The energy business is notoriously cyclical, following ups and downs in the economy, facing headwinds of supply and demand – and gaining from tailwinds when trends start looking up. That’s happening now in the natural gas sector, where a combination of increasing demand and a need for additional infrastructure is creating a bullish situation in the midstream energy stocks.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The midstream companies hold a vital position among the energy players, providing the services needed to move crude and processed fuels from the production sites through the pipelines and storage facilities to the refineries and distribution points.

According to Citi analyst Douglas Irwin, the compression market – an important link in the natural gas supply chain – is particularly well positioned for gains given current conditions.

“We expect an already tight compression market to benefit from several ongoing macro tailwinds, most notably increasing natural gas demand over the near-to-medium term,” Irwin says, and goes on to add, “Specifically, we estimate the potential for as much as 20+ bcf/d of incremental natural gas demand through 2030, which would roughly translate to a call for ~12 million horsepower (HP) of incremental compression capacity in the US. This would represent a ~20% increase over estimated current operating capacity, which we expect to result in incremental fleet additions, increasing utilization rates, and continued upward pressure on prices.”

Irwin follows these statements with some specific recommendations on midstream stocks that are poised to benefit from that series of strong tailwinds. Opening up the TipRanks platform, we’ve looked up his choices – and found that they get Strong Buy ratings from Wall Street. Let’s take a closer look.

Kodiak Gas Services (KGS)

First up, Kodiak Gas Services provides large-scale gas compression services on a contract basis, for field gathering, enhanced oil recovery, gas lift, and processing. The company has well over 4 million horsepower of operating equipment in its fleet, and boasts that this fleet is the most energy-efficient, and newest, in the industry. Kodiak can design, build, and commission compressor stations and other natural gas midstream infrastructure, as well as contract for operations and maintenance of customer-owned infrastructure and equipment.

All of this makes Kodiak a leading provider of compression services in the US energy industry. The company operates in all of the major hydrocarbon production regions of the US, with a particularly strong presence in the Permian basin of Texas. Kodiak claims, with reason, that its services are critical in enabling its customers to meet the natural gas and oil demands of the global economy.

Kodiak went public through an IPO in the summer of last year, and since then has seen steady gains in its share price. Year-to-date, the stock is up 51%, a strong outperformance when compared to the ytd gain of 20% on the S&P 500 index. We should note that Kodiak’s quarterly revenues were steady near $200 million in its first four public earnings reports, but took a dramatic jump upwards in 2Q24.

That second quarter report saw Kodiak bring in $309.7 million, for a 52% year-over-year increase – although it slightly missed the forecast, coming in $1.76 million below the estimates. At the bottom line, Kodiak brought in earnings of 6 cents per share by GAAP measures. The company generated a discretionary cash flow in the quarter of more than $90 million.

For analyst Irwin, in his coverage for Citi, the key item to keep in mind about Kodiak is the company’s solid position in the industry. As he says, “We believe KGS is well positioned to capitalize on a tight and growing market for a few reasons. First, KGS offers the largest fleet among peers with ~4.5 million HP. Second, this fleet is strategically positioned with >80% of capacity located in the Permian or Eagle Ford, which we expect to see meaningful demand growth as US LNG capacity is poised to more than double over the next five years. Finally, KGS offers peer-leading utilization rates (~97% 2024 Citi estimate) and revenue / HP, both of which we expect to continue to improve over time.”

Looking ahead, Irwin believes that Kodiak will bring stronger returns for investors, writing of the stock, “As a result, KGS boasts a rapidly growing FCF profile, which we expect to allow for increased capital returns in the form of a growing dividend and additional potential buybacks moving forward.”

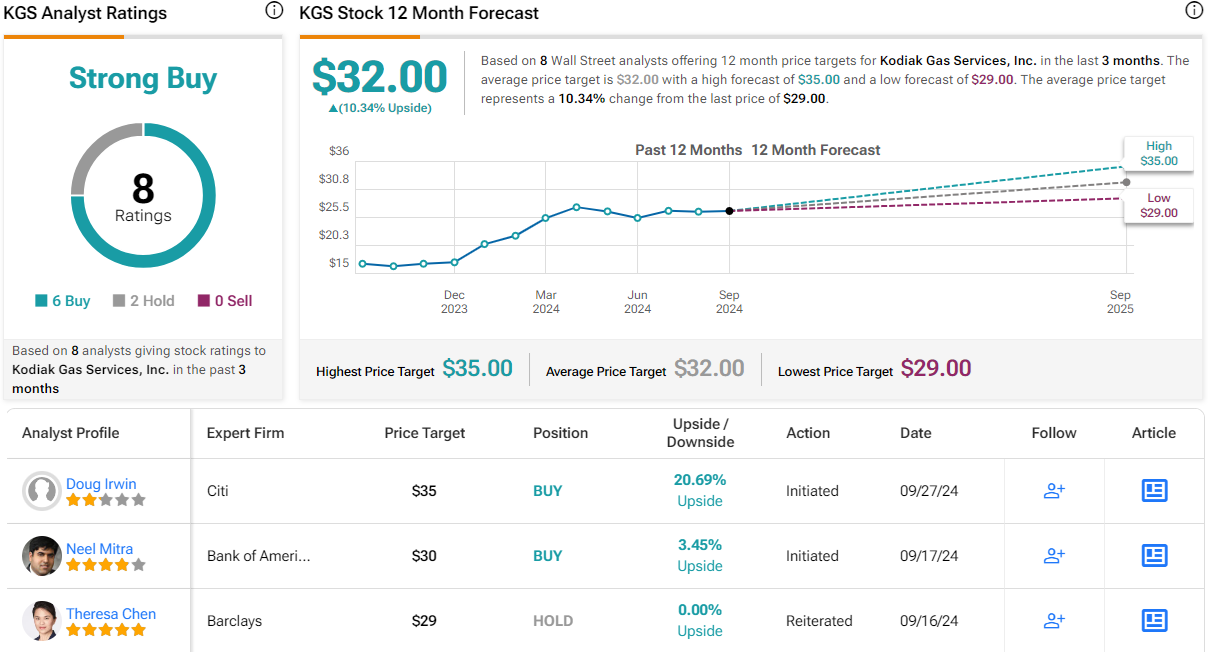

These comments support a Buy rating on the shares, and Irwin’s $35 price target indicates potential for a one-year upside better than 20%. (To watch Irwin’s track record, click here)

This stock’s Strong Buy consensus rating is based on 8 Wall Street reviews that include 6 Buys to 2 Holds. The shares are trading for $29 and their $32 average price target implies a gain of 10% over the next 12 months. (See KGS stock forecast)

Archrock (AROC)

Next up is Archrock, a pure-play midstream company focused on natural gas compression. Archrock provides these services to customers in the oil and natural gas industry across the US, and also provides aftermarket services to customers who independently own their compression equipment. The Houston-based company boasts a market cap of nearly $3.6 billion, and is a premier provider of compression services in the US midstream sector.

Archrock uses its own fleet of compression equipment to provide contracted natural gas compression services. This fleet is based on both traditional and electric motor drive (EMD) compression packages. EMD packages reduce the CO2 emissions inherent in compression operations, and Archrock is the leader in providing this option to the US market. In addition, Archrock provides methane reduction services – important, as methane is a major by-product of all segments of the natural gas industry – and aftermarket services of all types for customers who own their own compression equipment but are looking for greater operational expertise. Archrock brings some 70 years’ experience to the natural gas midstream sector.

We should note here that in August, Archrock completed an important acquisition move, when it closed the transaction with Total Operations and Production Services (TOPS). The acquisition brings 580,000 horsepower of new operating capacity to Archrock. The transaction of approximately $983 million, was conducted in both cash and stock.

Like Kodiak above, Archrock’s stock has outperformed the broader markets this year, with a 35% year-to-date share gain. The company is riding high on increased demand, in both the domestic and export markets, and revenues have been trending upwards for the past several quarters. In the most recent reported quarter, 2Q24, the company had a top line of $270.5 million, up 9% year-over-year and in-line with the estimates. Earnings came to 22 cents per share, up from 16 cents in the prior-year period although it missed the forecast by 3 cents.

Turning again to the Citibank view, as expressed by Irwin, we find the analyst staking out an upbeat position here. Irwin cites Archrock’s overall success, its position in a growing industry, and its acquisition activity, writing of the firm, “We model a peer-leading 2-year EBITDA CAGR of ~15%, which we expect to be driven by several factors. The first is continued organic growth on the base business. With ~2/3 of the fleet located in the Permian and Eagle Ford, we expect AROC to continue to benefit from natural gas demand tailwinds such as incremental LNG capacity… Second, we expect AROC to benefit from continued pricing tailwinds in a structurally tight market – we model low-mid-single-digit growth over the next two years.”

“Finally,” Irwin further added, “AROC recently completed the TOPS acquisition, which we expect to drive an incremental ~$140mm of EBITDA (pre-synergy), adding >500k HP to the fleet and providing exposure to a growing electric HP market.”

Irwin’s stance is congruent with his Buy rating on the stock, and his price target, set at $24, implies the stock has a potential one-year upside of 18.5%.

The Street has given Archrock a consensus rating of Strong Buy and it is unanimous, resting on 6 recent positive analyst reviews. The shares have a trading price of $20.24 and an average target price of $23.80, suggesting an upside of 17.5% by this time next year. (See AROC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.