One thing is certain these days, and that’s uncertainty. Markets remain volatile, as a series of data releases have investors somewhat unsure whether high inflation, rising interest rates, or a possible recession – or perhaps all three at once – will come to dominate the forecasts. The result: day-to-day price swings and sharp changes that make predictions a risky business.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Not every economist, however, is willing to throw in the towel, and the difficult market environment hasn’t put the scare on John Stoltzfus. The chief investment strategist from Oppenheimer remains bullish on stocks, and in his monthly report on market strategy, he lays out why.

“Our longer-term outlook for the US economy and the stock market remains decidedly bullish. We believe US economic fundamentals remain on solid footing. Once inflation begins to moderate, US growth should begin to recover, supported by consumer demand and business investment,” Stoltzfus opined.

Acknowledging the current volatility, and the high risk of a dangerous economic recession, Stoltzfus goes on to say, “We can’t say that the market has bottomed at these levels or that the bear market might not grind on for some time to come, but with so much bad news already priced in, the potential rewards of investing at these levels are looking more attractive relative to the risks.”

Taking Stoltzfus’ outlook into consideration, we wanted to take a closer look at three stocks earning a round of applause from Oppenheimer, with the firm’s 5-star analysts forecasting over 30% upside potential for each. Using TipRanks’ database, we learned that the rest of the Street is in agreement, as all three boast a “Strong Buy” analyst consensus.

CSG Systems International (CSGS)

The first Oppenheimer pick is CSG Systems International, a software and services company in the business support systems (BSS) niche. CSG’s platforms, available on the SaaS model, offer a wide range of functions, including revenue management and monetization, wholesale and partner management, and payment and merchant services. The company has a worldwide reach, and works with well-known brands as Bell, Comcast, and Dish.

CSG has brought steady performance over the past several years, with the recent 3Q22 results being considered fairly typical. At the top line, total revenue was reported at 273.3 million, up 3.8% year-over-year. At the bottom line, the company’s results were split; GAAP EPS was down 20% y/y, from 50 cents to 40 cents, while non-GAAP EPS was up 20.5%, from 88 cents to $1.06.

On the balance sheet, CSG’s cash flows were down y/y. Cash from operations declined from $46.1 million to $22.8 million, while free cash flow fell from $38.7 million to $10.9 million. The company attributed the decline to ‘unfavorable changes in working capital.’

Even though the cash flows were down CSGS maintained its regular share dividend payment, as part of a $91 million year-to-date capital return to shareholders. The Q3 dividend was set at 26.5 cents per common share, and totaled $8 million paid out in the quarter. Annualized, the dividend is $1.06 and yields 1.9%, about average for the broader markets. The company has been gradually raising the dividend payment over the past 9 years.

In his coverage of CSG Systems for Oppenheimer, 5-star analyst Timothy Horan gives several reasons to believe that this company will bring long-term gains for investors. Horan writes, “The company has historically been a consistent cash cow serving MSOs (née ‘Cable Services Group’), but the base business is accelerating from: 1) digital, 5G, and cloud, 2) CSG’s taking share from less focused competitors, and 3) new management’s reorienting its modular SaaS-and cloud-native customer engagement offerings to faster-growing geographies and verticals outside the communications service providers (CSPs). The process will take time, but should boost growth and valuation.”

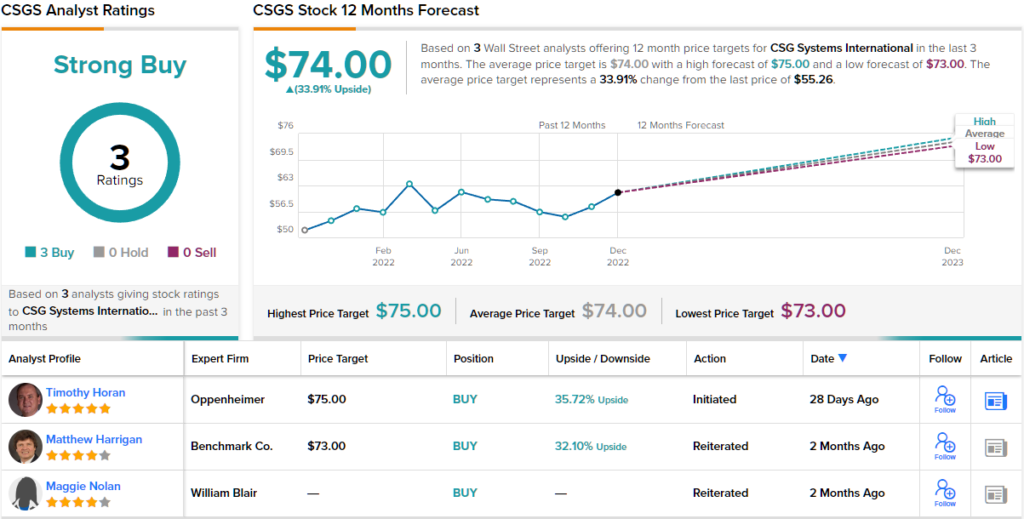

Horan translates his upbeat view of CSG’s forward prospects into numbers with a $75 price target – which implies an upside of ~36%. It’s not surprising, then, why he rates the stock an Outperform (i.e. Buy). (To watch Horan’s track record, click here)

Overall, there are 3 recent analyst reviews on record for CSGS, and they all agree that it’s a stock to buy – making the Strong Buy analyst consensus unanimous. The stock has an average price target of $74, implying ~34% one-year upside from the current trading price of $55.26. (See CSGS stock forecast on TipRanks)

Wag! Group Co. (PET)

The next stock we’ll look at is Wag! Group, an up-and-coming online app offering users access to a full range of pet care services, including dog walking, pet sitting, advice, and even pet training. The company boasts an online community of more than 400,000 pet caregivers, and has completed transactions for more than 12 million pet care services since its 2015 founding.

This stock is a new one on the public markets, having entered the NASDAQ exchange earlier this year through a business combination merger – a SPAC transaction. The merger was with CHW Corporation, and was approved on July 28. The PET ticker started trading on August 10. At its closing, the transaction net Wag! Group approximately $350 million in gross capital.

Last month, Wag! released financial results for 3Q22, showing top line revenue of $15.4 million, for a 161% year-over-year gain. The company’s revenue gain was driven by a strong increase in gross bookings over the period, from $13.7 million one year ago to $25.3 million in recent report – or y/y growth of 85%.

At the same time, during this period, the company’s net income fell sharply, from $1.6 million in 3Q21 to a 3Q22 net loss of $40.9 million. Wag! attributed that shift to one-time inclusion of COVID-era PPP loan forgiveness. Excluding that factor, the company saw a $1.4 million loss in the 3Q22.

During 3Q22, Wag! reported important gains on customer metrics. The company reached a total of 473,000 platform participants during the quarter, up 22% y/y and increased its Pet Parent Wag! Premium program penetration to 53%, beating the company goal of 50%.

Oppenheimer’s Jason Helfstein, a top analyst with a 5-star rating from TipRanks, sees plenty of reasons for investors to buy up shares of this newly public stock. Getting into some specifics, and his outlook for the company’s longer-term prospects, Helfstein writes: “We believe the company is well positioned to grow as pet services shift online… We believe the total addressable market (TAM) for online pet care will be a $24B opportunity by 2028, driven by the secular shift of consumers purchasing services/products via online platforms. We estimate the US Online Pet Care industry grew 98% y/y in 2021, as ~20M families adopted a pet during the pandemic lockdown.”

“Our 2026 service estimate would imply 190K households using the platform 2.0x weekly. This is 3% of our estimated 7.4M households that might shift to online dog-walking and pet service bookings. Currently modeling positive EBITDA profitability in FY24 and no need for additional funding,” Helfstein added.

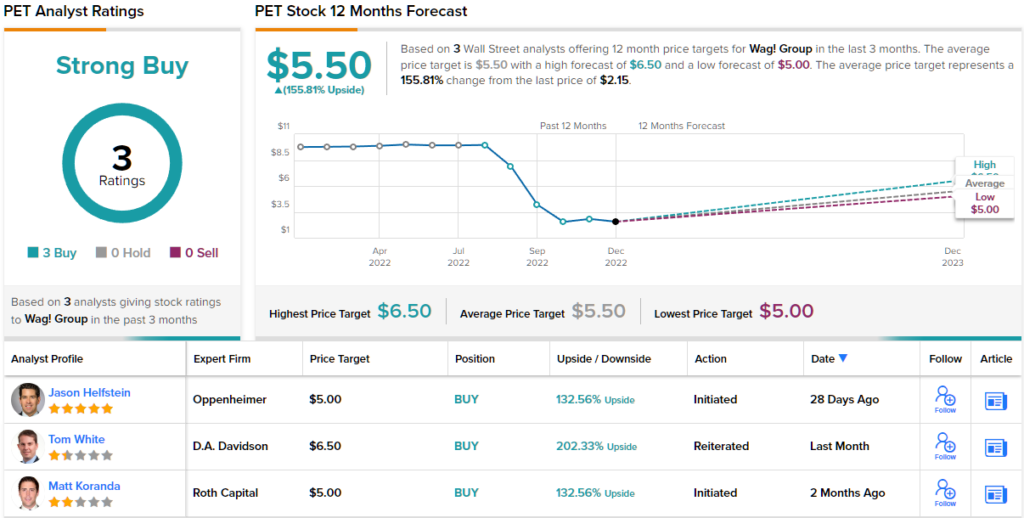

Keeping up his optimistic view, Helfstein rates PET an Outperform (i.e. Buy), and his $5 price target implies a one-year upside potential of a strong 132%. (To watch Helfstein’s track record, click here)

Overall, all three of the recent analyst reviews on PET are positive, making the consensus rating here a unanimous Strong Buy. The stock is selling for $2.15, and its $5.50 average price target suggests a bullish 156% upside potential by the end of 2023. (See PET stock forecast on TipRanks)

Datadog, Inc. (DDOG)

Last up is Datadog, a cloud software firm offering observability tools, the tools needed to monitor, track, and secure cloud-based websites in real time. Datadog’s package of cloud-based software tools includes automation, source control, bug tracking, troubleshooting, optimization, and basic monitoring instrumentation. Customers can use Datadog’s software and service to search and navigate site logs, follow key metrics and website traces, and make proactive management choices based on high-quality datasets.

The company offers investor a history of consistent EPS beats. Datadog’s last reported quarter, 3Q22, showed a bottom line of 23 cents per diluted share, compared to the 16-cent forecast, for a 43% beat. Revenue in the same quarter was up 61% y/y, reaching $436.5 million.

The top and bottom lines were not the only positive metrics. Datadog also saw $83.6 million in total cash from operations, which included $67.1 million in free cash flow. As of the end of Q3, September 30, Datadog had $1.8 billion in cash and liquid assets available.

Looking ahead, there is reason for continued optimism. Datadog’s ‘high-yield’ customers, defined as customers with at least $100K in annual recurring revenue (ARR), reached 2,600 at the end of Q3, up from 1,800 one year earlier, for a 44% y/y increase.

All of this shows that Datadog has a solid foundation to move forward, and Ittai Kidron, another of Oppenheimer’s 5-star analysts, would agree. The analyst says of Datadog, “The company has a strong history of outperforming expectations, never missing consensus expectations, and typically guiding above the Street… While not recession-proof, the mission-critical nature of its solutions gives Datadog relative resiliency in times of spending constraints. The company has also expanded into security, capitalizing on ‘shift-left’ efforts in security and its strong standing with developers, offering large TAM expansion and a long tail of growth.”

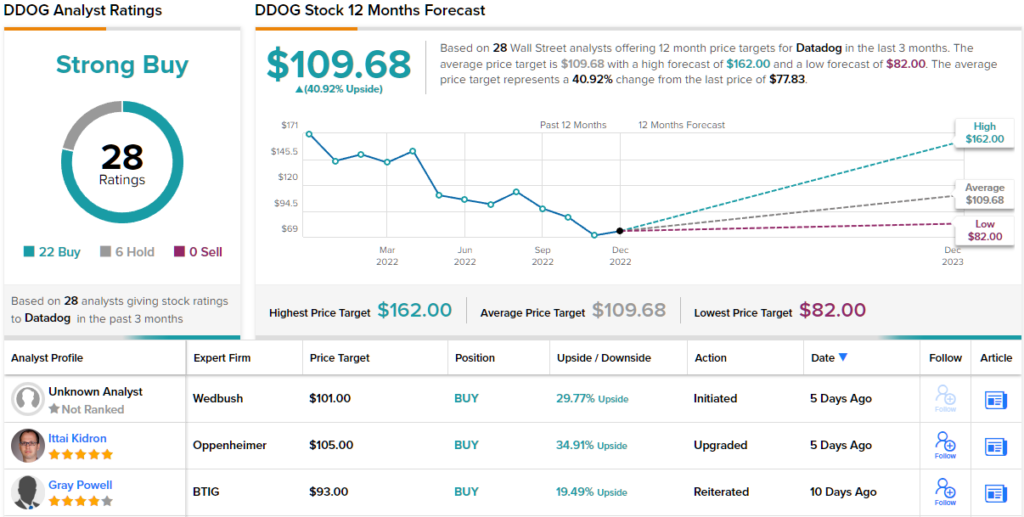

At the bottom line, Kidron describes this company as ‘a core long-term holding.’ Befitting this upbeat view of Datadog’s overall excellence as an investment, Kidron rates DDOG an Outperform (i.e. Buy), with a $105 price target suggesting ~35% one-year gain in the offing. (To watch Kidron’s track record, click here)

With 28 recent analyst reviews on file, including 22 Buys against 6 Holds, Datadog shares get a Strong Buy consensus from the Street’s pros. The stock is selling for $77.83 and its average price target of $109.68 implies ~41% upside over the next 12 months. (See DDOG stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.