The CPU market is going through a big resurgence, driven largely by rising demand for processing power tied to agentic AI workloads in data centers.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The surge in demand requires a rethink around expectations for the segment, and that is why Citi’s Atif Malik, an analyst who ranks in 3rd spot amongst the thousands of Wall Street stock experts, has now updated his server CPU TAM model.

Malik reckons the CPU TAM could grow from $29.3 billion in 2025 to $131.5 billion by 2030, reflecting a 35% CAGR (compound annual growth rate). Within this, he expects general-purpose CPUs to expand at a 20% CAGR to $50.9 billion by 2030, AI head nodes to grow at a 21% CAGR to $21.1 billion, and agentic CPUs to rise sharply at a 185% CAGR to $59.4 billion. Based on these estimates, general-purpose CPUs would account for 39% of the TAM in 2030, AI head nodes 16%, and agentic CPUs 45%.

That has also led Malik to update expectations for CPU leaders Intel (NASDAQ:INTC) and Advanced Micro Devices (NASDAQ:AMD).

Factoring in his revised CPU outlook, as well as potential upside from Intel’s ASIC business, particularly its Mount Evans IPU, which is currently used by Google and extends to Anthropic, Malik has raised his INTC data center sales estimates.

Separately, following last week’s news that Intel and Apple have reached a preliminary agreement for Intel to manufacture some Apple chips, Malik anticipates a formal announcement in the coming months, given Apple is “likely incentivized to diversify” its supply chain. Based on industry discussions, he also thinks Intel could eventually secure Nvidia as a foundry customer for gaming GPUs.

As a result, Malik has raised his INTC price target from $95 to $130, suggesting the stock could gain 15% over the coming months. Malik’s rating stays a Buy. (To watch Malik’s track record, click here)

Among Malik’s colleagues, 10 other analysts join him in the INTC bull camp, yet with an additional 24 Holds and 3 Sells, the stock claims a Hold consensus rating. Meanwhile, the $84.82 average price target implies shares are now overvalued by 25%. (See Intel stock forecast)

As for AMD, the 5-star analyst believes the company has secured Anthropic as a customer for its MI450 AI accelerator, based on discussions with industry contacts, and expects AMD to announce the partnership at its Advancing AI event in July. The analyst also thinks AMD could emerge as the biggest beneficiary of the CPU resurgence due to its performance leadership and capacity allocation at TSMC.

However, Malik remains on the AMD sidelines for now. “While we are constructive on AMD’s CPU opportunity on agentic AI demand, we await the release and success of its next-gen GPU product MI450 and Helios racks,” he explained.

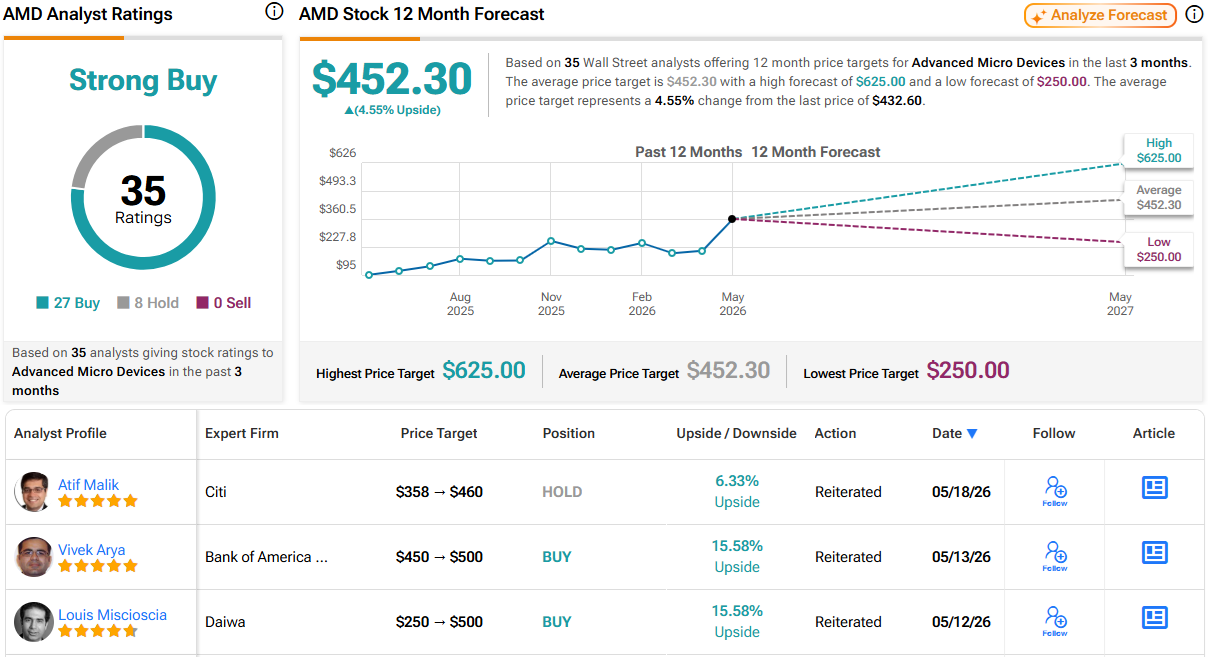

Nevertheless, while Malik maintains a Neutral rating here, he has raised his price target to $460 (up from $358), indicating room for 12-month returns of 6%.

Malik’s take here also differs from the general Street view. Based on a mix of 27 Buys and 8 Holds, the stock claims a Strong Buy consensus rating. At $452.30, the average price target points toward one-year gains of a modest 4%. (See AMD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.