The airline industry presents investors with an interesting set of choices. The industry’s biggest names are also among the market’s blue-chip names, while smaller, regional airlines may offer sound opportunities for investors willing to take on some added risk on airline stocks.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The key to finding these lesser-known names lies in abandoning a US-centric approach and looking at secondary markets in the airline world. Latin America, with a total population near 665 million and its rising middle class, is one of those potentially rich secondary airline markets.

That’s the underlying theory behind a recent report from Morgan Stanley on the transportation sector in Latin America, a sector that includes the region’s airlines. Analyst Jens Spiess explains these airlines’ underlying strength, saying, “Most airlines in Latin America have emerged stronger from the pandemic, as air travel has mostly recovered close to pre-pandemic levels… The airline industry is notoriously competitive, in particular because airlines only incur marginal costs to occupy seats that would otherwise remain empty. As supply constraints are set to persist over in 2024 and 2025, we expect the airlines under our coverage to sustain above average profitability levels.”

The analyst looks forward from these comments to detail the ‘attractive entry point’ that 2 Latin American airline stocks are offering investors right now. A look into the data, drawn from the TipRanks platform, bears this out; both stocks feature Strong Buy ratings from the analyst consensus, along with solid upside potential. Here are the details and the Morgan Stanley commentaries.

Volaris (VLRS)

We’ll first head to Mexico, where Volaris is based. This company is a leading discount airline in the Mexican air travel market, with operations extending into the US, Central, and South America. Volaris offers customers low-fare tickets with quality service, and holds an impressive 42% market share in Mexico’s domestic airline sector. The company is its home country’s largest airline, calculated by passengers transported.

Earlier this month, Volaris reported its April 2024 traffic results, a set of key metrics for an airline, and one of particular interest as the company is heading toward the summer high season. The company reported sharp declines year-over-year in Revenue Passenger Miles (RPMs) and Available Seat Miles (ASMs), attributed to an accelerated schedule of Pratt & Whitney engine inspections and consequent aircraft groundings. For April, RPM came to 2.24 billion, along with ASM of 2.64 billion. These figures were down 21% and 20% respectively. The airline reported carrying 2.3 million passengers during the month.

While the key metrics were down in April, kicking off Q2, the company’s 1Q24 report showed sound financial results. Revenue in the first quarter came to $768 million, up 5% year-over-year and beating the forecast by nearly $66 million. The bottom line figure, expressed as a GAAP EPS per American Depositary Share (APD) was 29 cents, 36 cents better than had been anticipated.

We should note here that Volaris shares have been on a downward trajectory over the past year. In the last 12 months, the stock is down approximately 41%, and the year-to-date decline clocks in at 15%. This makes the stock a serious underperformer compared to the S&P 500, which is up 26% in the last 12 months and 11% for 2024 so far.

Turning now to the Morgan Stanley view, expressed by analyst Jens Spiess, we find him laying out a simple outlook for the stock: a reduced share price for a company with sound prospects. He writes, “…. we see an attractive entry-point amid a challenging outlook. We believe the stock has reached deep-value territory. At 3.4x our 2025e EBITDAR, the stock is trading well below its historical average of 4.7x. While we acknowledge that the company will face fleet capacity constraints in 2024 and 2025 due to its exposure to GTF groundings, we see upside to consensus estimates as we think the market is underappreciated the favorable market conditions and the implication these will have on Volaris’s P&L.”

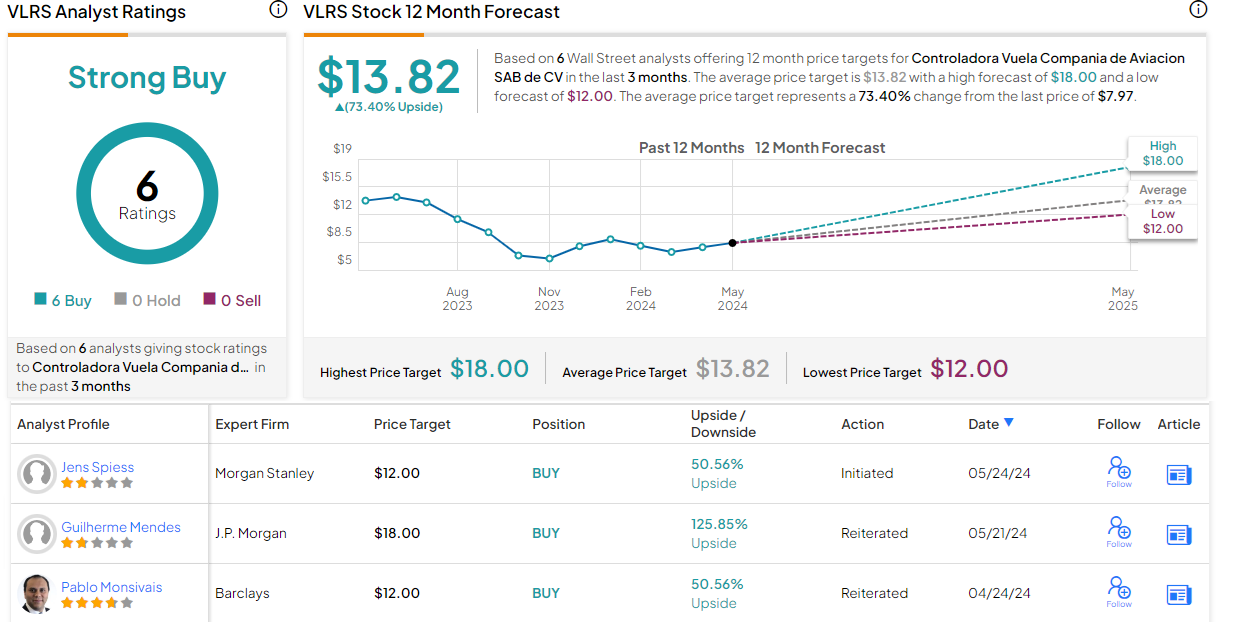

Unsurprisingly, Spiess rates VLRS shares as Overweight (Buy), with a $12 price target that implies a 50.5% upside potential on the one-year time horizon. (To watch Spiess’s track record, click here)

Volaris holds a Strong Buy consensus rating from the Street, based on a unanimous 6 positive analyst reviews set in recent weeks. The shares are priced at $7.97, and their $13.82 average price target suggests a robust 73% one-year upside potential. (See Volaris’ stock forecast)

Copa Holdings (CPA)

The second stock on our list is Copa Holdings, one of Latin America’s major discount airlines. The company acts as a holding firm, and through its subsidiaries, Copa Airlines and Wingo, is an important provider of passenger and cargo air services throughout the Latin American region. Copa Airlines is based in Panama, a strategic central location from which it offers over 300 daily flights to more than 70 cities in 32 countries across North, Central, and South America, and the Caribbean. In addition, Copa had code agreements with several other airlines, including the industry legacy carrier UAL, under which it provides access to another 180 destinations. Wingo, the smaller subsidiary, is a low-cost regional carrier based in and around Colombia.

On the key metrics, Copa reported 2.09 billion RPM for April 2024, up 11% year-over-year, and 2.42 billion ASM for the same period, up more than 9% from April 2023. These figures are system-wide, based on all of Copa’s passenger services. There is some worry about the company’s future passenger metrics, as the company relies on an all-Boeing fleet and has made significant purchase commitments for 66 late-model 737 MAX aircraft – the models under investigation for recent safety incidents – for delivery between 2023 and 2028.

Closely following the release of the April traffic numbers, Copa beat expectations with its 1Q24 financial results. The company generated a top line in the quarter of $893.5 million, up 3% from the prior-year quarter and beating the estimates by over $21.7 million. The company declared earnings of $4.19 per share by non-GAAP measures, a full 86 cents per share better than the forecast.

For return-minded investors, it’s important to note that on May 15, Copa Holdings declared its most recent dividend payment, at $1.61 per share for a June 14 payment. The dividend annualizes to $6.44 per common share and gives a strong forward yield of 6.51%.

In his coverage of this stock for Morgan Stanely, Spiess likes what he sees of the company’s longer-term potential, writing of CPA, “We expect Copa, the only FSC (full-service carrier) in our coverage, to continue benefitting from strong demand for international travel and premium offerings. Medium to long term, delivery delays of MAX-9s pose a risk to our passenger estimates, but we think the impact to earnings would be minimal from this given the incremental tightness it would place on capacity growth. On our 2025e EBITDAR, the stock is trading well below its pre-pandemic average of 7.3x.”

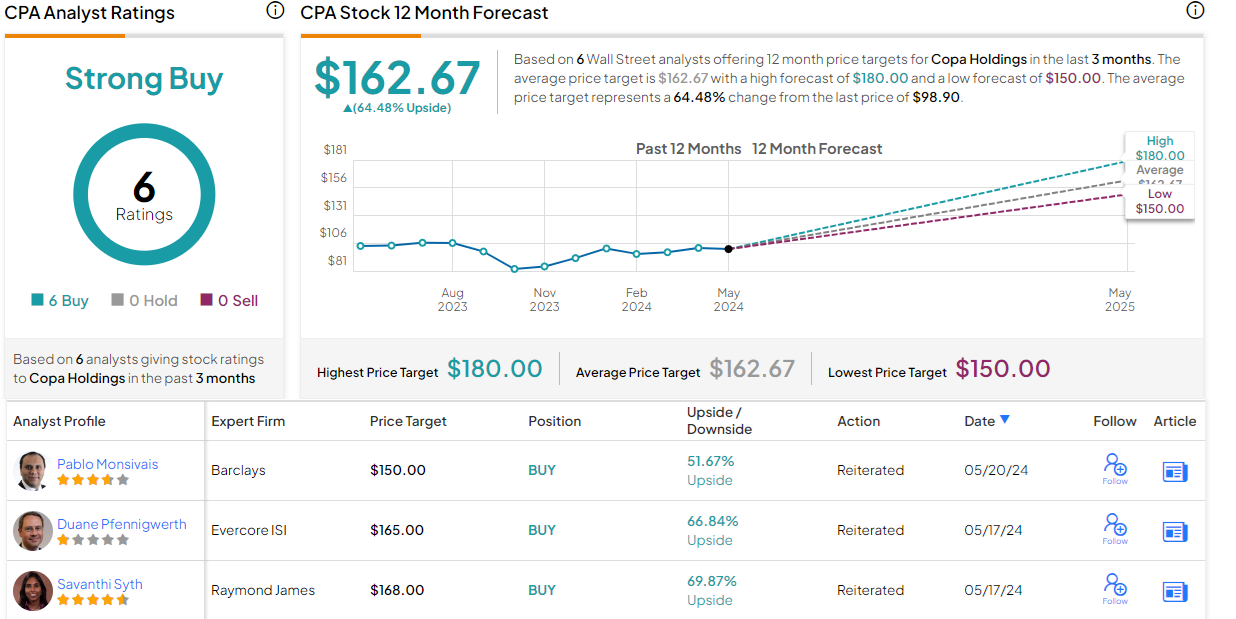

Quantifying this stance, Spiess rates CPA shares as Overweight (i.e. Buy) and names the stock as a Top Pick. His price target, at $140, points toward a 41.5% potential gain in the coming year.

Copa Holdings is another stock with a Strong Buy consensus rating, also based on 6 unanimously positive recent analyst recommendations. The shares have a current trading price of $98.90 and their $162.67 average target price is even more bullish than the Morgan Stanley analyst allows, suggesting a 64.5% share appreciation in the next 12 months. (See CPA stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.