When billionaire financier Jim Simons makes a move, Wall Street pays attention. Simons is best known as the inventor of quantitative trading, using data crunching algorithms to make market predictions. He put his theories to work in the 1980s, when he founded the Renaissance Technologies hedge fund, and since then has established the best record on Wall Street, averaging a 66% annual return for over 30 years.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Ask how he did it, and Simons will likely tell you that he took the emotional factor out of trading. Humans are fickle beasts, but data never lies. Take out the human factor, focus solely on the numbers and their patterns, and you can’t lose. Following this insight, Simons’ fund has brought in $100 billion in profits since 1988, and his personal fortune totals over $20 billion.

It’s clear that a smart trader can build an investment strategy just by following Simons’ lead. And right now, the 13F filings show that Simons is buying, among others, penny stocks.

These equities, priced below $5 per share, typically offer high upside potentials. Even a small gain in share price – just a few cents – quickly translates into a high yield return. Yes, there is risk involved, but that’s where Simons’ quantitative algorithms come in, to pick the winners.

Looking into Renaissance’s basket of stocks, we’ve chosen three penny stocks that TipRanks database reveals as a “Buy” and offer solid upside potential. Let’s take a closer look and see what Wall Street analysts have to say.

Orbcomm, Inc. (ORBC)

We’ll start with a small-cap communications company. Orbcomm controls both ground-based wireless messaging infrastructure and a network of 31 satellites, giving it global coverage. Orbcomm’s network provides machine-to-machine communications, and is heavily involved with Internet of Things. The company boasts 2 million billable subscribers in 130 countries.

During the first quarter, Jim Simons’ Renaissance upped the ante by 464%, adding 1,150,018 shares of the company to the fund. The fund had first bought into the stock in Q4 2019, with a purchase of 248,000 shares. Its latest buy brought its total holding to over 1.39 million shares, worth $4.8 million.

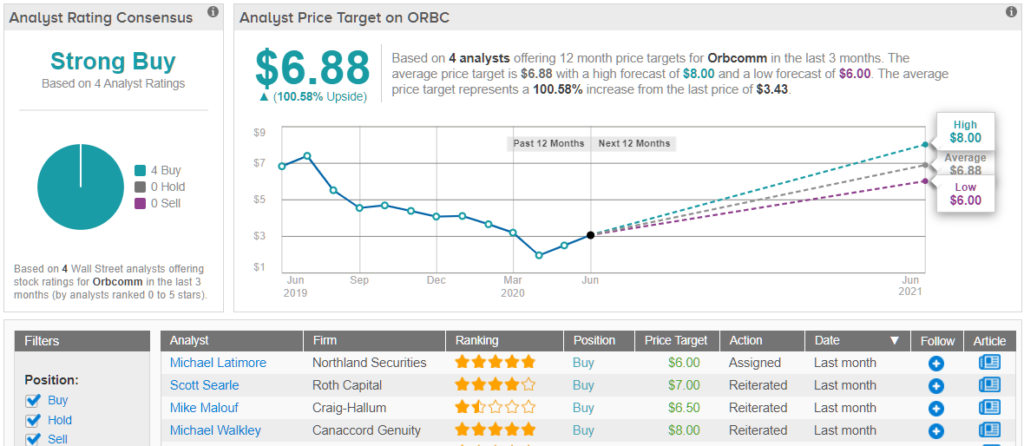

Currently going for $3.43 apiece, some members of the Street believe the share price reflects an attractive entry point.

Canaccord’s 5-star analyst Michael Walkley sees a bright future for Orbcomm, despite the coronavirus pandemic. He writes of the company, “With a portion of ORBCOMM’s business dedicated to helping its customers transport food and medicine during these uncertain times, a strong piece of the firm’s recurring revenues remains protected… we view the risk-reward as very positive…”

The analyst added, “ORBCOMM should be well positioned with its 2.2M subscriber base to drive consistent adjusted EBITDA through its high-margin recurring revenue solutions. Further, its improving cost structure and consolidated platforms should lead to longer-term margin expansion.”

To this end, Walkley rates ORBC a Buy along with an $8 price target. His target implies a wildly robust upside potential of 133% for the coming year. (To watch Walkley’s track record, click here)

Overall, Orbcomm has 4 recent analyst reviews, and all are Buys, making the analyst consensus rating a Strong Buy. The average price target stands tall at $6.88, which suggests the stock has room to double in the next 12 months. (See Orbcomm stock analysis on TipRanks)

Arcos Dorados Holdings (ARCO)

Next up is Arcos, the master franchise holder for McDonalds in the Latin America & Caribbean region. The company is one of the world’s largest McDonalds franchisees, and lists some 20 countries in its franchise territory. Arcos is the largest fast-food chain in Latin America.

Pulling the trigger on ARCO in the first quarter, Renaissance purchased over 563,000 shares. This is a 221% boost to the fund’s holding, and brings its stake in the company to nearly $2.6 million.

As you can easily imagine, the sudden halt in economic activity imposed to stop the coronavirus spread hit Arcos hard, as restaurants were among the businesses most harshly affected. Arcos saw Q1 earnings turn sharply downward, from a 16-cent Q4 profit that was nearly double the forecast to a 26-cent net loss. The Q1 loss was more than 6x worse than analysts had anticipated. Looking forward, Q2 losses are estimated to reach 70 cents per share.

Yet, JPMorgan analyst Ian Luketic believes ARCO’s long-term growth narrative remains strong and that its $4.59 share price reflects the ideal entry point.

Luketic lays out the clear case for Arcos’ return to profitability in the wake of corona: “As stores are reopened and the company is able to adjust its cost structure, we expect to have more visibility on what to expect from margins going forward. Although margins were at a miss, we don´t expect a major negative reaction as the market is already pricing-in weak margins for 2020 and focus should be on results ahead and potential indicators of consumption pick-up.”

Luketic maintains a Buy rating on this stock, and his $5.50 price target implies a 19% upside potential. His is the only recent analyst review on record for ARCO. (To watch Luketic’s track record, click here)

Some stocks fly under the radar, and CATS is one of those. Luketic is the only recent analyst review of this company, and it is decidedly positive.

Adecoagra SA (AGRO)

Last on the list, we have an agricultural holding company. Adecoagra’s subsidiaries operate in crop farming and dairy, along with sugar, ethanol, and even energy production. The company’s field of operations is in Argentina, Brazil, and Uruguay.

The company was hit on two fronts – food production and distribution were impacted by the shutdowns, while forced social lockdown policies put a heavy damper on the fuel market’s demand for ethanol. Yet, AGRO’s niche is essential, and the company is expected to benefit quickly as economies reopen. Demand is already beginning to resume for ethanol, as consumers are starting to purchase more automotive fuel.

Simons’ algorithms are forward-looking, so maybe it’s no surprise that he bought into this company, picking up 415,131 shares in Q1. This holding is worth $1.9 million.

Lucas Ferreira, covering this stock for JPMorgan, noted, “COVID-19 and the oil price decline drove sugar and ethanol prices down by 18%-25% year-to-date and compressed sector valuations and near-term free cash flow generation prospects.” He goes on to add that “the worst seems behind us with domestic ethanol demand surprising to the upside and the gradual reopening to give a further booster to volumes.”

Ferreira’s Buy rating comes with a $6 price target that indicates a solid 31% upside potential from the current share price of $4.57. (To watch Ferreira’s track record, click here)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.