ServiceNow (NYSE:NOW) is benefiting from what looks like a move back into underperforming enterprise software names. The stock is rebounding after experiencing a sharp sell-off. To wit, despite adding ~17% over the past week, shares are still down by ~50% over the last 12 months.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

NOW has been a victim of what has been termed the “SaaSocalypse,” driven by fears that AI agents could take the place of traditional software companies.

However, specifically in NOW’s case, BofA analyst Tal Liani thinks that perception entirely misses the point. “While AI is disrupting the software landscape, we think NOW stands to benefit from, rather than be replaced by, new AI solutions,” the analyst explained. “The starting point is strong, with the company occupying a deeply embedded mission-critical position within enterprise workflows, serving as the system that governs, routes, approves, and audits activity across organizations, making the displacement costly and complex

The analyst believes NOW’s “depth and breadth of workflow entrenchment” leaves it particularly well positioned to benefit from the rollout of autonomous agents across IT, employee, and customer workflows. As these deployments expand, the importance of orchestration, permissions, approvals, policy enforcement, and auditability is likely to increase, all of which closely match ServiceNow’s core strengths, making it the “orchestration layer in an AI-driven cycle.”

Rather than being displaced by AI solutions, Liani expects the company to capture additional value as AI adoption grows. AI Control Tower “defines the strategic role,” Action Fabric serves as the layer connecting workflows, hybrid pricing establishes the monetization model, and the Armis and Veza acquisitions enhance the company’s security and identity capabilities.

Liani sees revenue growth of 18-22% between 2026 and 2028, alongside “best-in-class” FCF margins in the 35-37% range. The outlook is supported by ongoing platform expansion, a rising share of customer budgets, and new AI-related monetization opportunities. “Notably,” says Liani, “cRPO growth has exceeded 20% for five consecutive quarters, highlighting sustained demand and platform relevance.” Management also expects operating and FCF margins to expand by roughly 100 basis points in 2027, indicating further operating leverage despite continued AI investment.

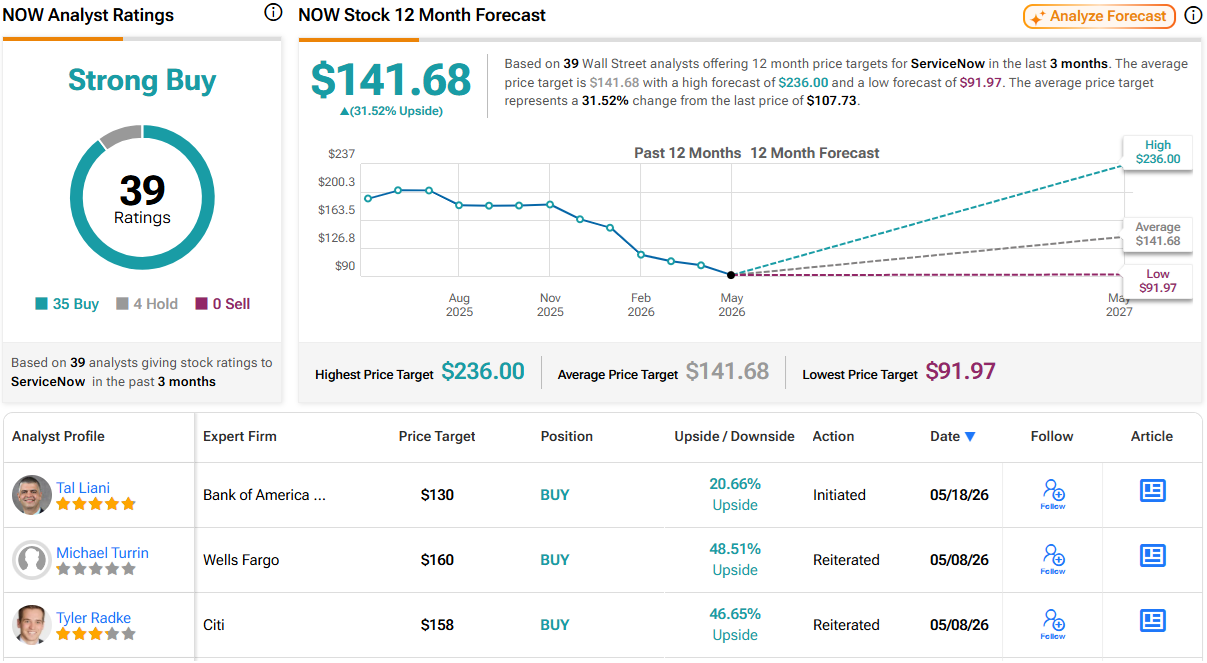

Bottom line, offering “faster growth and superior profitability relative to peers,” Liani calls the stock attractive, and has reinstated coverage with a Buy rating and a price objective of $130, a figure pointing toward 12-month share appreciation of 21%. (To watch Liani’s track record, click here)

34 other analysts join BofA in the bull camp while an additional 4 Holds can’t detract from a Strong Buy consensus rating. The forecast calls for one-year returns of 32%, considering the average target clocks in at $141.68. (See NOW stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.