Last summer, Elon Musk went on record describing lithium as ‘the new oil,’ pointing out that the light metallic element now forms a vital link in the automotive industry and supply chain. Lithium is an essential component of modern rechargeable battery technology and is found in everything from smartphones and tablets to laptop computers to electric-powered bicycles and automobiles.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Most of the world’s lithium is mined in Australia, Chile, and China. China is also the dominant player in the production of lithium-ion batteries, with a market share of approximately 80%. These are the facts behind Musk’s more recent comments on the subject, who points out the need for more of the element. “As we look ahead a few years, a fundamental choke point in the advancement of electric vehicles is the availability of battery-grade lithium,” he said.

Musk is not just talking about the issue; Tesla has also gone all-in on a new lithium refinery in Texas, a project that is estimated to cost $375 million and targeted to come online in 2025. The refinery will make Tesla the largest lithium refiner in North America.

You don’t have to be the richest man in the world, however, to take part in the coming lithium boom. As the metal faces more and more demand, lithium producers everywhere should benefit – and Wall Street’s analysts are pointing out stocks for investors to consider.

Against this backdrop, we’ve used the TipRanks database to locate two Buy-rated stocks that are heavily involved in the production of lithium-ion batteries, and are well-positioned to benefit from a continued boom in lithium demand. Let’s take a closer look.

Amprius Technologies (AMPX)

We’ll start with Amprius Technologies, a company that went public last year through a SPAC transaction. Amprius realized $87 million, and the ticker started trading on September 15. The company is putting its capital to work developing and producing high-end technology in lithium-ion batteries. Specifically, the company is focused on making and marketing silicon anode batteries, a lithium-ion battery technology with a higher energy density than traditional graphite anode batteries.

Amprius is developing its new batteries at a variety of sizes, to work in a wide range of applications, including electric vehicles, aviation tech, and wearable electronics. The company has begun construction of a new industrial-scale production facility in Brighton, Colorado, with a projected opening in 2025. The facility will total 775,000 square feet, and will have capacity to build up to 500 megawatt-hours at the opening. Full capacity is planned for 5 gigawatt-hours. Amprius’ factory will be the largest battery production floor in Colorado.

While Amprius is still in the ‘gearing up’ stages, it has shipped out more than 10,000 batteries to a select number of customers. The company’s products are listed under 10 sku numbers, and Amprius has more than 80 patents on file to protect its intellectual property.

Covering this stock for Northland Capital, analyst Abhishek Sinha sees some healthy growth ahead. He writes, “We believe AMPX is about to reach an inflection point with solid revenue growth in 2024 and breakeven gross margin in 2025. We see a clear path to profitability for this high growth company that has very differentiated and proven technology. We expect AMPX to achieve an EBITDA breakeven in late 2026.”

“We expect AMPX’s products revenue to grow 6-7x by the end of next year and much higher after that as the CO factory ramps up. AMPX has 80% repeat customers, which is a good indication of the sustainability of the demand,” Sinha went on to add.

Looking forward, Sinha quantifies this stance with an Outperform (i.e. Buy) rating on AMPX shares, and a target price of $16 that suggests a 91% upside on the one-year time frame. (To watch Sinha’s track record, click here)

Overall, all four of the recent analyst reviews on this stock are positive, showing that the Street is bullish – and giving AMPX a Strong Buy consensus rating. The shares are selling for $8.39, and their $14.50 average price target implies a gain of ~73% in the next 12 months. (See AMPX stock forecast)

Albemarle Corporation (ALB)

We’ll now shift gears and turn our attention to Albemarle, a North Carolina-based firm with a focus on specialty chemical products primarily based on lithium and bromine. The company refines both elements, and is particularly known for producing battery-grade lithium. Albemarle is a major supplier of lithium to the EV battery segment, and has a global reach, sourcing its lithium from mines in Australia, Chile, and Nevada.

Albemarle has recently restructured its MARBL Lithium Joint Venture, an Australian project, bringing MinRes onboard to improve the value given to customers. MinRes will also take on a 50% stake in Albemarle’s Chinese lithium plants. Rising prices for lithium in the global markets have been a boon for Albemarle, which has seen its earnings go steadily up in the past several quarters.

In Albemarle’s most recent quarterly results, for 1Q23, non-GAAP EPS reached $10.32, beating the forecast by $3.26 and expanding by a whopping 333% from the prior year. On the top-line, the company generated $2.6 billion in net sales, coming in $158 million less than expected despite 128% year-over-year growth. The company’s guidance for the rest of 2023 calls for revenue in the range between $9.8 billion to $11.5 billion, at the midpoint, a little under the $10.9 billion consensus figure.

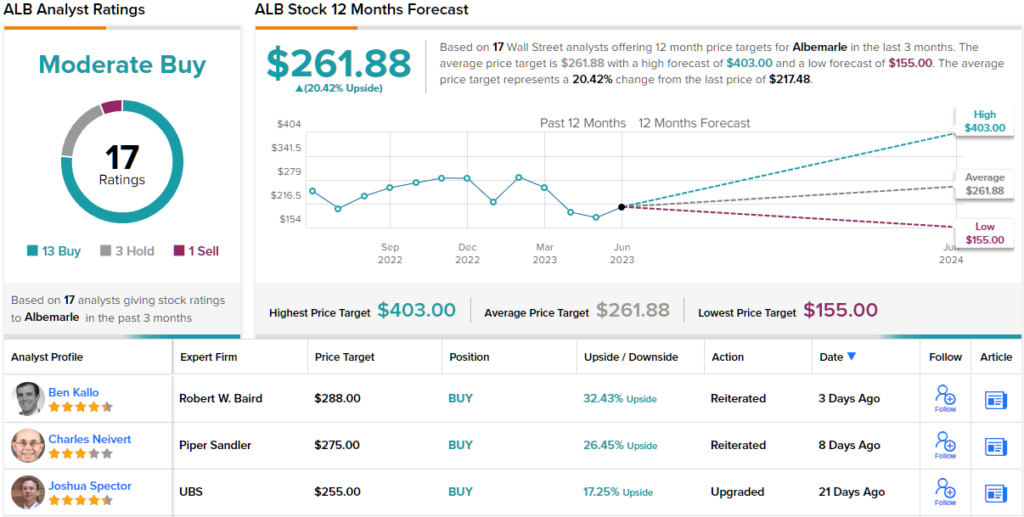

In the eyes of Baird’s 5-star analyst Ben Kallo, this is a company with real potential for investors. Kallo writes of Albemarle: “We believe that clarity on the impact of pricing, a reset of guidance, and ALB’s vertically integrated system position it as a leader for the near and longer term. ALB’s diversity and quality of resources give it a competitive advantage on cost and ability to service several end markets. We see upside to estimates from any increase in lithium pricing, potential tailwinds from the IRA, and the growing demand for lithium.”

The analyst goes on to give ALB shares an Outperform (i.e. Buy) rating and a price target of $288, implying a one-year upside of 32%. (To watch Kallo’s track record, click here)

Overall, Albemarle has picked up 17 analyst reviews recently, with a breakdown of 13 Buys, 3 Holds, and 1 Sell, giving the stock a Moderate Buy consensus rating. Albemarle shares are trading for $217.48 and their current average price target of $261.88 suggests ~20% upside potential in the year ahead. (See ALB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.