The S&P 500 is showing a 6-month gain of 24%. Stocks generally have been gainers as the coronavirus crisis recedes, economies reopen, and the Federal Reserve remains committed to low-rate regime. In this environment, it’s no wonder that many companies are considering going public through an IPO.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The high-return environment we’re experiencing right now makes the IPO attractive as a way to not just raise capital but to also cash in on the rising stock market. With interest rates at historic lows, stocks have become the go-to vehicle for investors seeking growth, and for companies seeking investors – the cohort conducting or contemplating IPOs – the partnership is natural. An IPO brings costs with it, in the form of compliance and disclosure rules – the market’s rapid gains outweigh them for the present.

This brings us to Goldman Sachs. The banking firm’s stock analysts have been looking for the equities primed to gain in current conditions. And just this week, they’ve tapped two stocks new to the public markets as likely to jump 60% or more in coming months – a solid return that investors should note. We ran the two through TipRanks database to see what other Wall Street’s analysts have to say about them.

Compass, Inc. (COMP)

Tech meets real estate in Compass, Inc., a technology company founded in 2012 to make relevant, cloud-based tools available to realtors. The company’s platform facilitates buying, renting, and selling real estate. The company aims to replace the real estate industry’s antiquated ‘paper’ model with a seamless digital experience that empowers agents and satisfies both buyers and sellers.

The company’s large size, and its agent-centered approach, give it advantages over online rivals such as Redfin and Zillow. Compass boasts a 4% market share in the crowded residential segment; by comparison, competitor Redfin’s market share is 1%.

Looking at Compass by the numbers paints an impressive picture. In its fiscal year 2020, Compass employed over 19,000 real estate agents, facilitated over 145,000 transactions with a total gross value of $152 billion, saw top-line revenues of $3.7 billion, and operated in 46 markets across 16 states.

Based on that performance, on April 1, the company went public. Compass put 25 million shares of common stock on the market, at price of $18 each, and netted $450 million.

Among the bulls is Goldman analyst Michael Ng, who likes the fundamental of this newly public stock.

“Compass is the largest independent U.S. real estate brokerage by gross transaction value (GTV) and differentiates itself from competing brokerages by providing its residential real estate agents with a first party, end-to-end platform for workflow and customer management, driving higher annual commissions for Compass agents over time. Compass targets the $2 trillion existing home sales addressable market in the US and, within that, ~$95 bn in annual real estate agent commissions,” the analyst wrote.

Getting to the bottom line, Ng adds, “[We] believe that attractive valuation and adjacent services optionality create a positive risk-reward…”

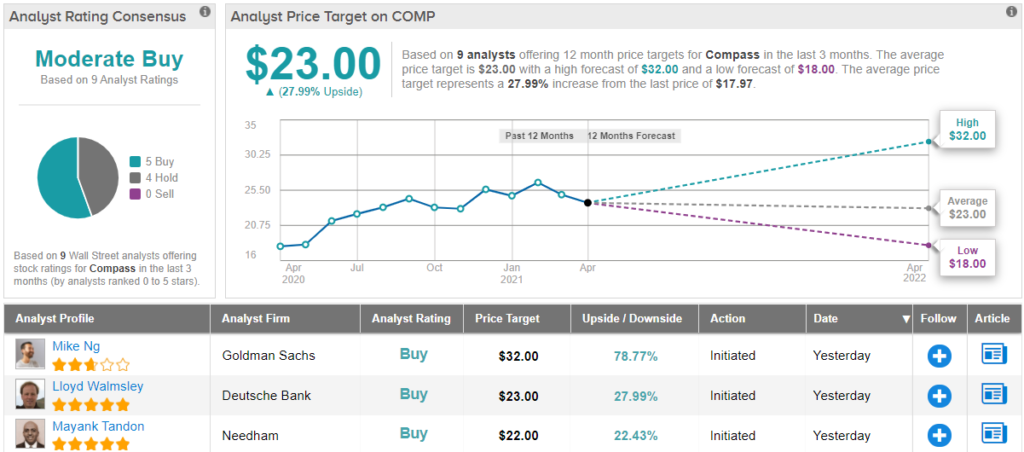

To this end, Ng rates Compass shares a Buy along with a $32 price target. Investors stand to pocket ~79% gain should the analyst’s thesis play out. (To view Ng’s track record, click here)

After less than month in the public markets, Compass has already picked up 9 analyst reviews. These break down to 5 Buys and 4 Holds, giving the stock a Moderate Buy analyst consensus rating. The average price target of $23 implies an upside of 28% from the current trading price of $17.89. (See COMP stock analysis on TipRanks)

Smart Share Global (EM)

Smart Share Global, also called Energy Monster, is a Chinese firm that has staked out a fascinating niche in the digital world: it rents out power banks. The company has backing from Alibaba, and in the last three years has secured a 34% market share and over 219 million users, making it the largest charging service provider in China’s mobile device ecosystem.

Large market share in a large market has brought in the cash. The company’s revenue in 2020 hit 2.8 billion yuan, or $431 million at current exchange rates, and has spread out to encompass a network of 664,000 power bank rental spots across more than 1,500 of the country’s 2,846 counties and local districts. The user base expanded by 47% in 2020.

Smart Share Global started trading on the NASDAQ on April 1, with the offering of 17.65 million shares to the public at an initial price of $8.50. The stock actually opened at $10, and closed that first day at $8.54, putting the total capital raised in the neighborhood of $150 million.

Analyst Ronald Keung, of Goldman Sachs, sees plenty of reasons to buy into Smart Share Global, and in his initiation report on the stock he lays them out.

“We like EM’s: (1) growing network effect, with an extensive national network of 5mn power banks at 664k POIs across 1,500cities (by YE2020), driving better user experience and brand recognition… (2) better-than-peer unit economics with the company picking POIs of high margin/monetization potential, thereby generating Rmb2 daily revenue per power bank, vs peers’Rmb1-1.5. As a result, EM has a very fast cash payback period of five quarters per power bank, which we estimate will lead to double digit net profit margin by 2022; and (3) improving revenue visibility, thanks to key accounts (KA) such as Disney, HTHT, and KFC that are exclusive and long term in nature,” Keung wrote.

Keung puts a $13.90 price target on the stock, to go along with his Buy rating. At current levels, that suggests a one-year upside potential of ~65% for the shares. (To watch Keung’s track record, click here)

The Goldman review is the first on file for this company, which is currently trading for $8.43 per share. (See EM stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.