If there’s one thing certain, it’s that markets are unpredictable – and that unpredictability is increasing. The reasons are multiplying: high inflation is rising higher, wages are not keeping up, Russia’s invasion of Ukraine has started Europe’s largest war since 1945, and energy and food commodities – key ingredients in the inflation mix – are sure to rise in price as a result of that fighting.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

It will be interesting to see, in the coming weeks, just how these cross currents impact the markets, and especially so as we approach the peak of the earnings season. Last year, despite high inflation, saw generally solid earnings numbers; the big question now is, will that continue?

The analysts at Goldman Sachs are working to give at least one answer to that question, by finding stocks that are primed to gain in the current environment. They’ve picked out three equities that offer the attractive combination of Buy-ratings and high upside potential – in the Goldman view, triple-digit potential. We ran the trio through TipRanks’ database to see what other Wall Street’s analysts have to say about them.

Arcutis Biotherapeutics (ARQT)

We’ll start with Arcutis, a clinical-stage biopharma company that is working in the dermatology niche, and its chief product, roflumilast (also called ARQ-151), is being evaluated in Phase 3 clinical trials. In its cream formulation, the drug is being tested as a treatment for atopic dermatitis; in foam formulations, it is undergoing trials for the treatment of seborrheic dermatitis and scalp and body psoriasis. In an important event for investors, the company reported in December that roflumilast cream’s NDA for the treatment of plaque psoriasis was accepted by the FDA, with a PDUFA date of July 29, 2022.

That acceptance opens the way for Arcutis to begin planning commercialization activities for roflumilast cream. In a move that will aid commercialization, the company announced that roflumilast cream has moisturizing properties similar to commercially-marketed, ceramide-containing moisturizing creams.

On the clinical side, Arcutis has several Phase 3 trials ongoing. In its most recent clinical update, the company announced that enrollment in the ARRECTOR trial, a Phase 3 pivotal study of roflumilast foam in the treatment of scalp and body psoriasis. This study has 432 subjects enrolled, and topline data is expected in late Q3 or early Q4 of this year. There is a projected patient base of 3 million people for this product.

The likely FDA approval and the high profit potential of roflumilast are the key factors behind Goldman Sachs analyst Chris Shibutani’s bullish stance on ARQT. He writes, “We expect FDA approval of the NDA by the July 29th PDUFA date and project potential peak sales in the initial psoriasis indication exceeding $1bn in 2036. Our confidence in the company’s ability to execute on the commercial launch derives in particular from what we see as a conservative pricing strategy aimed to improve payor dynamics…”

“We look for top line data readouts from three Phase 3 studies in mid- to late-2022 to further de-risk additional meaningful commercial opportunities, and in our view, expand the visibility of the company’s ripening portfolio and thus the company as an attractive strategic asset,” the analyst added.

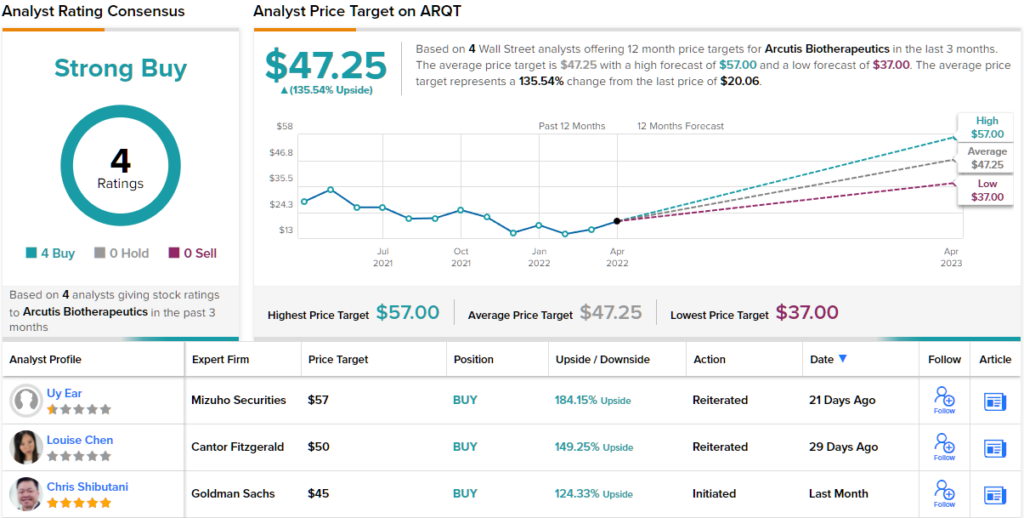

All of the above makes it clear why Shibutani is now standing with the bulls. The 5-star analyst rates ARQT a Buy while his $45 price target implies an upside of ~124% for the year ahead. (To watch Shibutani’s track record, click here)

Are other analysts in agreement? They are. Only Buy ratings, 4, in fact, have been issued in the last three months, so the consensus rating is a Strong Buy. ARQT is trading for $20.06 and its $47.25 average price target implies an upside of ~136% in the year ahead. (See ARQT stock forecast on TipRanks)

Tricida, Inc. (TCDA)

Next up is Verrica Pharma, a company focused on the development and commercialization of drug candidate veverimer. Previously known as TRC101, this drug is an orally administered polymer, not absorbed by the human system, that is designed to treat metabolic acidosis – too much acid in the body tissues – by absorbing excess acids. The drug candidate is being studied for its applications to the treatment of metabolic acidosis associated with chronic kidney disease (CKD).

Tricida is currently conducting the VALOR-CKD trial. This Phase 3 clinical study follows several previous trials of veverimer, which showed positive data on safety, tolerability, and efficacy. The VALOR trial, underway now, will evaluate the safety and efficacy of the drug in delaying CKD progression in patients also suffering from related metabolic acidosis.

For administrative reasons, the company will be shortening the VALOR trial early. The trial currently has 1,480 subjects enrolled and randomized, and evaluation will continue to the primary endpoint in 3Q22. The company expects to release top line data in 4Q22.

On the business side, Tricida had $150.6 million in cash assets on hand at the end of 2021. With Q4 admin and R&D expenses of totaling $45.9 million, this gives a cash runway of nine months. The company has attributed its early end to the VALOR trial to its cash status, stating a need to keep funds available for post-trial operations.

Even though the company has admitted that cash is tight, Goldman Sachs takes a sanguine view of this stock. The company’s 5-star analyst Madhu Kumar writes: “We are optimistic on the outlook for veverimer in MA with CKD considering the safety and efficacy in three previous placebo-controlled clinical studies. Specifically, the data show patients experience only mild adverse events (AEs) and achieve improvements in serum bicarbonate (SBC) levels, a key marker for MA with CKD severity, in addition to other key functional outcomes. Given these encouraging results, we look forward to VALOR-CKD results in 4Q22 as the key event for TCDA shares.”

These comments support Kumar’s Buy rating on the stock, while his $25 price target implies a one-year upside of 126%. (To watch Kumar’s track record, click here)

Overall, there are only 2 recent analyst reviews of TCDA but they both agree that this is a stock to buy, giving the company its Moderate Buy consensus rating. The stock is selling for $11 and its $21.50 average target indicate potential for 94% upside in the months ahead. (See TCDA stock forecast on TipRanks)

Coupang (CPNG)

Now let’s shift gears, to e-commerce, where Coupang is a market leader in South Korea’s online retail sector. The company offers an online platform where customers can buy, well, anything. From pet supplies to kitchen wares to home furnishings to automotive needs to childcare items, it’s all under one electronic roof. In a plus for customers, Coupang also offers a guaranteed fast delivery on more than 5 million items, using its Rocket Delivery network.

All of this adds up to big revenue numbers. In the pre-COVID year of 2019, Coupang saw US$5.9 billion in total sales, and during the pandemic crisis year of 2020, with lockdowns keeping everyone home for extended periods – and putting a premium on online retail – Coupang saw revenues double to US$12 billion.

In 2021, as economies reopened and people got back to work, they had more money to spend – and didn’t lose their habit of spending online. Coupang’s revenues grew to US$18.4 billion for the year. Last year was also Coupang’s first year as a publicly traded company on Wall Street. It’s quarterly reports for the year showed consistent sequential gains, as well as the broader year-over-year full-year gain.

Despite the growing revenues, Coupang still runs quarterly losses – although those losses did moderate in 2021. In the first quarter of last year, the company reported a 68 cent EPS loss; by the end of the year, this down to 23 cents. Looking ahead, however, the Street is predicting a 29 cent per-share loss in 1Q22.

Among the bulls is Goldman Sachs analyst Eric Cha who takes a bullish stance on CPNG shares. He writes, “The market is underestimating Coupang’s operating leverage potential, which we think has been concealed under COVID induced expenses… We especially believe larger improvement in adjusted EBITDA vs. consensus which could surprise the market and improve the overall sentiment on the stock due to improved LT profitability outlook as well as lessen concerns on the burn-rate and cash supply for the company.”

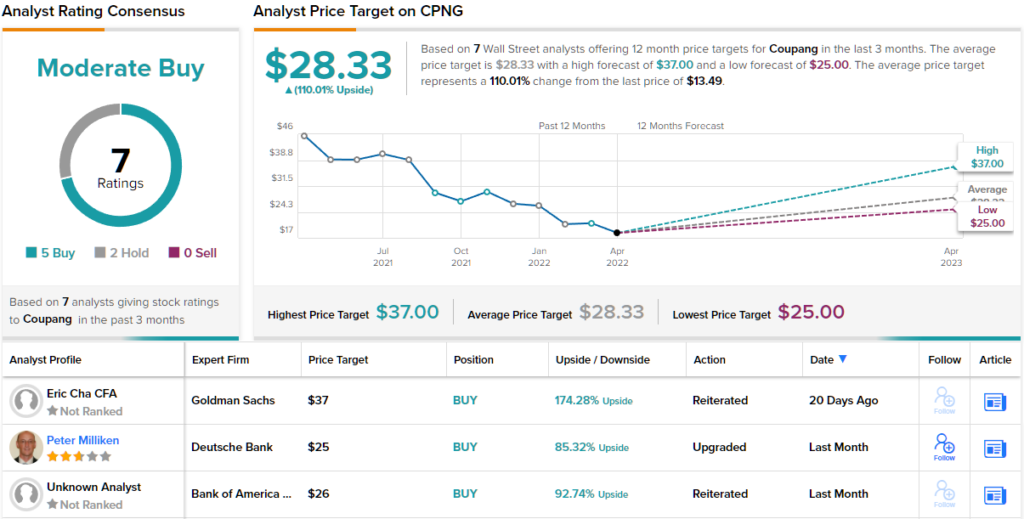

To this end, Cha gives CPNG a Buy rating along with a $37 price target. This figure indicates his belief in a 159% upside by year’s end.

Looking at the consensus breakdown, 5 Buys and 2 Holds have been published in the last three months. Therefore, CPNG gets a Moderate Buy consensus rating. Based on the $28.33 average price target, shares could rise 110% in the next twelve months. (See CPNG stock forecast on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.