Mobile sports betting operators are moving all their chips into one basket. In this case, those chips are an open service broker platform, and the basket is the in-house technology of SBTech, acquired by DraftKings Inc. (DKNG).

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Four-star analyst Jed Kelly of Oppenheimer & Co. covered the stock, detailing the announcement made by the online sports betting company. He wrote that the migration of the platform to SBTech from the Kambi Group (KMBIF) will provide DraftKings with the opportunity to operate new betting services, most notably one called Same Game Parlays (SGP). This form of sports betting has gained in popularity as of late. (See DKNG stock charts on TipRanks)

Kelly assigned a Buy rating on the stock, and provided a price target of $80. This reflects a potential 66.46% upside from the Friday closing price of $48.06.

SGPs are anticipated to help increase gaming revenues and their yields, said Kelly. He came to this conclusion after analyzing the transition efforts made by several similar sports betting companies, such as FanDuel (not publicly listed). FanDuel has a more vertically integrated technology ecosystem than DraftKings, and as such higher yields are achieved.

The analyst was encouraged by the fact that DraftKings has strong user engagement, and that even if SGPs will not be implemented until Q3, its customers are likely to stick around long enough for the new betting options to become operational. He explained that at that point, DKNG can potentially “close the yield gap with its peers,” in turn creating more upside for the stock price in Q4.

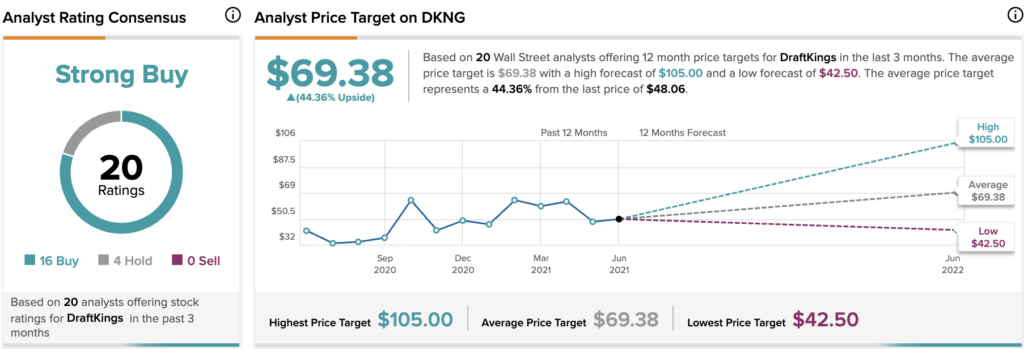

On TipRanks, DKNG has an analyst rating consensus of Strong Buy, based on 16 Buy and 4 Hold ratings. The average analyst DraftKings price target is $69.38, suggesting a possible 12-month upside of 44.36%.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.