The week has just begun but Wall Street is already looking ahead to later in the week. That’s because when the market action comes to an end on Wednesday (May 20), Nvidia (NASDAQ:NVDA) will dial in its fiscal first-quarter results (April quarter).

Meet Samuel – Your Personal Investing Prophet

Explore NVDS for 2X short leverage on NVDAAs the market’s biggest name, the report carries a lot of weight and will point to trends in the AI chip world, giving a sense of where demand is heading and how AI infrastructure spending is evolving.

Nvidia has made a habit of beating expectations in its quarterly readouts, and according to KeyBanc’s John Vinh, an analyst who ranks among the top 1% on Wall Street, more of the same will be on deck this time around. “We expect NVDA to report strong results and guidance driven primarily by increased demand for Blackwell Ultra GPUs and initial shipments of Rubin GPUs,” the 5-star analyst said.

Vinh anticipates Blackwell GPU shipments will rise by 150,000–200,000 quarter-over-quarter, which would translate into sequential revenue growth of $5 billion-$7 billion. Supply chain checks suggest Rubin will start ramping in fiscal Q2, with the R200 expected to add about $3 billion-$4 billion in incremental revenue. Meanwhile, despite early issues with Samsung and Micron scaling HBM4, supply and yields are said to be improving, and the analyst expects Nvidia will ship 1.7-1.8 million Rubin GPUs this year.

Given the timing of the recent China H200 approvals (in mid-May, the U.S. government granted licenses enabling Nvidia to sell H200 AI chips to around 10 Chinese tech firms, including Alibaba and ByteDance), Vinh anticipates the Q2 guide won’t include any contribution from China, though management is likely to offer a range for the potential upside. Approval for 10 Chinese customers at 75,000 chips each would suggest roughly $13 billion-$14 billion in revenue, which the analyst thinks will be booked across several quarters.

Vinh also sees Nvidia using Computex (June 1-5) to announce Vera CPU racks (256 CPUs per rack) aimed at agentic AI workloads, with shipments expected to begin in the second half of the year. At around 5,000 racks shipped in the second half, he estimates this could contribute $1.5 billion-$2 billion in revenue.

As for the numbers, Vinh has now raised his fiscal Q1 and Q2 revenue estimates from $78.1 billion and $84.9 billion to $80.8 billion and $89.5 billion, compared with consensus at $78.8 billion and $86.9 billion.

That takes Vinh’s fiscal 2027 revenue and EPS estimates from $365 billion and $8.24 to $383 billion and $8.71, vs. the Street at $370 billion and $8.42.

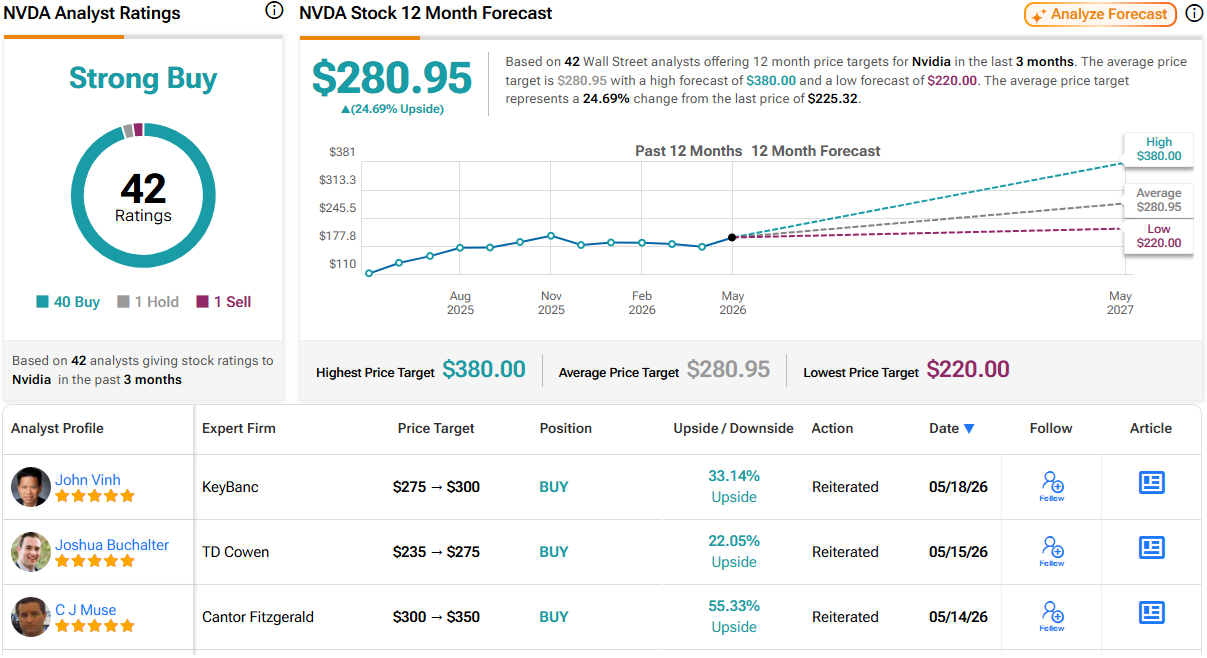

So, what does that ultimately mean for investors? Vinh maintained an Overweight (i.e., Buy) rating on the shares and raised his price target from $275 to $300, implying the stock will gain 33% over the coming months. (To watch Vinh’s track record, click here)

Nvidia gets strong support elsewhere on the Street. Based on an additional 39 Buys vs. 1 Hold and Sell, each, the stock claims a Strong Buy consensus rating. The forecast calls for 12-month returns of 25%, considering the average target clocks in at $280.95. (See Nvidia stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.