Cabaletta Bio (NASDAQ:CABA) shares have staged an enormous rally in the last year to reach an all-time high, but analysts still see plenty of gains ahead. The clinical-stage biotech firm, which discovers and develops T-cell therapies to treat patients with a variety of autoimmune diseases, has seen its shares more than triple in price over the past 12 months.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Biotech stocks have a history of dramatic spikes and valleys owing to the promise—and potential letdown—of potentially influential new drug treatments. For that reason, CABA’s rally is not out of line with the broader industry. But the fact that analysts across Wall Street forecast that shares will continue to trend upward suggests a unique optimism likely tied to the company’s recent approval by the U.S. Food and Drug Administration for a high-potential Investigational New Drug (IND) application.

I’m bullish on CABA stock for this reason as well, but there are factors both related to the IND and pertinent to the broader industry that warrant a closer look.

Significant Momentum Heading Into 2024

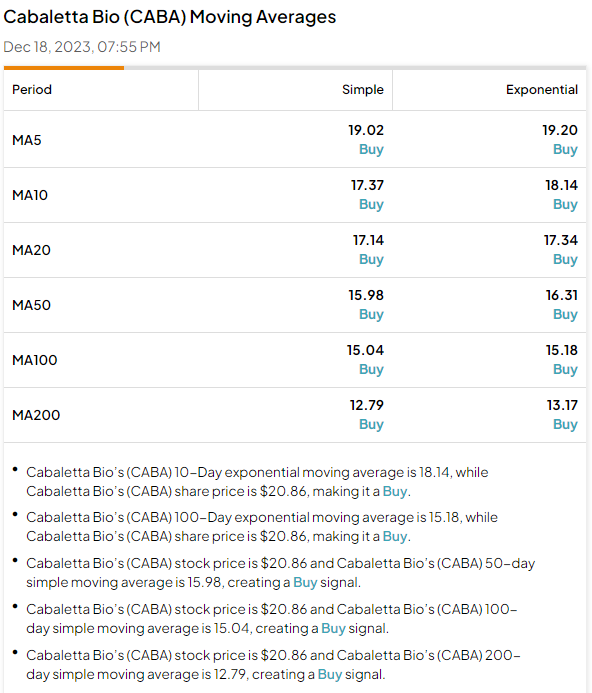

One of Cabaletta’s major advantages as calendars turn over into 2024 is momentum. Trading at $20.86 per share, the biotech firm easily surpasses exponential moving averages for 5-, 10-, 20-, 50-, 100-, and 200-day periods, suggesting a continued upward trend. The price rate of change as of the same day is 9.89, also flashing a Buy signal.

This comes even as a benchmark ETF for the biotech industry, such as the iShares Biotechnology ETF (NASDAQ:IBB), has remained flat in the last year, so Cabaletta’s momentum has outpaced that of its peers.

CABA-201 Approved for Phase 1/2 Study

In November, Cabaletta announced that it had received FDA approval for its fourth IND application for CABA-201, a potential treatment for generalized myasthenia gravis. CABA-201 is an example of a CAR-T cell therapy, which attempts to alter cells within the immune system so that they are able to attack cancer cells.

The company added that it planned to expand its clinical data collection beyond rheumatology and into neurology into 2024, suggesting potentially wide-ranging applications of this drug. One of the most significant is SLE, or systemic lupus erythematosus, the most common type of lupus and an enormous possible revenue source. Indeed, the SLE drug market is expected to reach more than $329 billion by 2032.

FDA Investigation Into CAR-T Therapies

While CABA-201 has no doubt contributed to Cabaletta’s recent stock gains, including the most recent IND approval, there may be reason to be cautious. In late November, the FDA said it was investigating CAR-T therapies based on cancer risks believed to be associated with this class of drugs. CABA’s stock fell in the days immediately following this announcement.

An FDA investigation is a scary prospect, to be sure, but analysts at Cantor Fitzgerald say it’s “likely a storm in a tea cup” and find the news to not be a sign to shift gears when it comes to CABA stock. The reason is that these analysts have already factored in a variety of risks to the eventual possible approval of CABA-201 into their assessments, also noting that INDS related to CAR-T drugs are still being approved and that the investigation does not prove a causal association.

Strong Optimism Despite Being a Clinical-Stage Company

Cabaletta is a clinical-stage company that does not yet have any revenues from the sales of approved drug treatments. So why are analysts so bullish about its future prospects?

One key factor is Cabaletta’s strong cash position relative to many competitors in the high-stakes biotech space. The firm’s Q3 financial report indicated R&D expenses of $13.8 million for the quarter, as well as total cash and related assets of over $164 million. Assuming an annualized cash burn of somewhere above $50 million (similar to its current cash-burn rate), it seems that Cabaletta will easily have enough cash to continue R&D operations at the current pace for more than three years.

This is likely to provide Cabaletta enough cash on hand to advance some of its most promising treatments in the pipeline through all of the stages of clinical trials. Many biotech firms struggle to make it to phase 3 trials at all, so Cabaletta’s position is strong by comparison.

Wall Street Analysts Expect CABA Stock to Rise

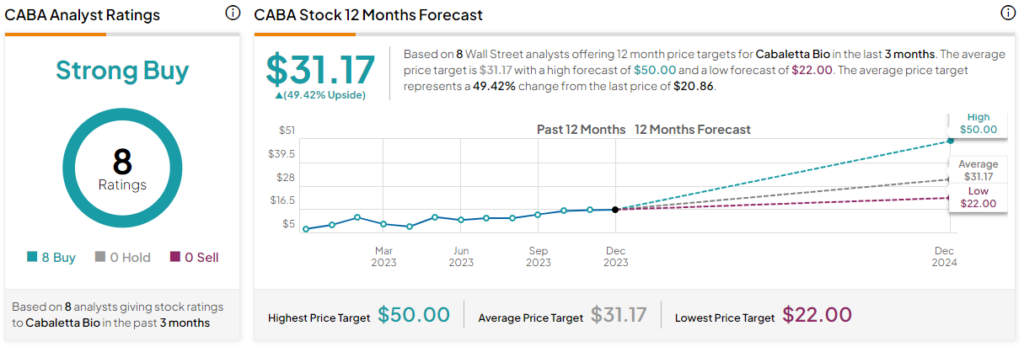

Among Wall Street analysts, Cabaletta enjoys a Strong Buy consensus rating based on eight unanimous Buy ratings assigned in the last three months. At $31.17, the average CABA price target implies 49.4% upside potential.

The Takeaway: Industry-Specific Risks May be Outweighed by Potential

When it comes to clinical-stage biotechnology companies, investors should be prepared for a high-risk, high-reward scenario. Cabaletta’s strong history of stock gains in the last year and Wall Street’s confidence in continued improvement, even as the stock is trading at an all-time high, suggest that the potential of CABA-201 is particularly strong. Backed up by Cabaletta’s solid cash position and recent track record of FDA approvals, investors may wish to look more closely.