Ken Fisher has a problem with the Fed, decrying it as ‘idiotic.’ And investors, says the billionaire stock picker, should not pay too much attention to its announcements.

Don't Miss our Black Friday Offers:

- Unlock your investing potential with TipRanks Premium - Now At 40% OFF!

- Make smarter investments with weekly expert stock picks from the Smart Investor Newsletter

“Maybe you’re still worried about what the Fed says,” wonders the Fisher Investments founder. “The September minutes warned of higher rates for longer. But here’s a little secret: The Fed never has a clue what it will do. In May 2022, Fed Chairman Jerome Powell said, ‘a 75 basis point increase is not something that the committee is actively considering.’ The next month, the Fed started doing exactly that – three times in a row.”

Those actions were designed to curb soaring inflation. To be fair, that’s what happened, although it hardly surprised Fisher, who reminds investors that last December he explained why inflation would wane and that it would just take time to do so. Since then, inflation has faded, and it will keep declining, while the bull market will keep pushing ahead, he says.

“The Fed’s 2% annual inflation rate goal is a done deal, just not in the numbers yet. The takeaway: This post-July stock slump is much like the one we saw in December and in the late winter, just slightly bigger and longer from a higher base. Each hiccup sets the stage for the bull market’s next leg up,” Fisher explained.

So, with the bull market set up for more gains, Fisher, who has a net worth of ~7.1 billion, has an idea about which stocks are the ones to take advantage of its resumption. We ran pair of his picks through the TipRanks database to see what the Street experts make of their chances. Here are the details.

ServiceNow, Inc. (NOW)

For our first Fisher-backed name, we’ll turn to the software space and check the details on ServiceNow, a cloud-based platform that offers a comprehensive suite of software solutions designed to streamline and automate various business processes.

The company is known for its exceptional capabilities in IT service management (ITSM), allowing organizations to efficiently manage and resolve IT issues, incidents, and requests. ServiceNow also excels in providing tools for IT operations management (ITOM), enabling businesses to gain greater visibility into their IT infrastructure and optimize its performance. Beyond IT, the platform extends its functionality to various other departments, including HR, customer service, and security operations, making it a versatile enterprise service management solution.

Like many in the tech space, NOW has enjoyed the spoils of the 2023 bull market, with shares having gained 45% year-to-date. In the last quarter reported, for 2Q23, revenue climbed by 23% year-over-year to $2.15 billion, surpassing the Street’s call by $20 million. Adj. EPS of $2.37 also outpaced the consensus estimate by $0.32.

For Ken Fisher’s part, he remains long and strong here. His current NOW holdings total 1,370,996 shares, amounting to a market value of $770 million.

While the stock has performed well this year, against a backdrop of high-interest rates, there have been concerns among investors about decelerating growth. However, this is not a problem foreseen by HSBC analyst Stephen Bersey, who remains confident in NOW’s trajectory.

“We estimate that ServiceNow will continue to demonstrate above-peer performance in 2023e and turnover rising by 23.2% to USD8.92bn,” the 5-star analyst said. “This is above the 22.9% y-o-y growth rate in 2022, and we believe demand conditions remain strong for the company. Fueling this strength, we think that the company’s TAM is large and growing rapidly due to the recent traction in cloud adoptions and digital transformations. For the next year, we estimate that the company will approach a run-rate of USD3bn for revenue by Q4 FY23e and estimate revenue at USD11.1bn for 2024e, growing by 24.4% per annum.”

“We are impressed with the level of growth demonstrated by the company at a high absolute level, and we can recall just a few software companies that have demonstrated this level of growth at a similar scale,” Bersey went on to say.

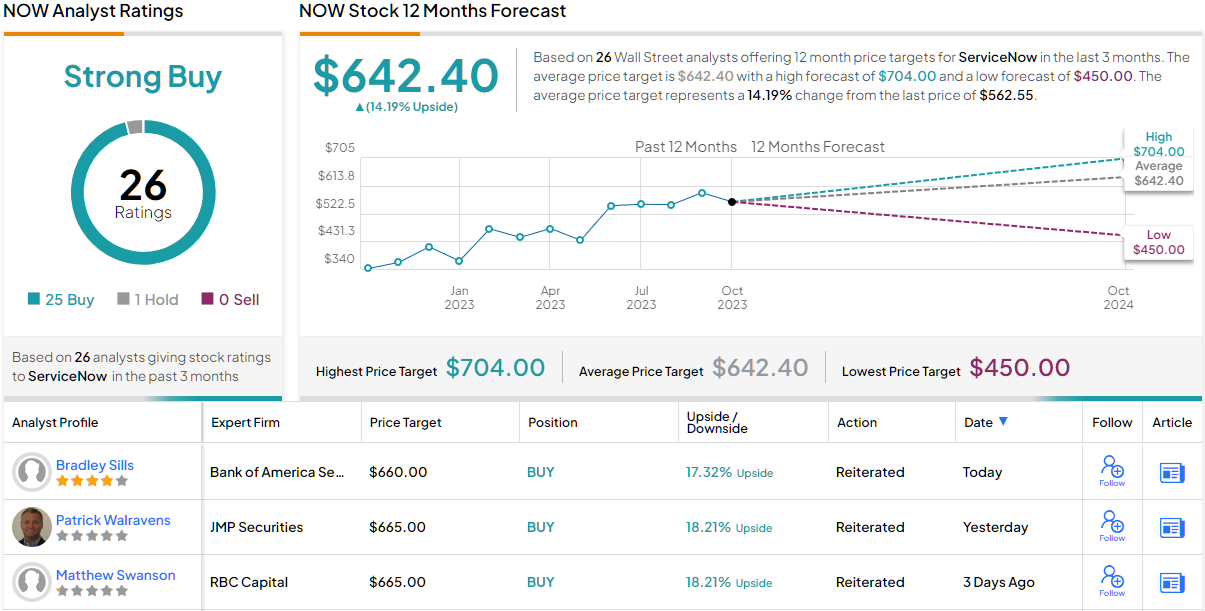

These comments underpin Bersey’s Buy rating on NOW, while his $704 price target makes room for 12-month returns of 25%. (To watch Bersey’s track record, click here)

That take gets almost unanimous support on Wall Street. One analyst currently remains on the sidelines, but all 25 others say Buy, naturally resulting in a Strong Buy consensus rating. The $642.40 average target implies shares will post growth of 14% in the year ahead. (See ServiceNow stock forecast)

Union Pacific (UNP)

Let’s now pivot to something completely different and take a look at Union Pacific, a prominent American transportation and railroad company with a rich history dating all the way back to its founding in 1862.

The company holds a significant place in the nation’s development and is renowned for its vast network of railroads that connect the eastern and western parts of the United States. Union Pacific primarily operates in the western two-thirds of the country, providing essential freight and transportation services across a diverse range of industries. The company plays a pivotal role in the transportation of goods, including agricultural products, energy resources, industrial commodities, and consumer goods, thereby facilitating economic growth and connectivity within the US.

While the company remains essential to the infrastructure of North America, its latest quarterly readout for Q2 had misses both on the top and bottom lines. Revenue fell by 5% year-over-year to $5.96 billion, falling short of expectations by $160 million. EPS of $2.57 missed the forecast by $0.20, falling short by $0.20.

Investors, however, felt somewhat compensated by the announcement of a new CEO, with Jim Vena returning to the company to take hold of the CEO reins from Lance Fritz. Vena served as chief operating officer between 2019 and 2020 and as the chairman’s senior advisor in 2021.

Meanwhile, Fisher has a significant stake in the company, currently owning 5,657,912 UNP shares, which represent a market value of $1.17 billion.

The company also has a fan in RBC analyst Walter Spracklin, who recommends UNP as a ‘high-conviction idea’ and thinks the new CEO is the right one for the job.

“We believe that UNP will deliver further operational progress despite volume headwinds,” opined the 5-star analyst. “Following the announcement that Jim Vena will be UNP’s CEO, we expect that his strong operating philosophy will result in a marked turnaround in operating performance, which we expect will drive O/R and service more toward PSR peers. While cadence of the improvement will be of focus, we have assumed this turnaround is achieved by 2025, resulting in midteen EPS CAGR (with risk to the upside) out to 2025.”

“We also believe that UNP’s competitive dynamics – unparalleled access to Mexico and the chemicals sector in the U.S. Gulf Coast – provide favourable growth prospects in the long run relative to peers,” Spracklin further said.

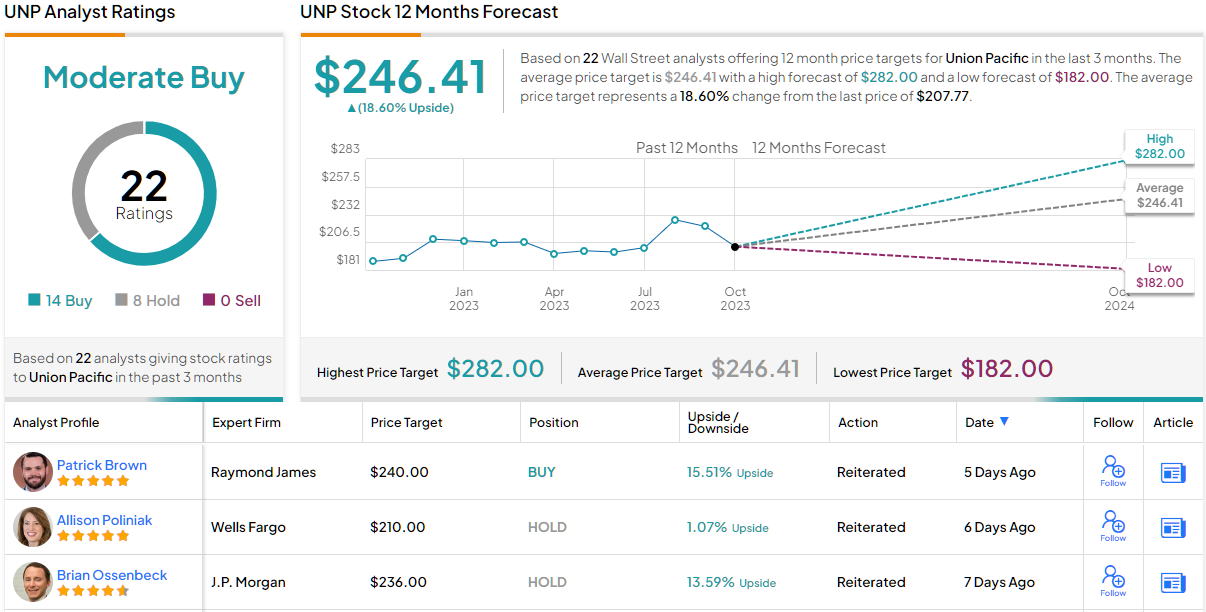

Conveying his confidence, Spracklin rates UNP shares an Outperform (i.e., Buy) and his $282 price target indicates share growth of 36% lies in store for the coming year. (To watch Spracklin’s track record, click here)

Elsewhere on the Street, the stock claims an additional 13 Buys and 8 Holds, for a Moderate Buy consensus rating. Going by the $246.41 average target, a year from now, investors will be sitting on returns of ~19%. Investors should also be aware that UNP provides a regular dividend. The current payout stands at $1.30/share, offering a yield of 2.5%. (See UNP stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.