Taiwan Semiconductor Manufacturing (TSM), the world’s largest manufacturer of AI chips, briefly reached a $1 trillion market cap last week, overtaking Tesla (TSLA) in market capitalization. Notably, the stock has gained 20% since I pointed out in April that TSM’s impending growth is being overlooked. I am still bullish on TSM, given multiple tailwinds of insatiable AI demand, various growth catalysts, its monopoly-like position in advanced microprocessors, and capacity expansion.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Multiple Catalysts Fostering Growth at TSM

TSM remains the key producer and supplier to AI stalwarts like Nvidia (NVDA), Advanced Micro Devices (AMD), Apple (AAPL), and Qualcomm (QCOM). Markedly, TSM is also the top manufacturer of NVDA’s latest line of advanced Blackwell chips.

High demand for manufacturing chips from these AI giants has led to TSM’s stock price gain recently. TSM will continue to benefit from strong AI demand as numerous industries continue to integrate AI into their business infrastructures.

Additionally, a cyclical recovery in demand for personal computers and robust momentum in AI chips will drive sales growth. Smartphone sales rose globally during the first quarter, leading to higher orders for mobile chips.

As a result, sales of handset chips for Apple’s iPhone as well as high-end Android phones have been higher than expected. As a result, TSM has fetched sizeable orders from a number of its top-notch clients including AMD, Apple, Broadcom (AVGO), etc.

Crucially, TSM said it will most likely increase the price of its chips being supplied to Nvidia. Given the incessant demand and supply constraints, the price increase could be significant. Better pricing will boost TSM’s margins in the coming quarters.

Positively, NVDA’s management is open to TSM’s price increases and has not commented against them. Therefore, other AI players will likely accept the price increase in the coming months.

Considering the surging demand, TSM will likely increase its capital spending to $37 billion, a 15% year-over-year increase from the $32 billion forecasted for 2024. TSM will utilize the additional spending toward capacity expansion and developing more advanced processes with higher computing power, like the 2-nanometer technology chips. Its 2nm technology is much awaited and is predicted to lead the industry with its advanced capabilities.

With the increased investments, TSM will ensure its market leadership in the manufacturing of AI chips. Competition is building up with peers like Samsung Electronics (GB:SMSN) and Intel (INTC) eyeing a bigger slice of the pie in the semiconductor foundry market. However, TSM’s scale and cutting-edge technology make it gain a clear industry-wide edge with a market share at over 60% versus a much lower market share for its closest competitor, Samsung, at 11%, according to Statista.

Importantly, TSM is making geographical diversification its key strategy. It is expanding into other international territories to reduce geopolitical risk. For instance, TSM launched its first chip factory in Kumamoto, Japan, to alleviate U.S.-China concerns. Production at the fabrication plant is expected to start by the end of 2024, while a second Japanese plant is also expected to begin construction around 2024-end.

Earlier this year, TSM received yet another boost in its manufacturing operations. The company received approval for direct federal funding worth $11.6 billion under the U.S. government’s CHIPS Act, as well as $6.6 billion in grants to expand its manufacturing facility in Phoenix, Arizona.

Given the above-mentioned factors, TSM is bound to benefit from robust AI demand, as the outlook for semiconductors remains bright.

Q2 Revenues and Earnings Expectations

On July 6, TSM announced that its May sales increased 30% year-over-year in local currency, though they were down 2.7% sequentially from April. For the June quarter, sales are expected to grow 32.9% year-over-year (down 9.5% sequentially). Combined, sales for the first half are expected to surge 28% year-over-year, beating analysts’ expectations.

On the EPS front, TSM is expected to report EPS of $1.50 for the second quarter. Markedly, TSM has a strong track record of beating the street’s EPS expectations for the past 11 quarters.

Ahead of TSM’s Q2 earnings expected tomorrow, many Wall Street analysts have already increased price targets on TSM. Further, TSM stock has a very positive signal from hedge fund managers, who added 5.8 million shares during the last quarter.

TSM Is Trading at an Attractive Valuation

In terms of its valuation, TSM looks cheap. Currently, it’s trading at an attractive forward P/E ratio of 26.7x compared to much higher multiples of its peer group. Semiconductor company Advanced Micro Devices is trading at a higher forward P/E multiple (52x), while the AI prodigy Nvidia is trading at a forward P/E of 47x.

Wall Street analysts expect TSM’s EPS to reach $8.20 in FY2025 (ending December). If TSM keeps the same forward P/E multiple by then, its share price will be about $219, around 28% higher than the current price. Therefore, it makes sense to consider buying TSM stock at current levels, given the strong growth potential in the AI space.

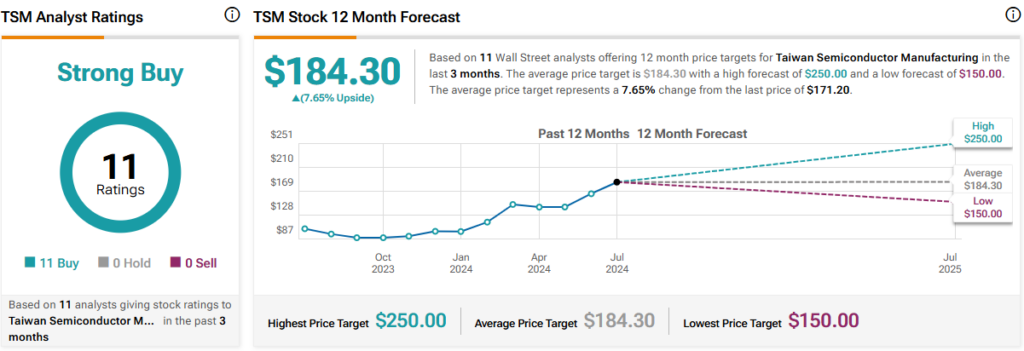

Is TSM a Buy, Sell, or Hold, According to Analysts?

The Wall Street community is clearly optimistic about Taiwan Semiconductor Manufacturing stock. Overall, the stock commands a Strong Buy consensus rating based on 11 unanimous Buys. However, TSM stock’s average price target of $184.30 implies 7.65% upside potential.

Conclusion: Consider TSM for the Long-Term AI Potential

A continuous uproar in demand for everything AI has led to significant demand for AI chips. TSM’s dominance in the manufacturing of AI chips remains undisputable, making it a key contributor as well as a direct beneficiary of the AI boom.

With its extensive capacity expansion plans and geographical diversification, highly anticipated 2-nm technology, and higher pricing, TSM is set on a growth trajectory for the next few years. Therefore, I will buy the stock at current levels.