Honda (NYSE:HMC) is the world’s leading motorcycle manufacturer, with roughly 3x the 2023 unit sales of Hero and 4x that of Yamaha. It also sells ICE (internal combustion engine), hybrid, and fully-electric vehicles, known for their reliability and fuel efficiency. Hybrid vehicles seem to have turned a corner, with Honda’s earnings growing faster than Tesla’s (NASDAQ:TSLA) over the past year. I remain bullish on Honda because of its low valuation and exposure to emerging Asia, a region that could soon come roaring back.

Claim 30% Off TipRanks

New trading tool for TSLA bearsThe Opportunity in Emerging Asia

Honda is big in emerging Asia. From India to China to Thailand to Vietnam, consumers love Honda motorcycles, and they love Japanese manufacturing. And why shouldn’t they? In my experience, Honda makes some of the most reliable cars out there. The motorcycle segment is no different.

There are huge tailwinds as these Asian countries grow their GDP per capita. In Indonesia, the average Honda motorcycle retails for less than $2,000. As you can imagine, that price tag is likely to be much higher five years from now and in the distant future.

Honda’s unit sales in Asia make up a substantial share of its business, as you can see below:

Don’t Fret the Japanese Currency

Also, notice that Honda’s unit sales in Japan make up a small portion of its business, meaning weakness in the Japanese Yen doesn’t have much of an effect. Honda’s cash and cash equivalents are also diversified. In its last 20F, Honda said, “The ¥3,803.0 billion in cash and cash equivalents as of March 31, 2023 is mainly denominated in U.S. dollars and in Japanese yen, with the remainder denominated in other currencies.” The company has over $30 billion of cash and cash equivalents today.

Why I’m Bullish on a Rebound in China

It is well understood that Southeast Asia and India have tons of room to grow. However, there’s been a lot of negative things going on in China. Does the Chinese real estate crisis mean China and its neighboring countries are done for? I suspect the answer is no. Chinese savings rates are massive. It’s not that Chinese consumers have no money; they’re just not spending it. But I think they eventually will.

Gross domestic savings account for 47% of China’s GDP compared to just 17% for the United States. A rebound in consumption could be bullish for Honda’s automotive and motorcycle sales in China and neighboring countries like Vietnam.

The Valuation Is Still Favorable

I’ve been bullish on Honda since I first covered it in January of 2023. Since then, the stock has surged 38%, all while paying a nice dividend. I’ve since taken profits, but with the recent pullback, I think Honda stock is still cheap. In fact, I think I grossly understated Honda’s profitability potential in the past.

Honda averaged a 3.1% return on assets over the past 15 years (from 2010 to 2024). If we apply that to the company’s total assets today, we can conclude that Honda’s normalized earnings power is about $6.1 billion, giving it a normalized P/E ratio of just 8.4x based on its current market cap.

While Honda may be over-earning in a strong North American market, it may simultaneously be under-earning in Asia. Auto sales are cyclical, so if there’s a recession, Honda’s earnings could temporarily fall.

With auto companies, I’ve had the most success buying strong manufacturers below their tangible book value, which protects my downside. Honda currently trades at 0.65x its tangible book value. In comparison, Toyota (NYSE:TM), Stellantis (NYSE:STLA), and Ford (NYSE:F) all trade above 1x their tangible book value. Perhaps if Honda can engage in some cost-cutting efforts or continue its pace of share buybacks, its multiple will rerate higher. At this point, anything positive on the upside, such as a boom in emerging Asia, just adds excess returns.

Honda’s Hybrids May be the Future

I think hybrids have a strong value proposition. They are more versatile than pure EVs, which come with range anxiety and make long road trips difficult with lagging and slow charging infrastructure in many regions.

Using data from Edmunds, Aparna Narayanan of Investor’s Business Daily recently wrote the following: “The total market share of conventional hybrid cars and plug-in hybrids grew to 9.1% in 2023. The EV share rose to 6.9%. Meanwhile, traditional vehicles with internal combustion engines fell to 84%. She also said, “In 2023, hybrid and EV sales in the U.S. each crossed 1 million for the first time. Hybrid sales rose 65% vs. a 46% gain for EV sales.”

In other words, EVs and ICE vehicles are losing share to hybrids. This benefits Honda, which is a leader in the hybrid space. In fact, over the past year, Honda’s net income grew at a faster pace than Tesla’s.

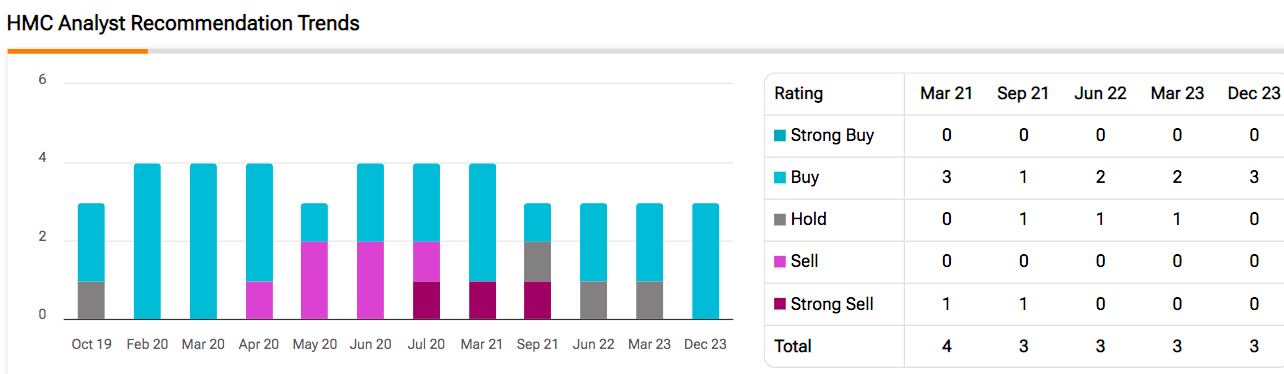

Is HMC Stock a Buy, According to Analysts?

Currently, all three analysts covering HMC give it a buy rating. In the below image from TipRanks, you can see how analyst recommendations have changed over the years. In HMC’s case, analysts have become notably more bullish over the past three years.

The Bottom Line on HMC Stock

Honda’s net income grew faster than Tesla’s over the past year on the back of hybrid vehicles gaining share against ICE and EVs. Honda may be slightly over-earning and cyclical, but its stock is still cheap on normalized earnings and a price-to-tangible book basis. Moreover, I expect that Honda’s performance won’t be too adversely affected by a weakening Japanese Yen and may benefit as China rebounds and emerging Asia booms.