Apple (NASDAQ:AAPL) investors look poised to head off to the weekend in high spirits. The shares are on track for one of their strongest days of the year so far, up nearly 5% as of writing, following the tech giant’s strong March quarter (FQ2) readout.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The company posted revenue of $111.18 billion, up 16.5% year-over-year, exceeding expectations by $1.6 billion, while EPS came in at $2.01, topping estimates by $0.07.

Looking ahead, Apple expects June quarter revenue to grow between 14% and 17% compared to the same period last year, well above analysts’ projections of 9.5% growth to $103 billion.

Outgoing CEO Tim Cook pointed to “extraordinary demand” for the iPhone 17 lineup as a key driver behind the company’s strongest-ever results for this time of year. iPhone revenue reached $57 billion, amounting to 22% YoY growth, supported in part by robust sales in China. Revenue from China totaled $20.5 billion, marking a 28% increase from a year earlier and building on a recent recovery trend.

While Apple continues to face rising memory chip costs tied to surging demand for AI data center buildouts, the company still managed to expand gross margins to 49.3%, up from 47% in the prior year.

The results elicited an unequivocal reaction from Morgan Stanley’s Eric Woodring, an analyst ranked among the top 3% on Wall Street. “Well, that was an impressive quarter and guide,” said the 5-star analyst. “We got the March quarter topline strength we expected, with June-quarter guidance reconfirming our expectations for >20% Y/Y iPhone growth for a 3rd consecutive quarter.”

Not only that, but there were also other notable positives: the high-margin Services came in well ahead of expectations, growing 16.3% YoY vs. the guide of around 14%, and June-quarter gross margin guidance of 47.5% to 48.5% was much stronger than expected despite the “significantly” higher memory costs.

Additionally, Woodring points out that on top of revenue and EPS growth accelerating to 16% and 20% YoY, respectively, in the first half of fiscal 2026, free cash flow rose by 64% YoY in the first half and is projected to increase 53% YoY for the full fiscal year, alongside annual capex of just $9 billion.

“Revs and profit strength are persisting, including a remarkable June qtr margin guide, leaving us more confident in AAPL’s ability to mitigate record cost inflation,” Woodring summed up. “A thematic Megacap winner (FCF +53% in FY26) in a product cycle with upside optionality at WWDC and Foldables on deck.”

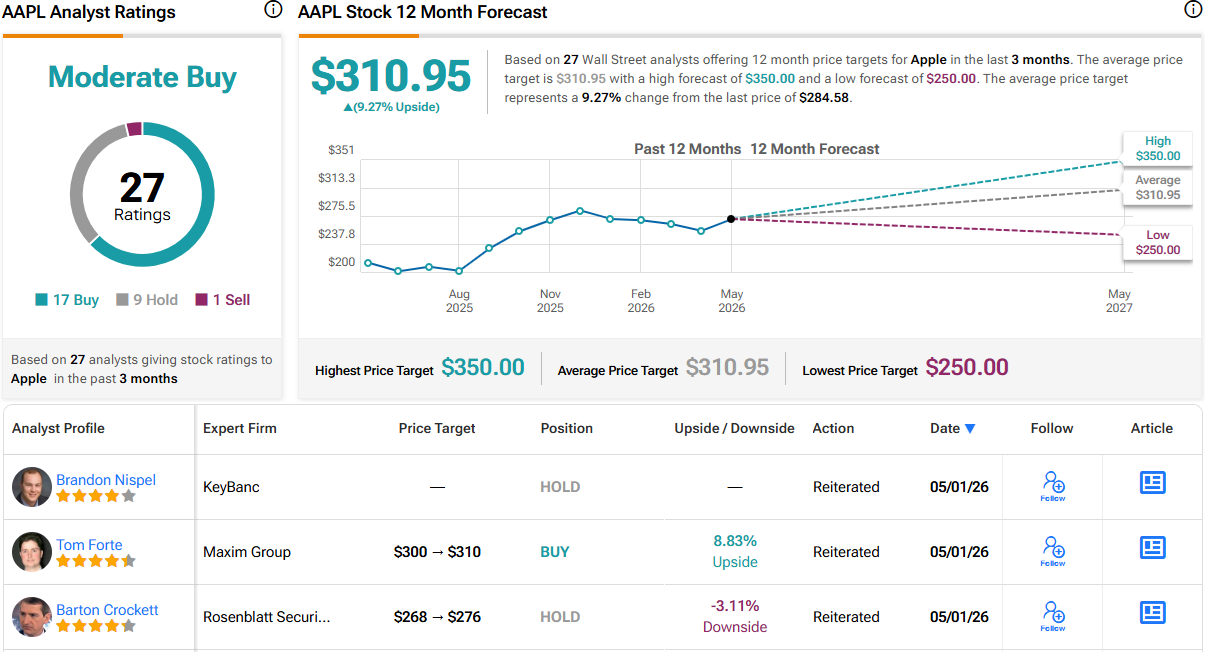

So, where does all that leave investors? Woodring maintained an Overweight (i.e., Buy) rating on the shares, while his price target goes from $315 to $330, implying the stock will gain 16% in the months ahead. (To watch Woodring’s track record, click here)

16 other analysts are also bullish on AAPL’s prospects, while an additional 9 Holds and 1 Sell all add up to a Moderate Buy consensus rating. Going by the $310.95 average target, a year from now, shares will be changing hands for a 9% premium. (See Apple stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.