I am neutral on International Business Machines Corporation (IBM) as it has a strong competitive position, Wall Street analysts are generally bullish on it, and the average price target implies decent upside.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

However, the stock looks slightly over valued based on its historical valuation multiples and the company faces stiff competition from other large companies.

Founded in 1911, International Business Machines Corporation is a multinational technology company headquartered in Armonk, New York. The company has operations in over 171 countries.

IBM sells computer software, hardware, and middleware and provides consulting and computing services in different technological sectors. The company has also always been a strong believer in research. It has managed to have the highest number of registered patents over the last 28 years.

Strengths

The core strengths of IBM are its strategic imperatives. These are its security businesses, cloud, social, data analytics, and mobile.

Compared to last year, IBM’s revenue from these five sectors has climbed by 16% in Q4 2021. Over the years, revenue in these five sectors has seen a drastic increase, which is also why the company invests heavily in these sectors.

That said, IBM also expects the demand for hybrid installations to grow. A hybrid installation combines cloud-based and local services for a larger business that does not want to move data to the cloud.

Recent Results

In Q4 of 2021, IBM reported strong 6.5% year-over-year revenue growth (up 8.6% on a constant currency basis), driven in large part by 8% (10% constant currency) software revenue growth, 16% (18% constant currency) hybrid cloud growth, and 13% (16% constant currency) consulting revenue growth.

The company’s balance sheet also remained in great shape, with full-year free cash flow of $6.5 billion and $7.6 billion in cash on hand at year-end. The company also paid out a whopping $5.9 billion in dividends to shareholders in 2021, which was fully covered by free cash flow.

Valuation Metrics

IBM stock looks slightly overvalued here as it trades above its historical valuation multiple average on a price-to-normalized earnings basis and EV/EBITDA basis.

Its EV/EBITDA ratio is 9.3 compared to its historical average of 8.9 and its price-to-normalized earnings ratio is 12.1 times compared to its historical average of 11.1 times.

Moving forward, analysts expect EBITDA to increase by 10.9% and normalized earnings per share to increase by 26.5% over the next 12 months.

Wall Street’s Take

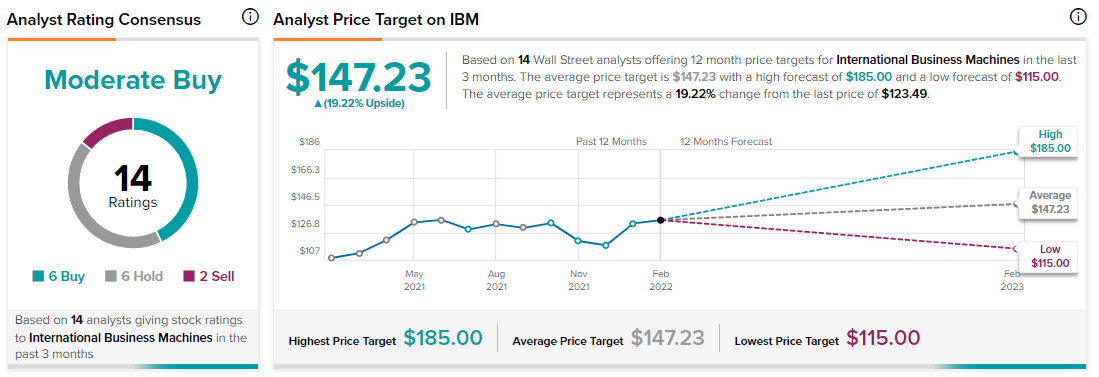

According to Wall Street analysts, IBM earns a Moderate Buy rating based on six Buy ratings, six Hold Ratings and two Sell ratings in the past three months. Additionally, the average IBM price target of $147.23 puts the upside potential at 19.2%.

Summary and Conclusions

IBM stock is backed by a large intellectual property portfolio as well as several growing business segments. It also benefits from an asset-light business model that throws off a lot of free cash flow and enables it to pay off a very attractive and consistently growing dividend.

Given that it finally seems to have turned the corner and returned to consistent top-line growth, IBM likely deserves a richer multiple than it has commanded in recent years.

On the other hand, it continues to face stiff competition from other large tech companies and does not look particularly cheap at the moment.

Download the TipRanks mobile app now

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Read full Disclaimer & Disclosure