We’re now just days away from the ’24 elections, and what a race it’s been. Polls have been all over the place, and both parties can make legitimate claims to holding the advantage as we approach Tuesday’s vote.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Amidst the political drama, the stock market has remained robust, with the S&P 500 surging 20% year-to-date. Historically, the index tends to perform well in election years, but this year has been exceptional, making it the most bullish election-year market in decades. A mix of macroeconomic factors, especially expectations of further Fed rate cuts, has fueled strong investor confidence.

Morgan Stanley’s analysts are embracing this momentum, picking out stocks they believe are primed for gains regardless of the election outcome. They’ve zeroed in on two specific stocks poised for substantial growth in the coming year – including one with a potential upside as high as 670%.

As if that weren’t compelling enough, according to the TipRanks database, both stocks are also rated as Strong Buys by the analyst consensus. Let’s see what’s driving this optimism among market experts.

Tenaya Therapeutics (TNYA)

We’ll start with Tenaya Therapeutics, a research-oriented biopharmaceutical company that is focused on developing and producing new therapeutic drugs for the treatment of heart disease. Tenaya is targeting its approach on the underlying causes of heart disease, including rare genetic disorders. The company’s approach includes gene therapies, cellular regeneration, and precision medicines.

Heart disease is the world’s leading cause of death among adults, making its treatment an important niche. Tenaya currently has two primary drug candidates under investigation, TN-201 and TN-401, for the treatment of MYBPC3-associated hypertrophic cardiomyopathy and PKP2-associated arrhythmogenic right ventricular cardiomyopathy, respectively.

The leading candidate, TN-201, is currently undergoing a Phase 1b human clinical trial. The study is focused on safety and tolerability and will enroll up to 24 adults. Data from the first patient cohort in the study are expected to be released in December, presenting a significant milestone for the stock. Meanwhile, enrollment is ongoing for the second cohort.

The second candidate, TN-401, entered its Phase 1 RIDGE-1 trial earlier this year. This global, open-label, dose-escalation study, which will continue patient dosing through Q4 2024, aims to evaluate the safety, tolerability, and effectiveness of a single intravenous dose of TN-401.

Morgan Stanley analyst Michael Ulz views TNYA as a compelling investment, with TN-201 as the primary value driver. Ulz notes, “Interim Ph1b MyPEAK-1 data for TN-201 in nHCM are expected in [December] and represent a key catalyst for Tenaya’s lead program. We see a favorable risk/reward on initial data, which could provide early de-risking, followed by more robust data in 2025.”

“We view favorable trends on cardiac biomarkers and uninterpretable protein expression data as the most likely scenario,” Ulz added. “We believe investors would view the data as positive and suggestive of benefit… Under this scenario we would expect TNYA shares to trade up +100%.”

To this end, Ulz rates TNYA shares an Overweight (i.e. Buy), while his $15 price target offers a whopping ~670% upside from current levels. (To watch Ulz’s track record, click here)

The consensus view here shows that Morgan Stanley’s bullish take is no outlier. TNYA stock has a unanimous Strong Buy consensus rating, based on 7 recent positive analyst reviews. The stock’s $1.94 trading price and $20.20 average target price together suggest an impressive upside of 941% on the 12-month horizon. (See TNYA stock forecast)

Royalty Pharma (RPRX)

The next Morgan Stanley pick we’ll look at is Royalty Pharma, a company that gives investors an interesting way to put money into the biotech sector. Royalty Pharma operates as a royalty company; that is, it purchases ownership rights in biopharmaceutical products and earns royalties on sales and profits. Royalty Pharma has built up a pipeline of such opportunities, designed to generate and maintain a steady stream of revenues.

This royalty strategy has led the company to put together a solid portfolio of assets. Royalty Pharma boasts rights in more than 35 approved products, and backs that up with rights in another 17 drug candidates still in the development stage. Of this total lineup, 15 products are considered ‘blockbusters,’ generating more than $1 billion in annual sales. And for the long term, the company’s portfolio has an average duration of 13 years. In the five-year period from 2018 to 2023, Royalty Pharma deployed an average annual capital of $2 billion, and in calendar year 2023, Royalty Pharma brought in $3 billion in total portfolio receipts.

In its last reported quarter (2Q24), Royalty Pharma reported portfolio receipts (revenue) of $608 million, marking a 12% year-over-year increase, though this came in $18 million below consensus. The company raised its 2024 portfolio receipts guidance to a range of $2.7 billion to $2.775 billion, up from a previous forecast of $2.6 to $2.7 billion. Additionally, the company posted an EPS of $0.96, reflecting a 13% increase year-over-year, slightly shy of the consensus estimate of $0.99.

Checking in with the Morgan Stanley view, we find analyst Terence Flynn taking an upbeat view of the company and its prospects for the long-term.

“RPRX has one of the highest top line growth rates in our coverage and is trading at a discount. In our view the company’s growth profile and diversified portfolio deserves at least an in-line multiple and hence our Overweight rating. We acknowledge that RPRX must continue to deploy capital towards new deals given patent/royalty expiries in order to sustain HSD growth, but management has a strong historical track record on this front. We see two areas of potential upside to estimates that could meaningfully move the needle – AMGN’s Olpasiran/ NOVN’s Pelacarsen for ACVD and JNJ’s Tremfya for psoriasis/IBD,” Flynn opined.

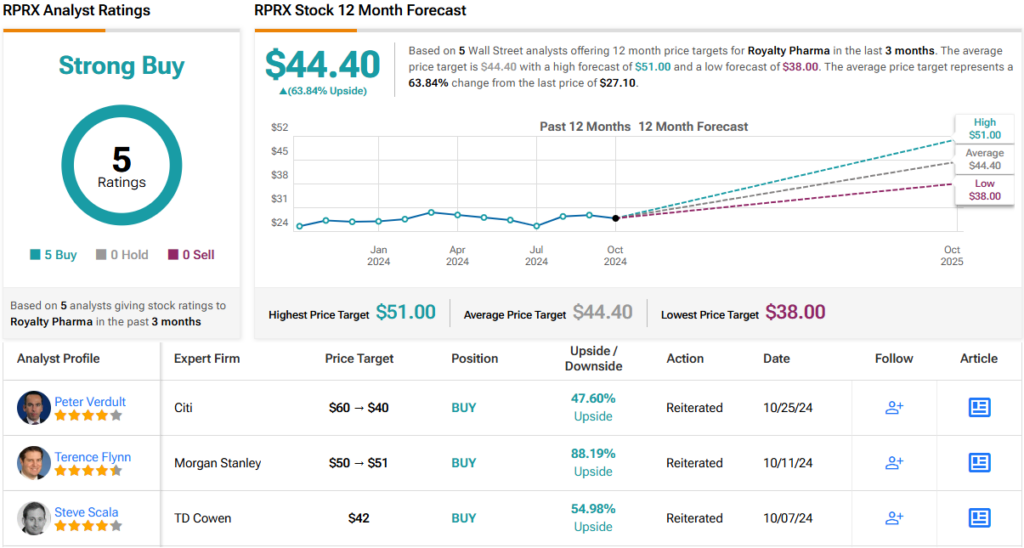

Flynn’s Overweight (i.e. Buy) rating is backed by a $51 price target, suggesting a potential one-year upside of 88%. (To watch Flynn’s track record, click here)

Morgan Stanley isn’t alone in this positive outlook. Royalty Pharma enjoys unanimous support, with 5 Buy ratings and a Strong Buy consensus. Currently priced at $27.10, the stock’s average price target of $44.40 implies a ~64% upside in the coming months. (See RPRX stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.