ServiceNow (NYSE:NOW) stock might be out of fashion right now, caught up in what’s been dubbed the SaaSocalypse, reflecting concerns that AI agents could render software companies irrelevant. Its recent quarterly results, while generally strong, were also given the thumbs down by investors due to a combination of a 75-basis-point drag on subscription revenue, driven by delays in large on-premise deals in the Middle East, and an outlook for contract growth that came in below expectations. On top of that, the Armis acquisition and ongoing AI infrastructure spending are expected to weigh on margins through 2026. All the above has resulted in a stock that has shed 41% year-to-date.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

However, having attended the company’s investor day in Las Vegas on Monday, D.A. Davidson analyst Gil Luria left impressed with what is in the pipeline. “We came away with greater clarity on ServiceNow’s view of its market position in AI moving forward,” Luria said. “The event provided incremental details on NOW’s AI pricing model and where it has a right to win around future agentic use cases. ServiceNow remains a long-term share gainer in our view.”

The company outlined new long-term financial goals targeting more than $30 billion in subscription revenue by FY30, while positioning the rule of 60 – where revenue growth plus profit margin equals 60% – as a baseline outcome for investors. It also presented an upside case of $32 billion, with CEO Bill McDermott saying he is “very bullish” on the company’s future, and indicating a preference to “guide even higher.”

The company highlighted three primary “growth drivers” – Security, CRM, and Data & Analytics – each seen as capable of delivering around 25% compounded growth. Management stressed that the fiscal 2030 targets exclude large-scale M&A, with capital allocation focused first on organic expansion, while smaller tuck-in deals will continue to play a role in expanding TAMs (total addressable markets) and advancing the product roadmap.

Meanwhile, margin improvement is expected to be supported by internal AI adoption. Headcount should stay flat in FY26 alongside an estimated $300 million in annualized cost savings from agentic AI. As such, FY27 free cash flow and operating margins are both expected to increase by 100 basis points.

NOW also indicated that ServiceNow AI ACV (annual contract value) could account for roughly 30% of the total by FY30, or about $9 billion, while AI consumption revenue, previously guided at $1 billion, is now expected to reach $1.5 billion in fiscal 2026. The fiscal 2030 targets incorporate “conservative assumptions” for AI adoption to follow a trajectory similar to Pro historically, despite currently exceeding that pace.

So, down to the nitty-gritty, what does all this ultimately mean for investors? Luria maintained a Buy rating on the shares, alongside a Street-high $190 price target. That figure points to 12-month returns of 108%.

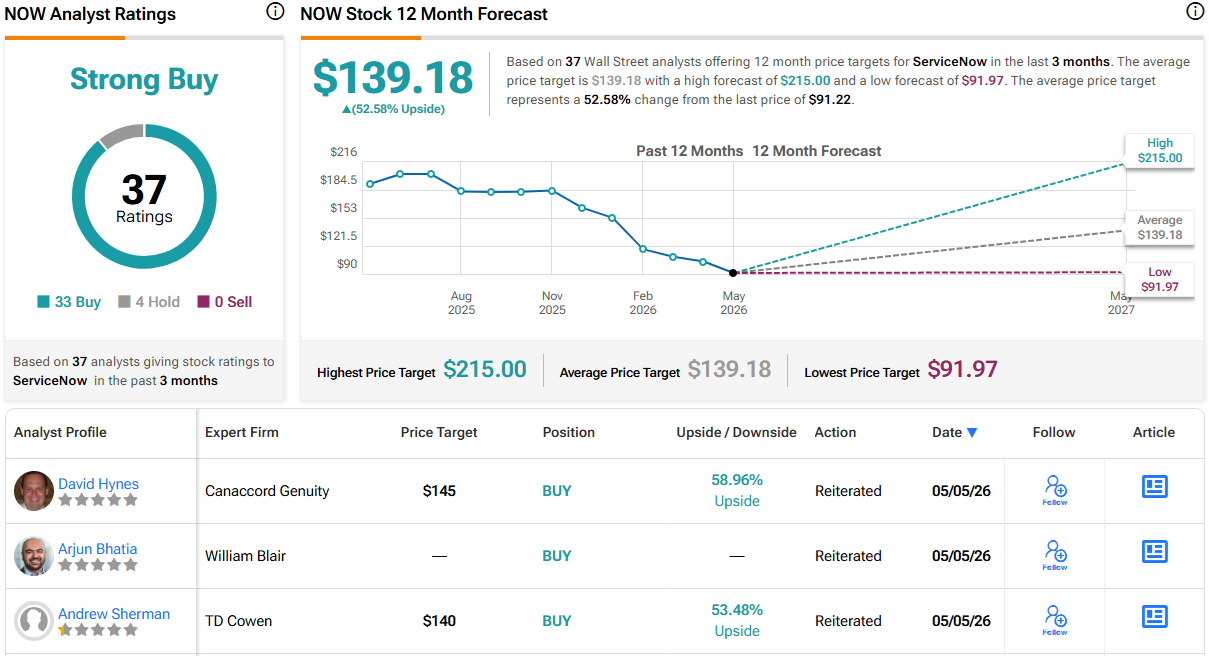

Most other analysts are bullish too. Based on a mix of 33 Buys vs. 4 Holds, the stock claims a Strong Buy consensus rating. Going by the $139.18 average target, a year from now, shares will be changing hands for a 52% premium. (See NOW stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.