SoFi Technologies (NASDAQ:SOFI) shares are going through a bit of a rough patch, having retreated by 43% from the highs reached last November.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

With the neobank set to report Q1 earnings before the open today (April 29), investors are obviously hoping the results will help the stock get back on an upward trajectory.

Looking ahead to the print, Truist analyst Matthew Coad thinks that with scrutiny rising around private credit, potential funding pressures, and higher loan retention following the December equity raise, the company will likely offer more detail on balance sheet trends for the rest of the year. Although SoFi has previously indicated that net interest margin will stay above 5%, investors are expected to push for more clarity around that outlook.

Management is also likely to highlight the rollout of its Business Banking segment, which introduces an “interesting set of products and capabilities,” including regulated business deposit accounts, real-time payments powered by SoFiUSD, and expanded support for digital assets. On the credit side, attention will turn to recent developments in securitizations, particularly after one of the LPB 2025 asset-backed securities (ABS) deals breached a cumulative net loss trigger, which Coad says “feeds into investor concerns on funding.” These LPB 2025 ABS transactions are pools of loans that SoFi packaged and sold to investors; when losses in the underlying loans exceed predefined thresholds, it can signal weaker credit performance and potentially affect investor confidence and funding costs.

Finally, Coad anticipates commentary around member growth beyond 2026, especially as the company works to sustain year-over-year growth above 30% in an increasingly competitive neobanking landscape, with players like Revolut and Nubank building a presence in the U.S. market.

As for the raw numbers, Coad is calling for Q1 adjusted net revenue of $1,049 million, representing 36% YoY growth compared with 37% in Q4, broadly consistent with both guidance and Street expectations. His diluted EPS estimate of $0.12 matches consensus, and also aligns with the guide.

Looking ahead, the analyst still believes that 30% adjusted net revenue growth remains within reach in 2026, with his forecast landing at $4.64 billion (29% YoY) vs. the Street at $4.66 billion (30%). That said, Coad flags potential headwinds, including net interest margin compression driven by a shift in mix toward lower-yielding student loans, as well as softer origination growth as the company increases loan retention.

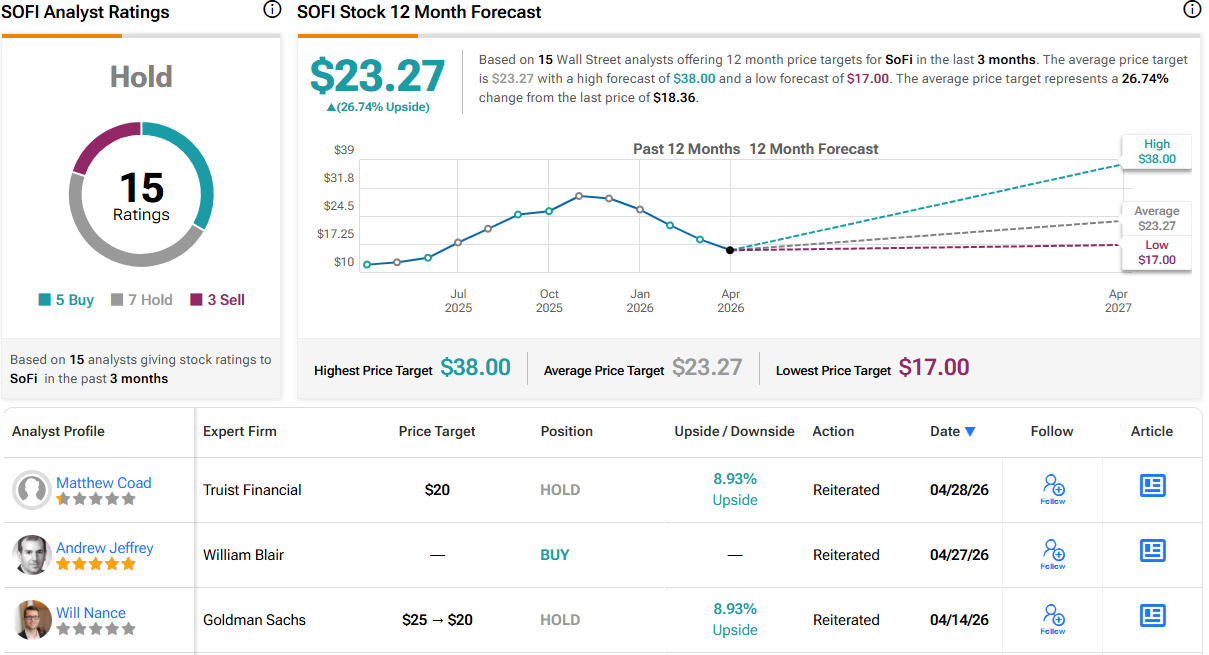

Bottom line, Coad maintained a Hold (i.e., Neutral) rating on the shares and lowered his price target from $21 to $20, implying the stock will now gain 9% in the months ahead. (To watch Coad’s track record, click here)

6 other analysts join Coad on the sidelines, while an additional 5 Buys and 3 Sells still add up to a Hold consensus rating. At $23.27, the average target points toward one-year gains of 27%. (See SOFI stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.