Fortinet (NASDAQ:FTNT), a global security leader, lost more than 12% of its value on November 3 after reporting third-quarter earnings that failed to impress investors and analysts. However, the big picture remains bright for Fortinet, with the company well-positioned to benefit from the long-lasting tailwinds in the global cybersecurity sector.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The ongoing deceleration in billings growth paints an ominous picture of the short-term financial performance of the company, but Fortinet still has a long runway to grow in the long term. On the back of the recent sell-off, Fortinet stock has meaningfully detached from its all-time highs, making the company an attractive investment once again. I am bullish on FTNT for the long term.

Short-Term Challenges

Most of Fortinet’s short-term challenges stem from an aggressive reduction in corporate IT spending budgets amid rising interest rates and a shaky economy. Spending on firewalls, according to management, has seen a notable decline this year, which has hampered the financial performance of the company.

In the third quarter, billings grew by 5.7% year-over-year to $1.49 billion, approximately $100 million below management’s guidance. To add context, billings grew by 18% and 30% in the second and first quarters of this year, respectively. A year ago, billings grew by more than 32% in the third quarter, which highlights the ongoing deceleration of billings growth.

Management, during the third-quarter earnings call, highlighted disappointing demand for firewall products as the main culprit of this growth deceleration.

Management also highlighted marketing inefficiencies and the challenging environment for sales execution as reasons for the slowdown in growth. The cybersecurity sector can be surprisingly cyclical as corporate IT spending patterns closely follow the economy, and today, amid challenging macroeconomic conditions, Fortinet has found it difficult to make the most of its marketing investments.

The Promising Long-Term Outlook

At a time when macroeconomic conditions are challenging, Fortinet is focusing on improving its profitability through margin expansion. In the third quarter, its operating margin contracted by a meager 50 basis points to 27.8%, well ahead of the management’s guidance for margins of around 25%. Despite industrywide growth challenges, Fortinet has been able to meet and exceed its operating margin goals, thanks to the company’s strong focus on reducing operating costs.

As a result, when growth accelerates in the next phase of the business cycle, Fortinet will be in a much better position to convert favorable macro conditions into higher earnings.

There are many reasons to be optimistic about Fortinet’s future. First, Fortinet has a platform approach to the business, and the company is focused on providing 360-degree solutions that address the entire spectrum of cybersecurity needs of its clients. This approach addresses the challenge of data silos that can arise as a result of a company using different solutions providers for different types of security needs.

Through three distinct product categories – Secure Networking, Security Operations, and Universal SASE – Fortinet offers a comprehensive set of solutions, including security convergence across all edges and users, real-time threat monitoring, and secure networks to access data on the cloud.

Fortinet’s focus on addressing all security needs of its clients is likely to pay off handsomely in the future, as this will help the company enjoy competitive advantages compared to many of its peers who specialize in one product category.

Second, the increasing adoption of cloud computing and digitalization will drive the demand for best-in-class security solutions in the future. According to a recent survey conducted by Cybersecurity Insiders in partnership with Fortinet, 39% of organizations are hosting at least 50% of their workloads on cloud platforms.

Also, cloud penetration is expected to reach 58% within the next 18 months. This growing prevalence of cloud computing has opened new doors for attackers, and companies are planning to aggressively invest in IT infrastructure to prevent unauthorized users from gaining access to sensitive corporate data.

Fortinet is diversifying into the cloud security space aggressively and is well-positioned to capture a meaningful share of this fast-growing market with its suite of products.

Third, Fortinet continues to attract high-value clients, which opens the door to new revenue streams in the future by upselling and cross-selling products to customers with a high spending capacity. In the third quarter, Fortinet closed 145 deals worth more than a million dollars on the back of five consecutive quarters of closing more than 100 deals valued at $1 million or more. Fortinet’s growing prevalence among large organizations bodes well for its long-term growth potential.

Finally, the increasing number of security threats and attacks will force organizations to take cybersecurity more seriously in the future, enabling Fortinet to thrive. In the second quarter of 2023, the worldwide cybersecurity market grew by 11.6% year-over-year to $19 billion, according to tech market analyst firm Canalys.

Interestingly, more than half of cybersecurity spending came from the top 12 vendors in Q2, and Fortinet came second behind Palo Alto Networks (NASDAQ:PANW). According to Canalys, reported ransomware attacks are up more than 50% this year, and 2023 is on track to dethroning 2021 as the worst year from a cyberattack perspective.

The growing threat posed by cyber criminals will force organizations to aggressively embrace security solutions, and Fortinet is poised to take advantage of this expected surge in security spending.

Is Fortinet Stock a Buy, According to Analysts?

Following the release of Fortinet’s third-quarter earnings, many analysts have cautioned about the short-term outlook for the company. HSBC slashed its price target for Fortinet from $75 to $49, citing competitive threats in the SASE (secure access service edge) segment. In addition, Cantor Fitzgerald slashed the price target for Fortinet from $75 to $50, while Stifel analysts lowered the stock’s price target to $52 from $69.

A common theme found in recent analyst notes is the lackluster outlook for billings growth through the second quarter of 2024.

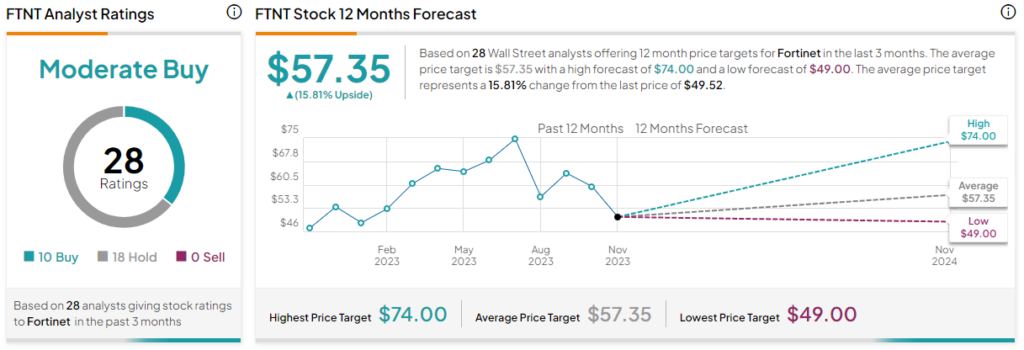

Nonetheless, based on the ratings of 28 Wall Street analysts, FTNT earns a Moderate Buy consensus rating, and the average Fortinet stock price target is $57.35, implying 15.8% upside potential.

The Takeaway: Fortinet Should Thrive in the Long Term

For Fortinet investors, the next couple of quarters could prove difficult. Still, those with a long-term investment strategy should consider the company’s initiatives to enhance operational efficiency and expand its product offerings, aiming to provide a comprehensive cybersecurity platform to both current and prospective clients. Therefore, the recent market pullback presents an attractive entry point for investors with a long-term perspective.