Micron (NASDAQ:MU) has become one of the market’s biggest AI winners, with the stock gaining 707% over the past year, as the company has benefited from AI’s insatiable demand for high-bandwidth memory (HBM).

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

But even though some might look at such a climb and conclude the shares’ upside could now be capped, investor Sarfatti Investment Research (SIR) argues that the opposite is the case.

With the stock trading at 11x forward P/E (some estimates have it at even a single-digit forward P/E), SIR believes the shares are “deeply undervalued.” “This is unheard of for a company showing over 190% year-over-year revenue growth and a 57% net income margin in the latest earnings release,” the investor said.

SIR had previously highlighted how “structural demand” is increasingly overtaking the volatility inherent in the memory industry’s well-defined cycles. The thesis was based on a rerating due to the “demand driver shifting” from consumer memory products toward AI infrastructure. HBM stacks are qualified on a per-GPU-generation basis, with each new generation requiring greater memory density, while Nvidia’s annual GPU release cycle further dampens cyclicality within this segment.

But while the initial focus centered on surging demand for GPUs and HBM used in training foundational models, attention has now shifted toward the orchestration and inference layers, where CPUs play a more central role. With Nvidia’s Vera Rubin platform beginning high-volume production, MU is also positioned to be a key supplier for Vera CPUs.

Of course, in an industry known to be highly cyclical, the primary concern remains oversupply. Although HBM capacity for 2026 is already fully allocated, there is still the possibility that hyperscalers pull forward demand in the near term, potentially setting up an “inventory digestion” phase in late 2027 or 2028. However, SIR points out that the 3-to-1 wafer trade ratio, where HBM requires roughly three times the wafer capacity of standard DDR5, acts as a structural constraint on bit supply growth and establishes a pricing floor that was absent in prior cycles.

Bottom line, SIR views Micron as the “most undervalued opportunity” in AI right now. The investor thinks a significant rerating is likely as demand expands across both the upcoming CPU-driven cycle and continued GPU-related HBM demand. The market still prices Micron as if demand were cyclical, despite growing evidence that AI-driven demand is increasingly structural rather than transient. “The combination of an incredible margin profile, a fully committed 2026 HBM capacity, and growth driven by SOCAMM2 (a next-generation AI server memory module concept) and HBM4 creates a path to $1,500 and beyond, and so I reiterate my Strong Buy rating on MU,” Sarfatti Investment Research summed up. (To watch SIR’s track record, click here)

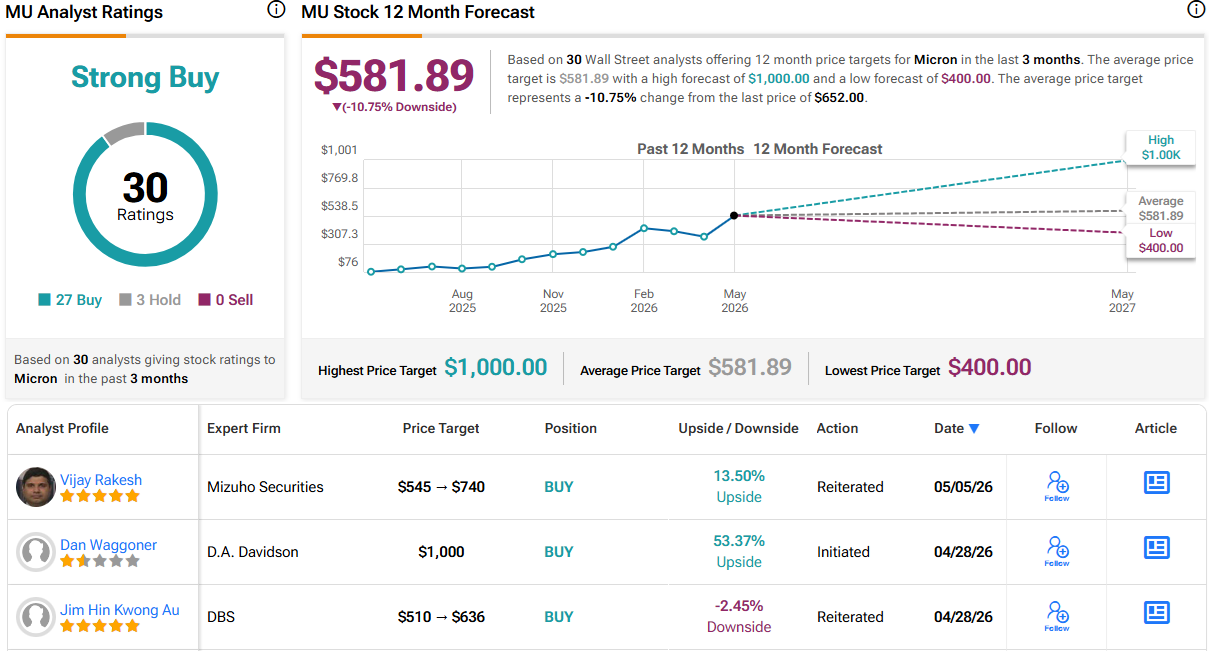

A Strong Buy is also the conclusion reached by the Street’s analyst consensus, a rating based on 27 Buys vs. 3 Holds. However, given the gains, the $581.89 average price target implies shares are now overvalued by 11%. It will be interesting to see if, as Sarfatti Investment Research argues, analysts rerate the stock in the near term. (See Micron stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.