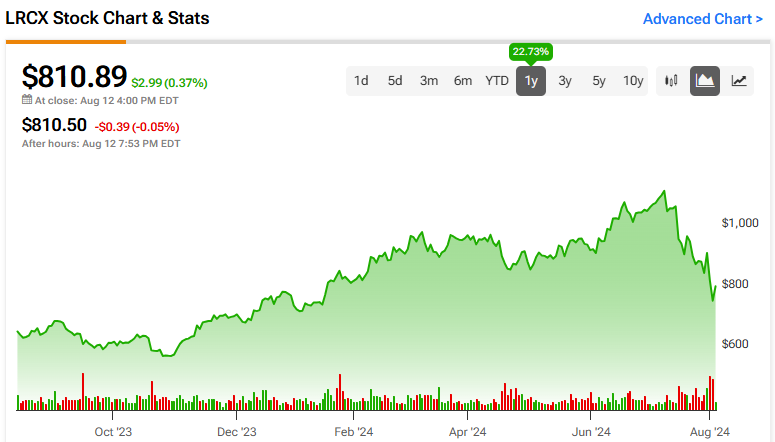

Shares of many highly-valued, high-multiple Tech stocks have fallen sharply during the recent market sell-off. While a reset was perhaps needed, as many of these stocks had reached unsustainable valuations, some great stocks were also thrown out with the bathwater, including semiconductor manufacturing equipment maker Lam Research (LRCX), as you can see below.

Claim 30% Off TipRanks

Trade LRCX with leverage

I’m bullish on this high-quality company based on its crucial role in the semiconductor supply chain, the wide moat of its high-tech business, projected earnings growth, and suddenly compelling valuation after the sell-off. Additionally, the analyst community sees significant upside potential of 36% for the company’s shares over the next 12 months.

Bargain Valuation for a Wide Moat, High-Quality Stock

With much of the air coming out of the AI trade during the current rotation, LRCX is now down nearly 30% from its 52-week high set just a few weeks ago in July. The good news for new investors looking at the stock now is that it trades at a very reasonable valuation.

Lam’s Fiscal Year just ended in June, and it earned $29.13 per share for the year. It is now beginning Fiscal 2025. With a share price of $811, the stock trades at 22.6 times consensus 2025 earnings estimates of $35.89 per share. This is roughly in line with the S&P 500 (SPX), which trades at a price-to-earnings ratio of 23.2 times and a forward multiple of 21.9 times.

But looking out to 2026, LRCX’s earnings are expected to grow to $46.02 per share, and the stock trades at just 17.6 times these estimates.

I would consider this to be a very attractive valuation for an important company that is growing earnings in a meaningful way like this. LRCX plays a critical role in the semiconductor industry, which is widely expected to grow significantly over the long term.

The company is one of the world’s largest manufacturers of semiconductor wafer fabrication equipment. Its equipment is used in the deposition and etching of semiconductors. Further, it has the largest market share in etch and the second-largest market share in deposition and serves both logic and memory chipmakers. Its customers include some of the world’s largest makers of semiconductors like Taiwan Semiconductor (TSM), Samsung (SSNLF), Intel (INTC) and others.

Demand for semiconductors, driven in large part by AI, is not expected to slow down anytime soon. Management consulting firm McKinsey expects it to grow to a $1 trillion market by the end of this decade. LRCX looks well-positioned to capitalize on this demand by providing its highly advanced equipment to these semiconductor manufacturers.

This is highly complex equipment and only a few companies have the technical expertise to provide it, giving Lam a real moat around its business.

The company spends about $2 billion per year on research and development. The technical expertise and considerable investment required to stay at the leading edge of this industry give it a competitive advantage and make it difficult for newer competitors to gain a foothold against it.

The quality of its business and the width of its moat are indicated by its impressive 47.6% gross profit margin, showing that the company also has real pricing power.

Becoming a Dividend Growth Stock

In addition to this relatively inexpensive valuation, Lam is also a dividend stock. Its yield of 1.0% may not be particularly compelling, but the company is becoming a dividend growth stock as it slowly but surely increases the size of this payout over time. Lam has paid dividends to its shareholders for the last nine years in a row, and it has grown this payout in each of those nine years. It has grown the dividend at a very respectable 12.7% compound annual growth rate (CAGR) over the past five years.

What’s more, the dividend payout looks extremely safe, with a conservative payout ratio of just 26.4%.

Is LRCX Stock a Buy, According to Analysts?

Turning to Wall Street, LRCX earns a Hold consensus rating based on 13 Buys, seven Holds, and zero Sell ratings assigned in the past three months. The average LRCX stock price target of $1,100.88 implies nearly 36% upside potential from current levels.

The Takeaway: A Strong Pick

While the tech sector sell-off has been painful for investors, it has also created the opportunity to buy some great stocks like LRCX at attractive prices.

Wall Street analysts clearly see significant potential upside for share of LRCX. Even the lowest analyst price target of $900 implies material upside from current levels.

I’m bullish on the stock based on its projected earnings growth and attractive valuation, especially for a company that plays a vital role in the manufacturing process for an industry that should continue to see immense growth in the years to come.