Cadence Design Systems (CDNS), a key player in electronic design automation (EDA) software, has recently seen its stock price drop by 14% over the past month, catching the eyes of investors. This decline is surprising, given Cadence’s strong foothold in the growing AI chip design market and solid financial performance. With Piper Sandler’s recent upgrade to Overweight and a $318 price target, it begs the question: is this dip a great buying opportunity? I think it is, and I’m bullish on CDNS stock.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

My confidence stems from the company’s strong growth in AI-related orders, a promising financial outlook with projected revenue growth of over 13% for 2024, and strategic expansion into new sectors through the BETA CAE systems acquisition.

The recent stock price dip seems like a temporary setback, likely offering a great entry point for investors eager to tap into the fast-growing AI-driven semiconductor market.

Financial Performance and Outlook

Cadence Design Systems is leading the charge in the AI-driven semiconductor market, where demand for advanced chip designs is soaring.

The company’s electronic design automation (EDA) tools have become the go-to for companies looking to create cutting-edge chip designs. The company’s Q2-2024 results didn’t just meet expectations—they exceeded them, setting a positive tone for the rest of the year.

Starting with the headline numbers, Cadence reported revenue of $1.061 billion for Q2 2024, marking a solid 8.6% increase year-over-year. This is pretty impressive, especially considering how tough the market has been for tech companies lately.

Cadence boasts a gross profit margin of 86.9% for Q2 2024, an impressive figure indicating high efficiency in turning revenue into profit. Further, its TTM gross margin of 88.5% is significantly higher than the average of its sector by 1.78x, highlighting Cadence’s operational strength.

So, what’s driving this financial success? A major factor is the Cadence.AI portfolio, which has seen orders triple over the past year. Additionally, Cadence’s nextGen Palladium Z3 and Protium X3 systems are in high demand, underscoring the robust interest in AI-focused solutions. It seems like everyone wants a piece of the company’s AI-focused solutions.

Cadence has raised its revenue outlook, now expecting growth of 13% for the year. This puts its projected revenue in the range of $4.60 billion to $4.66 billion compared to a previous range of $4.56 billion to $4.62 billion. It’s a bold forecast, but it’s one that seems well-supported by the company’s strong product portfolio and growing demand.

Market Recovery Potential

Even though Cadence had strong Q2-2024 results, its performance caused a sell-off, reflecting the overall downturn in the Tech sector. However, despite the recent drop, the stock is still up about 19% over the past 52 weeks. This indicates that the recent pullback might be more of a correction rather than a fundamental shift in the company’s prospects.

Piper Sandler’s recent upgrade of Cadence from Neutral to Overweight is a significant vote of confidence. The maintained price target of $318 implies substantial upside potential of approximately 17% from the current price.

Despite the semiconductor industry’s mixed signals and their impact on Cadence’s growth trajectory, Piper Sandler believes that the company’s year-to-date performance has been largely influenced by specific challenges, such as difficulties during the transition to newer verification technologies (used to test semiconductor designs) and revenue fluctuations in China.

However, as Cadence ramps up verification deliveries in the coming quarters, the firm anticipates a significant improvement in the business optics. This upgrade, coming on the heels of the stock’s decline, indicates that analysts see the current price as an attractive entry point.

Now, I can almost hear you asking about that P/E ratio. At 45.3x, its forward P/E ratio is about double the sector median of 22.8x. Doesn’t that mean Cadence is overvalued? It’s a fair concern, especially given the recent dip in its stock price. But when you look at its growth prospects and how well it’s positioned in high-demand sectors like AI and automotive, that premium starts to make sense.

Expanding Market Presence

Cadence Design Systems’ recent acquisition of BETA CAE Systems is a strategic move that significantly expands its market presence, especially in system analysis. This $1.24 billion deal, involving cash and stock, strengthens Cadence’s capabilities by adding BETA CAE’s top-tier simulation software to its portfolio. It’s not just about new tools; it’s about extending Cadence’s influence in high-growth areas like automotive, aerospace, and healthcare.

Financially, the acquisition is expected to add about $40 million to Cadence’s 2024 revenue and become accretive to earnings by 2025 despite being 12 cents dilutive to the 2024 EPS on a non-GAAP basis. The strategic gains and potential for future earnings make this a calculated risk worth taking.

This expansion comes as Cadence’s core business is already performing strongly, with a record $6 billion backlog and current remaining performance obligations of $3.1 billion. This solid pipeline underscores the company’s operational strength and provides a buffer as it integrates BETA CAE’s operations.

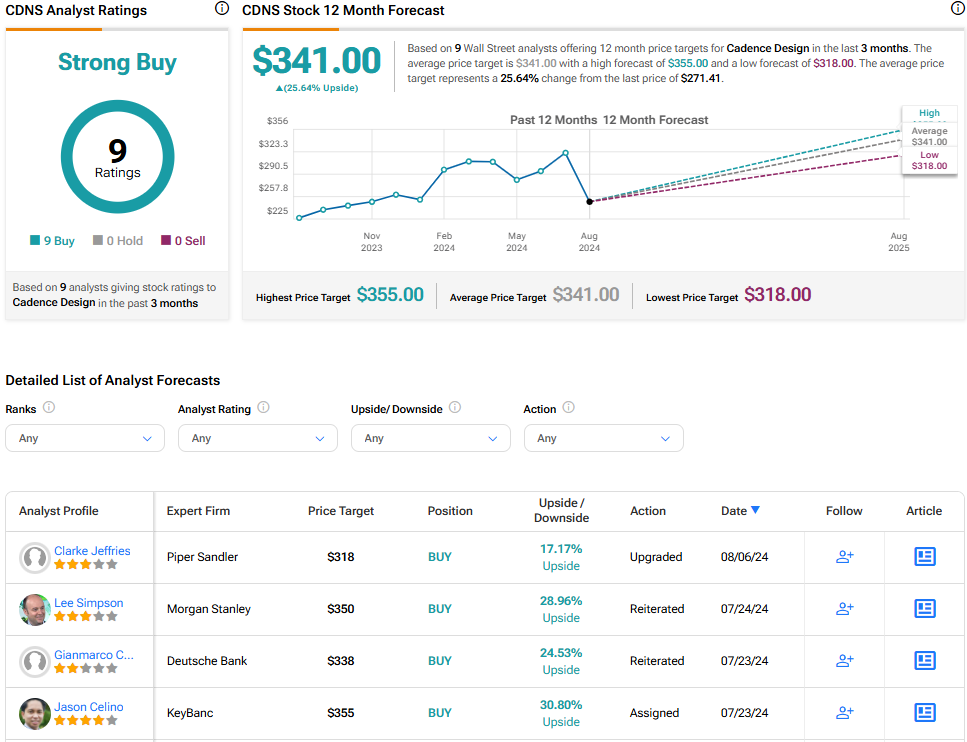

Is CDNS Stock a Buy, According to Analysts?

On TipRanks, Cadence Design Systems (CDNS) stock has a Strong Buy consensus rating. All nine analysts covering the stock rate it a Buy. The average CDNS stock price target of $341.00 implies upside potential of around 25.6%.

The Takeaway

The numbers, strategic moves, and market potential all point to a stock poised for impressive gains. I firmly believe that Cadence Design Systems is a stock worth buying. The recent pullback in its stock price offers an attractive entry point for investors looking to capitalize on this innovative company’s long-term growth potential.