Computer memory makers are some of the hottest names on the market right now, enjoying unprecedented AI-driven tailwinds. Micron (NASDAQ:MU) and SanDisk (NASDAQ:SNDK) operate in the space in different capacities but both share two similarities. The two companies have experienced incredible real-world growth that has been accompanied by massive stock market gains. The former has seen its share price explode by 695% over the past year, although those massive gains look rather puny when compared to the latter’s humongous 4,057% growth.

Claim 55% Off TipRanks

New trading tool for SNDK bullsWhile no doubt such returns would normally give investors reason to be wary of the future trajectory, such are the strength of the industry tailwinds driving the gains, Mizuho’s Vijay Rakesh, an analyst ranked in 5th spot among the thousands of Wall Street stock experts, has just made upward revisions for both.

Rakesh now expects Micron’s F26/27/28E HBM revenue to reach $19.1 billion, $30.7 billion, and $35.7 billion, respectively, all some distance above consensus estimates of $12.6 billion, $19.9 billion, and $27.4 billion. He sees Micron benefiting from “strong tailwinds” across both DRAM and NAND, with F27E revenue and EPS growing 66% and 80% year-over-year. He also projects HBM to grow at a 40% CAGR (compound annual growth rate), surpassing $100 billion by 2028E, supported by sustained AI demand, which he expects to remain strong at least through 2027E. In addition, he highlights “near-term tailwinds” in traditional DRAM and NAND nodes, as AI increases content intensity in consumer end markets while also exerting upward pressure on pricing, supporting robust near-term profitability.

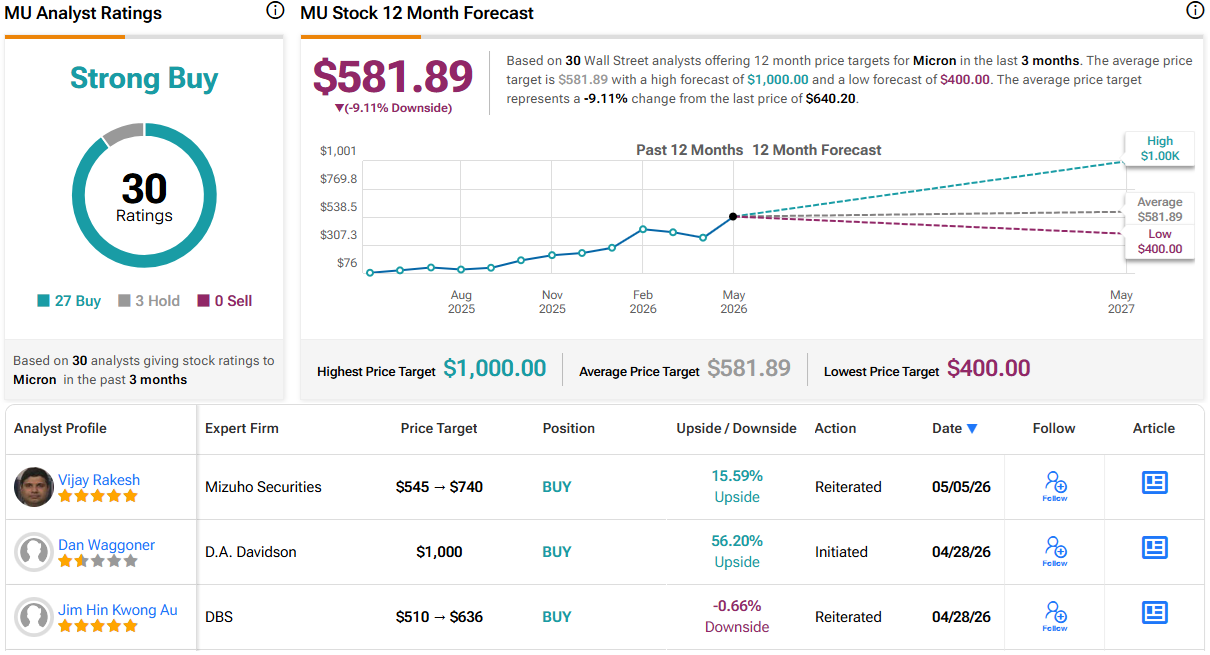

Bottom line, with agentic AI driving memory demand higher, Rakesh has raised his MU price target from $545 to $740, implying the stock will gain another 15.5% over the coming months. Hardly needs adding, but the 5-star analyst maintained an Outperform (i.e., Buy) rating on the shares.

Micron stock gets a Strong Buy consensus rating on Wall Street, based on a mix of 27 Buys vs. 3 Holds. That said, the gains have taken the share price beyond the $581.89 average target. With this in mind, watch out for either additional price target hikes or rating downgrades shorty. (See Micron stock forecast)

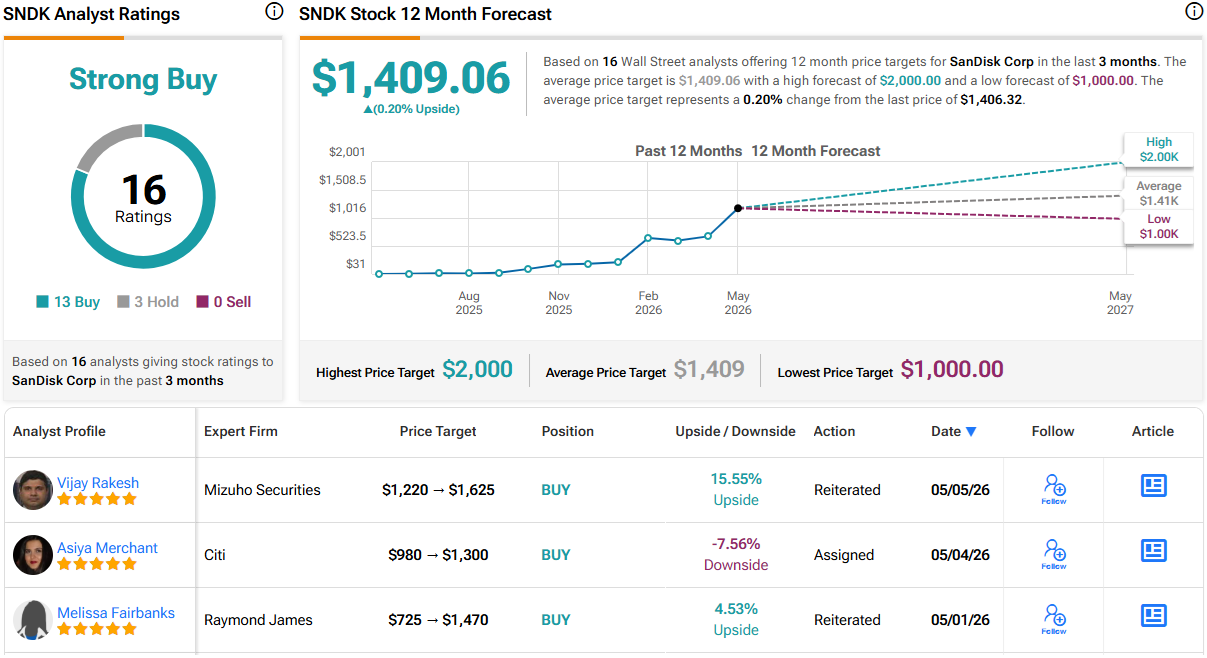

As for SanDisk, with agentic AI and inference driving growing NAND demand, Rakesh has reiterated an Outperform (Buy) rating on the shares and raised his price target from $1,220 to $1,625, suggesting the stock will also add another 15.5% in the year ahead. (To watch Rakesh’s track record, click here)

The new target implies roughly 9x F27E EPS compared with the prior ~8x multiple. Rakesh says this remains conservative compared to the SOX trading at ~20x P/E (C27E), given pricing tailwinds expected to persist through 2027E, supporting gross margins above 70% and EPS growth of ~51x from F25 to F28E. “We note SNDK and other players are benefiting from demand outpacing supply in the NAND market, driving higher pricing, as AI continues to drive tailwinds across handset, PC and server (eSSD) end markets with Reasoning/ Answer Tokens driving 2M+ Context windows and LLM/MMM data generation, while Agentic AI continues to ramp,” the analyst explained.

12 other analysts join Rakesh in the SNDK bull camp, while 3 Holds can’t detract from a Strong Buy consensus view. However, the $1,409.06 average price target implies shares will stay rangebound for the time being. As with Micron above, keep an eye out for additional analyst revisions. (See SNDK stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.