As the global shift away from fossil fuels accelerates, one constraint is becoming clear – clean energy also needs to be reliable. That’s where nuclear stands out, offering steady, around-the-clock output without the intermittency of solar and wind or the geographic limits of hydro, while its long-term safety record looks stronger than often assumed.

Meet Samuel – Your Personal Investing Prophet

Two ETFs to trade SMR long or short: SMU & SMZAround 75 reactors are currently under construction globally, with plans for more than 100 additional projects, including roughly 25 in the US. Policy is moving in the same direction, too, with the Trump administration supporting domestic nuclear development, adding another layer of momentum to the industry’s outlook.

With that backdrop taking shape, HSBC analyst Samantha Hoh has zeroed in on two emerging players in the field – Oklo (NYSE:OKLO) and NuScale Power (NYSE:SMR) – and has picked her top name for the near term. Let’s dive in.

Oklo, Inc.

The first stock we’ll look at, Oklo, is a company based in Santa Clara, California. Oklo works on advanced nuclear power reactors, developing new fission technology and new methods for recycling nuclear fuels. The company’s goal is to develop and deploy power plants, based on the latest and most efficient nuclear technologies, to provide electric energy that is clean, reliable, and affordable – and available at any scale.

The US Department of Energy (DOE) has programs to promote such technology, including the Reactor Pilot Program (RPP) and the Fuel Line Pilot Program (FLPP), and Oklo is involved with both of them. The RPP was announced last summer, and its goal to speed up the testing of advanced reactor designs aligns perfectly with Oklo’s business model.

Oklo focuses on fast-reactor design, using liquid-metal cooling and metal fuels, and with the capacity to use nuclear waste as fuel. The base technology is not new, but it is known to be one of the safest nuclear reactor technologies. In March of this year, Oklo received DOE approval for the safety design agreements on two projects, the Aurora powerhouse at the Idaho National Laboratory and the Atomic Alchemy Groves Isotopes Test Reactor in Texas.

Oklo currently has several projects under way, under the auspices of the DOE’s programs. While it is still a pre-revenue company, the years 2024 and 2025 marked a shift in Oklo’s stance, as the reactor developer moved product development to project deployment. To back this shift, and its ongoing work in gaining regulatory approvals and building reactors, Oklo has deep pockets – the company finished 2025 with $1.4 billion in cash and other liquid assets.

This strong foundation is what caught analyst Hoh’s eye, and she writes of Oklo, “With a total of four projects selected to participate in the Department of Energy’s (DOE) Reactor Pilot Program (RPP) and Fuel Line Pilot Program (FLPP), Oklo is positioned to leverage the new DOE-led licensing process for its 75 MW Aurora powerhouses and fuel foundry. The result is an accelerated timeline for constructing and licensing new reactors, with Oklo leveraging its expertise in ancillary opportunities of nuclear fuel recycling and radioisotopes production…”

Looking ahead, Hoh notes Oklo’s cash position, which has improved since last year, and outlines the company’s projected path, saying, “With no debt and approximately USD2.5bn in cash and equivalents, Oklo expects to book its first revenue later this year from the Idaho Radiochemistry Laboratory. The company is offsetting high upfront first-of-a-kind (FOAK) capital costs with customer pre-payments and third party investments, guiding to USD400m of annual capex over the next two years. Longer-term Oklo should be able to finance capex with multiple forms of financing including project financing against LT PPAs and federal loans. The company should also benefit from economies of scale and a vertically integrated fuels business.”

Bottom line, Hoh puts a Buy rating on OKLO shares, along with a $96 price target that suggests a one-year upside potential of 35%. (To watch Hoh’s track record, click here)

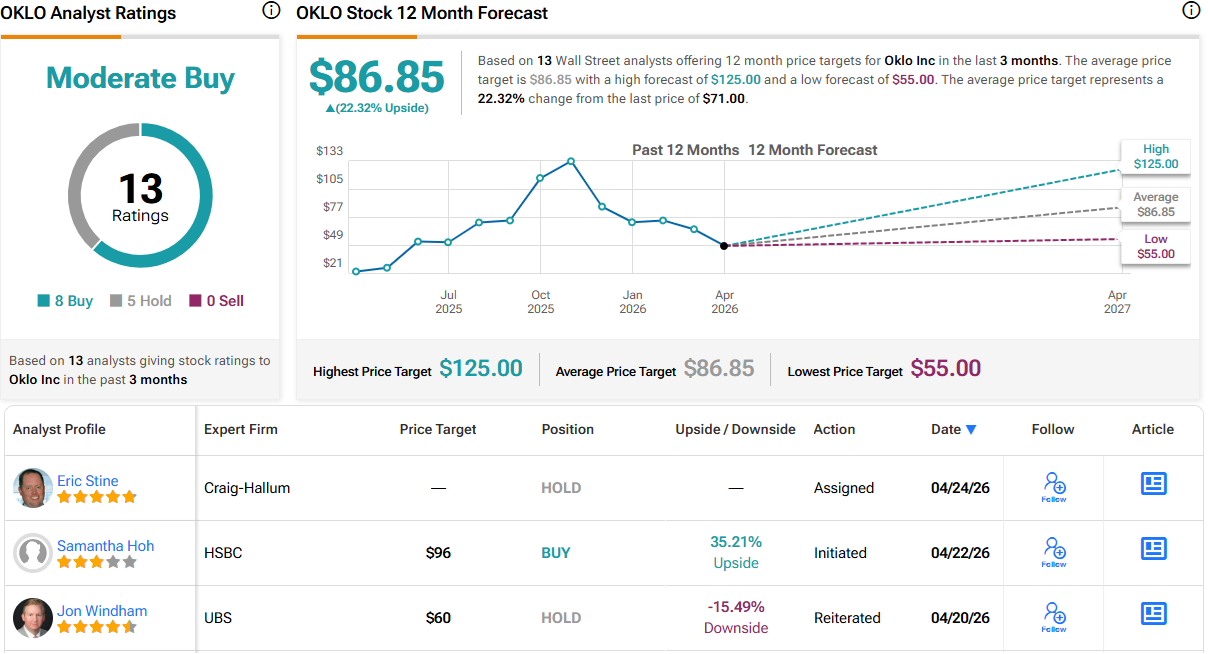

Overall, this stock holds a Moderate Buy consensus rating from the Street’s analysts, based on 13 recent reviews that include 8 Buys and 5 Holds. The shares are priced at $71, and their $86.85 average price target points to a 22% upside on the one-year horizon. (See OKLO stock forecast)

NuScale Power

The next stock that HSBC looked at was NuScale Power, a company focused on the development and deployment of small modular reactor, or SMR, technology. This is exactly what it sounds like: a nuclear power technology based on self-contained modular units that can be linked in tandem to scale the power deployment for any need. NuScale’s program is ambitious, and it is based on a 77-megawatt unit, housed in a 76-foot by 15-foot cylindrical containment vessel that includes the reactor and the steam vessel and weighs just 700 tons. NuScale’s reactor module is designed for easy portability and can be shipped in three segments by rail, truck, or barge.

Like Oklo above, NuScale has been successful in securing various regulatory approvals for its reactor designs, plans, and deployments. In May of last year, NuScale announced that its current reactor design, the uprated 77 MWe unit, had received design approval from the U.S. Nuclear Regulatory Commission (NRC), and remains on track for deployment by 2030. This was followed in September by the announcement that NuScale had entered a partnership with the Tennessee Valley Authority (TVA) and ENTRA1 Energy for an SMR deployment to reach up to 6 gigawatts. And finally, in February of this year, Nuclearelectrica, the Romanian nuclear reactor operator, made its final investment decision on its SMR project – and selected NuScale to provide up to 6 modules at the proposed Doicești reactor site.

NuScale’s stock has seen heavy losses in recent times and is down 69% over the past 6 months. The share price decline got rolling last fall, when the global construction and fabrication engineering company Fluor, a major stakeholder in NuScale, sold 71 million shares of its position in the company. Fluor realized $1.35 billion from the sale and retained 40 million shares and its partnership activities – but NuScale’s share price has not meaningfully recovered yet.

The reactor company did finish last year with $1.3 billion worth of available capital to support its operations. This is an important point, as NuScle is currently in a pre-commercial phase of operations and does not have a regular revenue stream.

HSBC’s Samantha Hoh is upbeat about NuScale’s technology and regulatory approvals, but expresses concerns about the company’s ability to maintain its capital position. She says, in her recent note, “NuScale has received US NRC standard design approvals (SDA) for both its 50 MW and uprated 77 MW modules, which materially derisks its small modular reactor (SMR) for global deployment. The regulatory lead enhances project bankability and positions NuScale to capture both domestic and international opportunities amid rising power demand from AI data centers. However, NuScale’s capital light model of licensing its technology and providing pre-and-post construction services puts them at the mercy of customers in terms of the pace of execution.”

Hoh adds to that her comments on current projects, writing, “While NuScale books pre- construction service revenue from the Romania project this year, the company may be required to provide a second milestone contribution to ENTRA 1 as it advances a power purchase agreement with the Tennessee Valley Authority (TVA). The agreement to deploy up to 6 GW of new nuclear power generation capacity bolsters NuScale’s US deployment prospects and should drive steady revenue longer term, but may require NuScale to raise additional upfront capital for higher G&A costs.”

Following from these comments, Hoh rates SMR as a Hold. Nevertheless, her $13 price target implies an upside of 9% for the coming year.

SMR’s current Moderate Buy consensus rating is based on 14 reviews, with a breakdown of 6 Buys, 7 Holds, and 1 Sell. The stock is priced at $11.96, and its $16.91 average price target is a bullish one, indicating a 41% upside potential by this time next year. (See SMR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.