The future of plant-based foods has yet to be decided, but for the company that serves as its poster child, its fate might already be sealed. Beyond Meat (NASDAQ:BYND) has seen its stock price plummet by 97% from its all-time high of $239.71 in July 2019 to just $7.16 at the time of writing. While I remain hopeful that the world will find a means of decreasing the impacts of meat production, transportation, and consumption, that optimism doesn’t extend to Beyond Meat’s battered shares, which look beyond repair.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The plant-based food industry as a whole still has tailwinds. According to Grand View Research, the U.S. plant-based food market is expected to experience a compound annual growth rate of 23.9% between 2023 and 2030, with revenue forecast to grow from $5.23 billion last year to $24.8 billion by the end of the decade.

However, the bulk of that revenue may end up in the pockets of long-tenured and well-established packaged foods companies like Conagra (NYSE:CAG), which owns Gardein plant-based products, WK Kellogg Co. (NYSE:KLG), which owns the MorningStar Farms brand and its plant-based products sold under the Incogmeato label, and Kraft Heinz (NASDAQ:KHC), which now offers a plant-based version of its widely popular Mac & Cheese.

For Beyond Meat, which doesn’t report Q4-2023 earnings until February 22, 2024, the writing may already be on the wall. Even for speculative investors looking for a buy-low opportunity, the company that once branded itself as the future of food should be avoided, in my opinion. I am bearish on the stock.

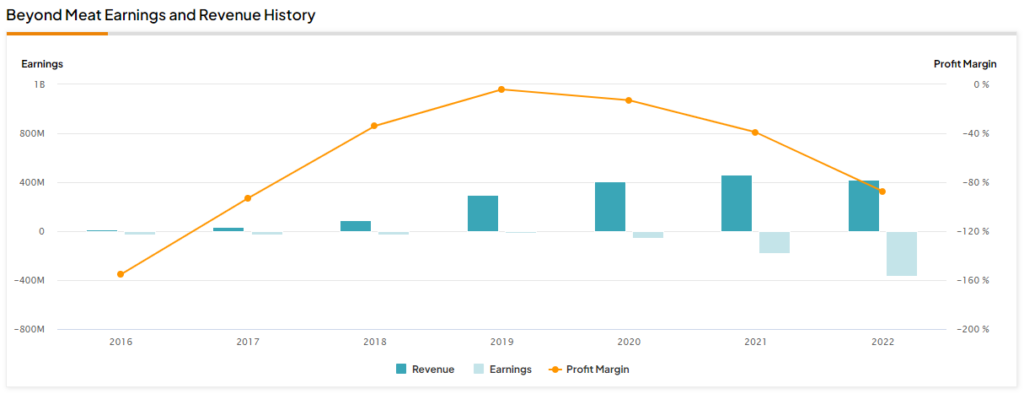

Rapid Rise, Rapid Fall

Despite being an early leader in the plant-based food products space, Beyond Meat has failed to keep its head above the water. In 2019, the company’s IPO was set at $25 per share based on an implied market valuation of $1.46 billion, and 9.625 million shares of common stock were offered.

The valuation mirrored the meteoric ascent the company experienced under its founder and CEO, Ethan Brown, who began the company 10 years prior in 2009. By April 2013, Beyond Meat products were being sold to Whole Foods. After going public, Beyond Meat’s shares quickly took off, jumping 163% in one day and resulting in the company’s market cap exploding to $3.8 billion.

Yet, despite the company reaching peak revenue of $464.7 million in 2021 on the back of its brand recognition and domestic and global distribution networks, Beyond Meat has never been profitable. Worse yet, its losses have been mounting, with a -12.97% profit margin in 2020, -39.18% in 2021, and a disastrous -87.4% in 2022.

The result: Beyond Meat’s current market cap of $463 million is about 88% lower than its valuation in May 2019 in the wake of its IPO.

Overwhelmingly Negative Investor Sentiment

For investors, sentiment has rapidly deteriorated. Fast forward to early January 2024, and the stock is experiencing heavy put volume. Options traders have established a 2.01 put/call ratio, meaning there is more than twice as much interest in BYND puts than calls — an indication of bearishness.

Compounding this negative sentiment is the fact that the stock’s short volume and short interest ratio are substantial. Currently, 24.4 million shares are being shorted, which represents more than 40% of the 60.86 million float.

This bearishness is also being echoed by professional traders and insiders alike. Last quarter, hedge funds decreased their BYND positions by 56,900 shares, and out of 108 insider trades over the past 12 months, a substantial 89 have been sells. Going back to December 13, 2022, the company’s own CFO, Kutua Lubi, sold $217,682 worth of BYND shares before the stock went on to lose another 48% in 2023.

Ongoing Earnings Letdowns

The basis of Beyond Meat’s 97% share deprecation since its all-time high in 2019 is the company’s track record of disappointing earnings, which was most recently punctuated in November 2023 when it announced net revenues of $75.3 million, good for a year-over-year decrease of 8.7%. Only twice in the past nine quarters has the company been able to beat revenue estimates.

BYND’s net loss in Q3 2023 was $70.5 million, or $1.09 per common share, and adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) came in at -$57.5 million, or a -76.3% margin.

Beyond Meat was able to improve its gross margin to -9.6%, which, despite representing the company’s costs of production exceeding its total sales, did mark an improvement over the -18% gross margin posted one year earlier.

It’s a similarly abysmal story for earnings per share (EPS). Dating back to Q4 2020, BYND has posted 12 consecutive quarters of EPS losses of at least 31 cents, reaching as low as a loss of $1.60 in Q3 2022. As a result, it’s hardly a surprise that the consensus EPS forecast for Q4 2023 is a loss of 89 cents.

All of this has contributed to a price-to-earnings (P/E) ratio of -1.9, a far cry from the ideal range of 20–25 and a negative figure which illustrates that the company is continuing to lose money.

Is BYND a Sell, According to Analysts?

BYND stock earns a Moderate Sell consensus based on zero Buys, five holds, and five sells. The average BYND stock price target of $5.83 implies 19.8% downside potential.

The Takeaway

Although the plant-based food industry will likely grow between 2023 and 2030, firmly established companies in the packaged goods space are better positioned to capitalize on the emerging trend than newcomers like Beyond Meat. BYND is forecast to continue its run of poor stock performance based on persistently negative earnings and ongoing revenue misses, making it an unattractive investment.