What to make of the markets today? The week started with the S&P 500 officially falling into bear territory, and on Wednesday the Federal Reserve made its most aggressive rate hike in almost 30 years – 75 basis points, or 0.75% – indicating that inflation, which is running at 8.6% annualized, is now Economic Enemy #1, even at the risk of recession. It’s definitely not an environment to encourage investments.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

But there are stocks out there that are worth a second look, if investors know which signs to watch. One clear signal comes from corporate insiders, the company officers who have to steer their companies through these treacherous market currents. They’re responsible for more than just their own wallets; Boards and shareholders look to them to bring in profits and share appreciation, or to properly prepare their firms to whether turndowns. As a result, they don’t trade their own stocks lightly, and when they buy en masse, those buys should grab investors’ attention.

TipRanks has the tools needed to follow the insider trades. One popular data sorting tool, the Insiders’ Hot Stocks, offers multiple sorting options for investors seeking to find and follow stocks with solid insider buys. We’ve pulled up the latest details on two controversial stocks that are showing both recent steep losses and strong insider buying. We’ll add in commentary from the Wall Street analysts to get a better view of these positions.

Maximus, Inc. (MMS)

The first stock we’ll look at, Maximus, is at heart a personnel agency. The company provides management and administrative services to government agencies on a contract basis. Maximus’ business is centered in the US, but it also operates in the UK, Canada, and Australia. Maximus is a provider of admin services for a number of major programs in the US social welfare system, including Medicaid and Medicare.

Maximus has seen a sharp decline in share value in recent weeks, despite reporting generally sound financial results for its Q2 of fiscal year 2022. The quarter, which ended on March 31, saw top line revenue of $1.18 billion, up ~22% year-over-year. Diluted EPS, at 80 cents, was down from the $1.29 reported in the year-ago quarter – but did beat the 71-cent forecast by a 12% margin.

What worried investors, however, was the company’s guidance. Revenue guidance for the full fiscal year remained unchanged, at $4.5 billion to $4.7 billion, but the EPS guidance of $3.00 to $3.50 was considered somewhat weak. The midpoint of the EPS range, $3.25, was well below the expectation of $5.23.

On a positive note, MMS declared its Q2 dividend at 28 cents per common share. This annualizes to $1.12 and gives a yield of 1.8%, about equal to the market average. The key point on this dividend is its reliability – Maximus has been keeping up the payments, and slowly increasing them, for the past 13 years.

On the insider trading front, there have been three major recent purchases of MMS shares by corporate officers just this week. Company CEO Bruce Caswell spent just over $500K to buy up 8,300 shares, while Board Member John Haley bought 18,000 shares for $1.085 million. Another company Director, Raymond Ruddy, made a purchase of 17,341 shares, for just over $1 million. Stock watchers should note that Ruddy has a 60% success rate when trading his own company’s shares, and has realized a 10.5% return. (To watch Ruddy’s track record, click here)

Covering this governmental contractor stock for Raymond James, analyst Brian Gesuale is cautiously bullish going forward. He writes, “MMS reaction to the print seems to price in many… concerns, and any prospect of ‘recession’ gives the stock a defensive cloak creating some optimism that it could be a relative performer versus a basket or more macro sensitive stocks. Unfortunately, it looks like FY24 will be the first year that the consolidated business can grow materially from the COVID shadows. Market sentiment is also prone to shift should the mid-term elections slant to Republican favor.”

These comments come with an Outperform (i.e. Buy) rating from the analyst, although he does admit that his rating should be considered ‘soft.’ Gesuale puts a price target of $80 on the stock, suggesting ~34% one-year upside. (To watch Gesuale’s track record, click here)

Some stocks fly under the radar, and Maximus is one of those. Gesuale’s is the only recent analyst review of this company, which is selling for $59.89.(See Maximus stock forecast on TipRanks)

Avis Budget Group (CAR)

Let’s shift our focus now, from government work to car rental, where Avis Budget Group is one of the industry’s long-established names. The company owns the major global brands Avis, Budget and Zipcar, along with an array of smaller regional car rental brands in Europe, South American, and Australasia. Taking its brands together, Avis boasts over 11,000 rental offices in 180 countries, with a fleet of 600,000 vehicles. The company brought in $9.1 billion in global revenues last year.

Avis’ solid performance has continued, as shown by the 1Q22 results. At the top line, the revenue of $2.4 billion was up 77% year-over-year, while the adjusted EPS came in at $9.99 per diluted share, the second highest print of the past two years. The company also reported high vehicle utilization rates – 68.9% in the American market, 63.2% internationally – indicating both a strong business and plenty of reserve vehicles to meet demand or to rotate cars through repair and maintenance. The company had $900 million in liquid assets at the end of the quarter.

The company does not pay out a dividend, but its Board has authorized increases to the existing share repurchase program. The increases, of $1 billion in March and $2 billion in May, will allow Avis to aggressively support share prices; there is $2.3 billion available in the current authorization.

Investors should note that CRTO shares hit a peak value in April of this year, and since then have been falling ~50%. A tough market and choppy seasonality amplified by the uneven global recovery from the COVID crisis have all combined to make Wall Street a bit wary of this stock.

That did not stop Bernardo Hees, Executive Chairman of the Board, from gobbling up Avis shares recently. Since latter half of May, Hees has bought over 83,000 shares, spending a total of $14.79 million on the stock. He made the buys in three tranches, spending between $4.89 million and $4.95 million on each. Hees’ average return when purchasing Avis stock has been an impressive 53%.

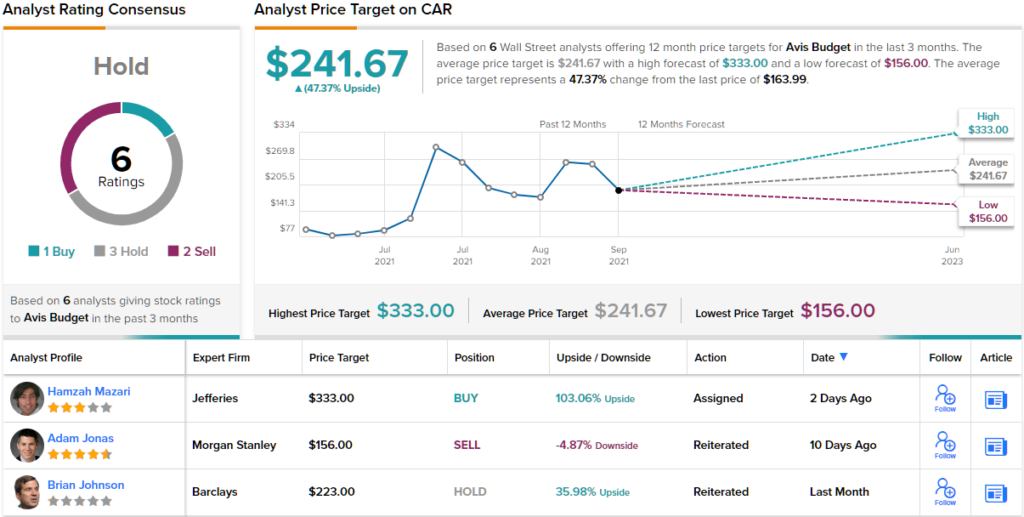

This rental car company also gets the nod from Jefferies analyst Hamzah Mazari who writes: “What to do with CAR shares: Buy more if you believe CAR can run at structurally higher margins and sustain high-single-digit growth longer term which will lead to structurally higher multiples going forward. We also think balance sheet catalysts continue to be underappreciated.”

Analyst comments on stocks don’t get much more upbeat than that, and Mazari backs it with a Buy rating and $333 price target that indicates potential for a robust 103% upside in the months to come. (To watch Mazari’s track record, click here)

Overall, the Street’s take offers an interesting paradox; CAR stock currently boasts a Hold consensus rating, based in 3 Holds, 2 Sells and a single Buy. However, there’s some nice gains projected here; at $241.67, the average target suggests shares will rise ~47% in the year ahead. (See CAR stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.