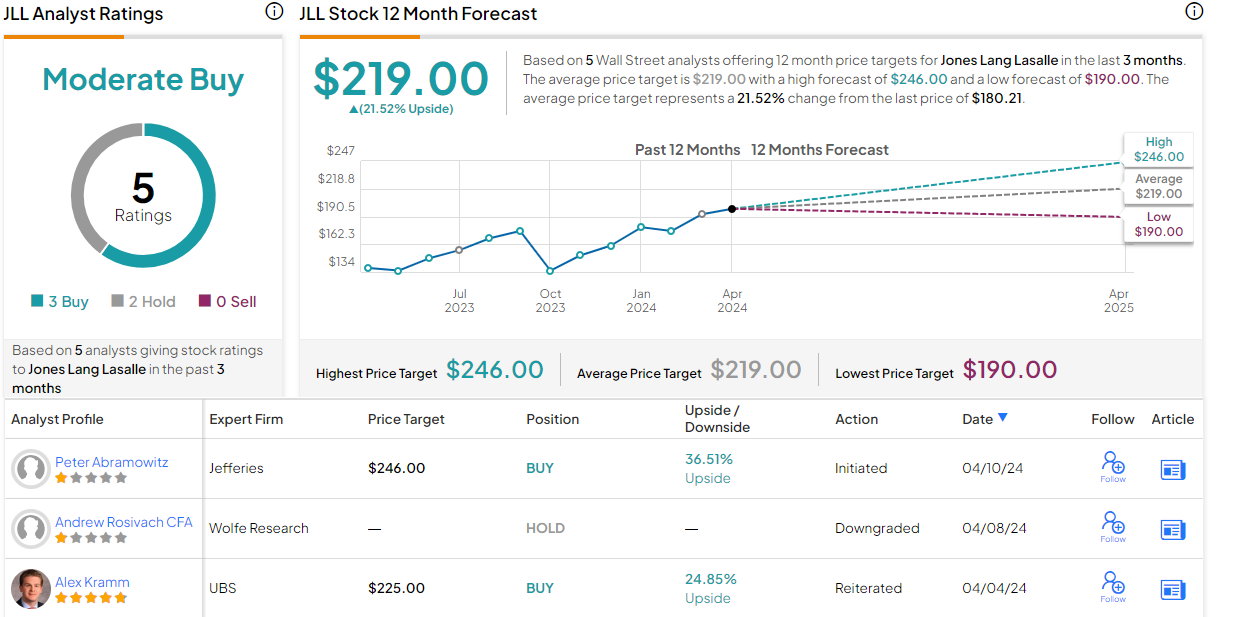

Jones Lang LaSalle (JLL)

We’ll start with Jones Lang LaSalle, a real estate services company with a truly global reach. JLL was founded in the UK, is currently headquartered in Chicago, Illinois, and operates in 80 countries. The company works with commercial clients to buy, build, occupy, and manage various commercial real estate properties and investments, and combines its global presence with local expertise.

A few numbers will show the scale of JLL’s operations, even after several years of difficult conditions in the commercial real estate world. The company has a hefty footprint in property and facilities management, taking care of 4.7 billion square feet, and it controls some 37,500 leasing transactions that total over 1.07 billion leased square feet. JLL’s customer base includes a wide range of investors, both institutional and retail, as well as corporate investment clients and high-net-worth individuals. JLL tailors its real estate activities and portfolio to a clientele that has ready money, immediately available for investment.

Over the past year, JLL has seen its revenues and earnings both take an upward trend. The company’s top line in the last reported quarter came to $5.88 billion, an impressive figure that was up 5% year-over-year and beat the forecast by $110 million. These revenues supported a bottom line, in non-GAAP measures, of $4.23 per share. While down from the $4.36 reported in the prior year quarter, the earnings figure beat the forecast by 50 cents per share.

Covering this stock for Jefferies, sector analyst Abramowitz sees JLL in a sound position to continue delivering performance improvements, writing of the company, “As the CRE services provider most tied to a recovery in capital markets and leasing activity, JLL stands to benefit the most from a market recovery. Despite optimism around a soft landing and a more stable rate environment, Street estimates are still hesitant around a recovery, modeling just +1.6%/+2.7% in Y/Y leasing/capital markets fee revenue growth in ’24, vs. our +5.3%/+3.9%, with a further divergence in 2025 (JEF capital markets fee revenue +21.6% Y/Y vs. consensus +12.3%). As such, we expect the stock to re-rate on upward earnings revisions as the recovery unfolds…”

Putting his expectations into quantifiable terms, Abramowitz rates this stock as a Buy, and he sets a $246 price target that suggests a solid one-year upside potential of 36.5%. (To watch Abramowitz’s track record, click here)

Overall, these shares have a Moderate Buy consensus rating, based on 5 reviews that include 3 Buys and 2 Holds. The shares are priced at $180.21 and their $219 average target price implies that they will gain 21.5% over the next year. (See JLL stock forecast)

Cushman & Wakefield (CWK)

Cushman & Wakefield, the second stock on our list, is another global entity working in commercial real estate services. The company offers management and investment services in commercial real estate, with the goal of delivering value for property owners and leaseholders. Cushman & Wakefield operates out of approximately 400 offices across 60 countries and reported $9.5 billion in total revenues last year. The company derives its revenues from its activities in ‘property, facilities, and project management, leasing, capital markets, and valuation and other services.’

In a recent report on the urban office landscape, Cushman & Wakefield painted a cautiously optimistic picture for the near-term. Acknowledging that new construction is going to slow down, and that supply currently outstrips demand, the company does see an opening for both renovated office spaces and ‘assets slightly further down the value chain.’ The company notes an increase in demand, pointing out that there is still a large demographic that wants to live in vibrant urban cores, and these people will need to work, shop, and play in physical locations. In a point that should not be ignored, Cushman & Wakefield states its belief that much of the post-pandemic ‘slack’ in urban office spaces – the vacancies caused by the increase in remote work – has filtered through the system. The result, in the company’s view, should be an increase in demand now that urban property owners have ‘right-sized’ their portfolios and begin to expand in line with current conditions.

When we look at CWK’s last reported financial release, from 4Q23, we find that the company generated $2.6 billion at the top line. This was flat from the prior year – but was $170 million better than had been anticipated. This revenue total was accompanied by an EPS of 45 cents according to non-GAAP standards, for a 5-cent per share beat of the estimates.

This is another stock that analyst Abramowitz sees on the cusp of solid performance gains. He writes of Cushman & Wakefield, “CWK has taken steps to make itself more operationally efficient, with $140M shaved off of its cost base in ’23. The company’s revenue breakdown is similar to that of CBRE’s (55% of fee revs from property, facilities & project management); however, we believe consensus estimates underestimate the potential for a rebound in capital markets activity in 2H24/2025, leading to our adj EPS estimates +7.1% vs. the Street in ’25. As such, we expect upward earnings revisions will help the stock re-rate more in line with peers (currently at a -44%/-35% discount on P/E and EV/EBITDA, respectively).”

Looking ahead, the analyst gives this stock a Buy rating with a $13 price target that implies a 31.5% upside potential on the one-year horizon.

This CRE firm has earned a Moderate Buy rating from the analyst consensus, derived from 2 recent Buys and 3 Holds. The stock is trading for $9.88 and carries a $12 average price target, indicating room for a 21.5% upside in the months ahead. (See CWK stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.