Investors are facing a dilemma. Markets are up; both the S&P 500 and the NASDAQ indexes are at record high levels, having fully rebounded from the crash in March. On the face of it, this would seem to be a perfect time to buy, to get into the markets on an upward slope. But some Wall Street pros approach the rally with caution. After all, the COVID-19 pandemic has not faded, and narrowing polls show that the upcoming November elections are up for grabs.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In this situation, investors want some assurance that a stock is upwardly mobile, and primed for growth. The markets generate an array of data, whose patterns of shift and change carry the answers that investors want – but making sense of that forest of data can be daunting. To find a path through it, investors can look up a stock’s Smart Score.

The Smart Score is a data analysis tool, which uses the real-time information collected in the database. The stock data is collated according to 8 separate factors, each of which is known to predict growth and share appreciation. The factors are averaged together, and given as a single-digit score, on a scale from 1 to 10, letting investors know at a glance the likely way forward for a stock.

And a perfect Smart Score, a 10, is a signal that investors should pay attention to. Here are the details on three such stocks, along with corroborative commentary from Wall Street’s analysts.

Quotient Technology (QUOT)

We’ll start in digital tech. Quotient Technology offers marketing solutions for e-commerce, creating digital coupons personalized by the use of deep data dives – online shopping histories, purchasing behaviors, and website visitations. The company’s ads and coupons are closely targeted to consumers.

The first half of 2020, containing the height of the coronavirus crisis, was hard on Quotient. End-use consumers, pushed out of work and forced to stay home, found themselves altering their purchasing habits. The company, which, like many tech operators, sees a net loss each quarter, saw that loss deepen in Q1 and again in Q2.

Quotient has a perfect ‘10’ Smart Score despite its contracting financials. Craig-Hallum’s Chad Bennett sees COVID-19 as helping to clear a way forward for the company.

“The pandemic is aggressively accelerating the adoption of grocery/CPG innovations (e-commerce, digital, etc.), that in turn will result in demand for QUOT’s solutions. We believe that the signing of Rite Aid and Hyvee (with more to come) as Retailer iQ and Performance Media partners is evidence of this claim. We have long praised QUOT’s solutions and the value they deliver to its partners… It is our belief that the pandemic will spur a secular shift, which QUOT will greatly benefit from,” Bennett explained.

Therefore, Bennett rates QUOT shares a Buy, and his $14 price target indicates a 60% upside potential for the year ahead. (To watch Bennett’s track record, click here)

Overall, the analyst consensus rating on QUOT is a Moderate Buy, based on 4 reviews. These include 2 Buys, 1 Hold, and 1 Sell. Shares are selling for $8.76 and the average price target of $10.65 suggests they have room for 21.5% growth from that level. (See QUOT stock analysis on TipRanks)

Renewable Energy Group (REGI)

Next up is Renewable Energy Group, an Iowa-based biodiesel company. Biodiesel is a cleaner burning variant of diesel fuel, derived from agricultural sources. REGI develops, manufactures, and distributes a range of biodiesel and other renewable clean fuels, with operations across 48 states – and in Germany. REGI is the largest biodiesel producer, going by volume produced, in the US.

The company finished Q2 with $546 million in revenues, beating the forecast by 8.5%. The higher sales figure reflects strong demand – and indicates that there is a market for the company’s product.

Writing for H.C. Wainwright, 5-star analyst Amit Dayal is impressed by REGI’s market position, saying, “We believe the company remains undervalued relative to the growth and business fundamentals it offers.” Getting into the details, Dayal adds, “We believe that: (1) the recent stability in the energy markets; (2) the pace of economic recovery taking place; and (3) the growing consumer interest in cleaner fuels, support our view for an improved demand environment for biodiesel and renewable diesel, as inventory drawdowns support suppliers.”

To this end, Dayal rates this stock a Buy. In a show of confidence, he puts his price target at $70, suggesting a robust growth potential of 85%. (To watch Dayal’s track record, click here)

Renewable Energy has a unanimous Strong Buy analyst consensus rating, based on 4 Buys set in recent weeks. The average price target is $55, and implies a 45% upside potential from the $37.90 current share price. (See REGI stock analysis on TipRanks)

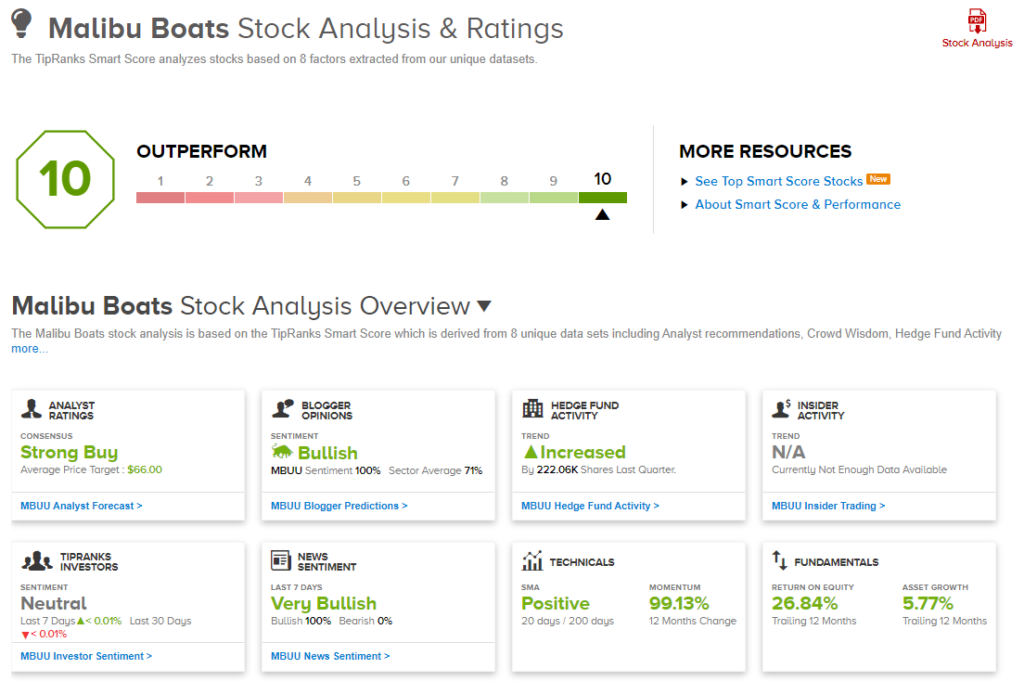

Malibu Boats (MBUU)

Last on our “perfect 10” list today is Malibu Boats, a manufacturer of recreational speedboats. The company bills itself as “the world’s largest manufacturer of watersports towboats.” Founded in California in the early 80s, Malibu Boats is now headquartered in Tennessee, with additional manufacturing facilities in Australia.

Malibu’s fiscal year 2020 came to an end with calendar Q2, and the company reported year-over-year drops in net sales and unit volume. The top line came in at $653.2 million, and the unit sales, or total boats sold, was 6,444. These numbers were down 4.5% and 12.5%, respectively. The decline was attributed to the coronavirus crisis and lockdown policies in the first half of the calendar year.

Overall, however, Malibu has not fared badly in the coronavirus pandemic. Earnings increased sequentially from the end of CY19 to 1Q20, and looking ahead, 3Q20 is expected to show another sequential EPS increase.

B.Riley FBR analyst Eric Wold is impressed with Malibu Boats, and upgrades the stock from Neutral to Buy. His new $75 price target implies that there’s room for 38% growth in the year ahead. (To watch Wold’s track record, click here)

To support his stance, Wold writes, “Even with obvious uncertainties around the COVID-19 situation and underlying demand that should return to more normalized levels, we are increasingly positive given soldout order books into 3Q21, depleted inventory that could take over a year to replenish and numerous profit-driving tailwinds to take numbers above our increased estimates.”

“In addition to margin efficiencies to be gained from improving production levels to replenish inventories (by adding production Fridays into heavier periods), we expect MBUU to benefit from the new Pursuit Boats facility (that could see a doubling of sales in 2-3 years), additional vertical integration efforts (flooring at Cobalt with 2-3 other projects behind that) and further Monsoon engine penetration,” the analyst added.

All in all, MBUU has 8 recent reviews, breaking down into 6 Buys and 2 Holds. This adds up to a Strong Buy consensus rating. The stock’s $66 average price target suggests a potential upside of 21% for the next 12 months. (See MBUU stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.