Markets are rising, and investors are looking to maximize their returns. While growth stocks are a natural choice in this environment, we should not ignore the dividend stocks. These shares, with their combination of natural price appreciation and dividend payouts, offer investors a sound choice for solid returns.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Dividend investing is usually seen as a defensive play, but it makes a sound choice in good times, too, as part of a balanced portfolio. The dividend payments ensure a steady income stream, always a plus, and add to the total return potential. And when the dividends are large, the rewards are higher.

Analyst Jason Stewart, from Janney Montgomery, has been picking out dividend stocks with a twist – these are shares that bring a combination of advantages to the table, including yields of 14% or better, and a monthly payment. With monthly dividends, investors can tap into the income stream more frequently, allowing for greater flexibility.

So let’s take a look at these two dividend picks from Janney, to find out just why the brokerage firm says to buy them now. We’ll also check in with the TipRanks data, to get a fuller picture of their prospects.

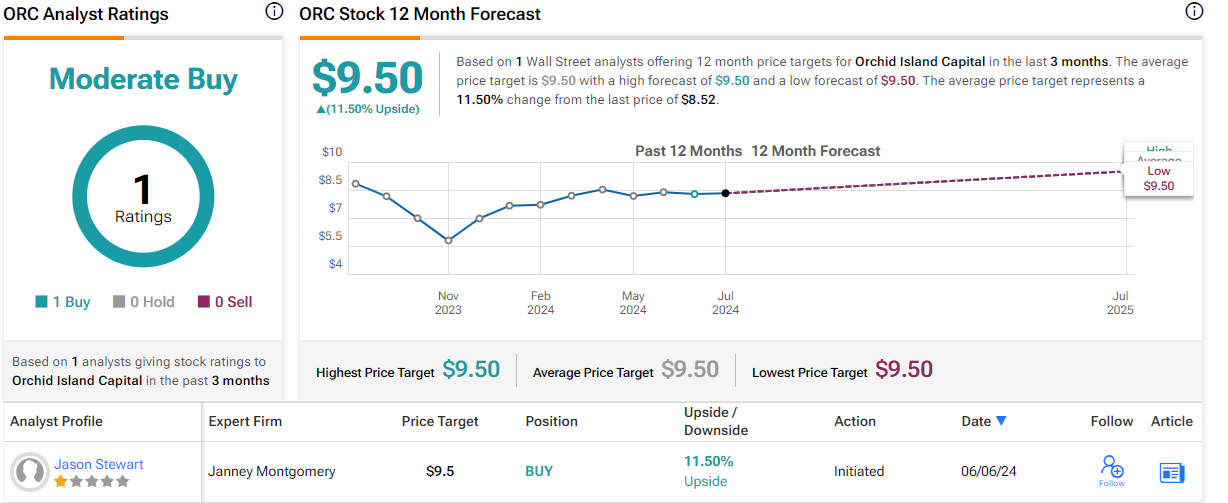

Orchid Island Capital (ORC)

The first stock we’ll look at here is Orchid Island Capital, a specialty finance company that invests heavily in the residential mortgage-backed securities market. The company is structured to act as a REIT, a real estate investment trust, for tax purposes – which leads directly to its status as a high-yield dividend payer. REITs are required by tax code regulations to return a certain percentage of profits directly to shareholders, and usually choose dividends as the mode of return.

Orchid Island has based its investment portfolio on traditional pass-through Agency RMBS and structured Agency RMBS, based on single-family residential mortgage loans and also including collateralized mortgage obligations and interest-only securities. According to the company’s own data, 30-year fixed-rate assets make up almost the entire portfolio, with interest rates ranging from 3% to 7%.

Based on this portfolio, Orchid Island realized a net income of $19.8 million in 1Q24, for an EPS figure of $0.38. The company’s earnings were 30 cents per share better than expected and were complemented by a liquidity position of $215.7 million, comprised of cash and cash equivalents.

The company’s monthly dividend payment is set at 12 cents per share – and so comes to 36 cents per share quarterly, or $1.44 annualized. At that rate, the dividend gives a hefty forward yield of almost 17%, far higher than the current rate of inflation and more than enough to guarantee a positive rate of return.

Turning to Janney’s Stewart, we find the analyst taking an upbeat view here, based on the company’s ability to capitalize on mortgage spreads and to return value to shareholders. He writes, “Mortgage spreads, which are the primary driver of book value, are wider than long-term averages and likely to tighten as fixed income volatility declines driving book value higher. Historically, investors have fared well capitalizing on government intervention as non-economic participants in markets and thematically we like increasing private capital investment in the agency MBS market. ORC’s diversified and liquid portfolio is well positioned to deliver long-term shareholder value in this environment.” (To watch Stewart’s track record, click here.)

Taking this view forward, Stewart initiates his coverage of the stock at a Buy, with a price target of $9.50, implying a one-year upside potential of 11.5%. With the dividend yield, this implies a total return of nearly 28.5%. Stewart’s is the only analyst review currently on file for ORC, which has a trading price of $8.52. (See Orchid Island’s stock forecast.)

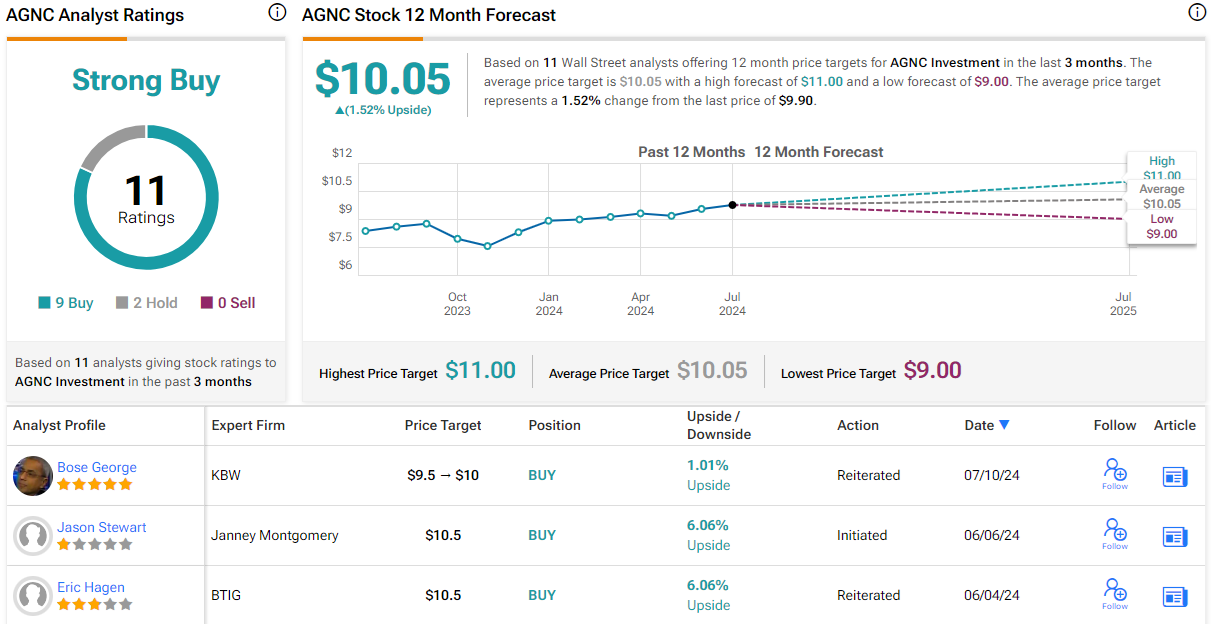

AGNC Investment (AGNC)

Next on our list is AGNC Investment, an internally managed REIT that focuses, like Orchid Island, on mortgage-backed securities. At the end of last year, AGNC had a portfolio valued at just over $60 billion, with $53.8 billion of that total being Agency MBS investments. As of the end of Q1 this year, the company’s portfolio has grown to $63.3 billion, with $53.7 billion of that, or 85%, being Agency MBS assets. Of the remainder, the bulk is in TBA Mortgages, which at $8.4 billion make up 13% of the current portfolio. Approximately 95% of AGNC’s investments are in 30-year fixed rate assets.

The company follows a risk-sensitive strategy in selecting assets for its portfolio and prides itself on providing capital for buyers in the US real estate market, allowing them to finance homes and facilitate the creation of wealth.

Getting to financial numbers, we find that AGNC reported a non-GAAP EPS in 1Q24 of 58 cents per common share. This figure was a penny better than expected, although it was down from the 70-cent EPS reported in 1Q23. The company also had a tangible net book value of $8.84 per common share, and reported unencumbered cash and Agency MBS of $5.4 billion.

For dividend investors, AGNC offers a 12-cent per month payment, or 36 cents per common share each quarter. The annualized rate of $1.44 gives a forward yield of 14.4%.

This is another stock covered by Janney Montgomery’s Jason Stewart, who sees the company as a solid choice in the REIT universe, writing, “AGNC’s diversified, liquid portfolio, cost-effective internal management structure, and focused risk-management approach make the stock the most liquid and efficient way to invest in the sector… AGNC is better positioned than most peers to deliver superior risk-adjusted returns versus peers with its flexible balance sheet profile and industry low operating cost.”

Stewart’s Buy rating comes along with a $10.50 price target that points toward a one-year gain of 6%. With the dividend yield added in, the total return here could reach more than 20% in the next 12 months.

Overall, the 11 recent analyst reviews on this stock, with their 9 to 2 breakdown favoring Buy over Hold, give the shares their Strong Buy consensus rating. However, the stock is currently trading for $9.9 and its $10.05 average target price implies the shares will remain rangebound for the time being. (See AGNC Investment’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.