Align Technology (NASDAQ:ALGN) stock recently fell to multi-year lows on the back of a misaligned quarter that saw demand sag. Indeed, macro headwinds bear most of the blame, given that teeth-straightening treatments aren’t exactly affordable, especially in an environment where everything has become so expensive. Despite the headwinds, I’m bullish on ALGN, primarily due to its valuation and what I view as a promising stage set for a recovery once the economy moves past this inflationary period.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Shares of Align Technology have been one of the market’s biggest losers since topping out back in 2021. It’s hard to believe, but the share price has shed around 74% of its value from its peak. While Align is still an industry leader with some of the most impressive tech in the field, it may prove difficult to stop the analyst downgrades from coming in until there’s more evidence that we’ll be in for some sort of big consumer-spending shift.

Align Feels the Cool Breeze of Macro Headwinds Recession Fears

At the end of the day, most consumers can afford to delay orthodontic treatment until they have enough disposable income again. Though adult demand was weak for the latest quarter, it was notable that the third quarter saw a record number of aligner shipments (up 8.4% year-over-year) to teenagers. That’s an encouraging sign and a testament to the firm having a best-in-breed product. However, without a turn in adult shipments, it will be tough for the stock to pick up any sort of traction again.

Apart from the underwhelming third quarter, management also cut its full-year revenue guidance by about 3.5%. On the whole, the market hated the numbers. However, if you have a long-term view (at least four years), I view Align stock as one of the turnaround plays that could prove very profitable once the economy has a chance to return to its old ways.

Indeed, it’s hard to imagine things could get much worse for Invisalign as recession jitters take hold. At this juncture, the firm may wish to go after the younger crowd to help it smoothen the rough waves created by macro headwinds. Invisalign First, a product meant for younger patients in the 6-10 age group, is an intriguing concept.

Nevertheless, I wouldn’t get my hopes up for a share price turn until adults are ready to open up their pocketbooks again. It’s never comforting to bet on a firm in the face of profound economic uncertainties.

Look for Growth to Recover Sharply Once the Economy Does

It’s impossible to time the market or the economy. But Align stands out as one of the economic recovery winners that many may be overly discounting right now. The company still has a great product. It may be one that’s very economically sensitive, but it’s also one that will probably see brighter days again. In the meantime, investors shouldn’t expect a straight path (forgive the pun) to recovery. It’s a rocky environment, and management can only do so much to spark a turnaround in this type of climate.

In light of macro unknowns, management is wise to guide cautiously. After the recent quarterly guidance downgrade, I think the firm is ripping the band-aid off now so that it can improve its chances of surprising and delighting down the road. For now, I expect the single-digit top-line growth to be more of a temporary “pause” than the start of a negative trend. Align is still very much a growth juggernaut that will be in for a reacceleration once we all feel better about the direction of the economy again.

Additionally, the “pull forward” in demand from the pandemic era may also be another contributing factor behind the sluggish demand for adult aligners. In any case, the effects of the “pull forward” won’t last forever. It has been a few years since lockdown, after all. At this juncture, it’s not hard to imagine that most adults holding off on aligner treatment are doing so due to economic reasons.

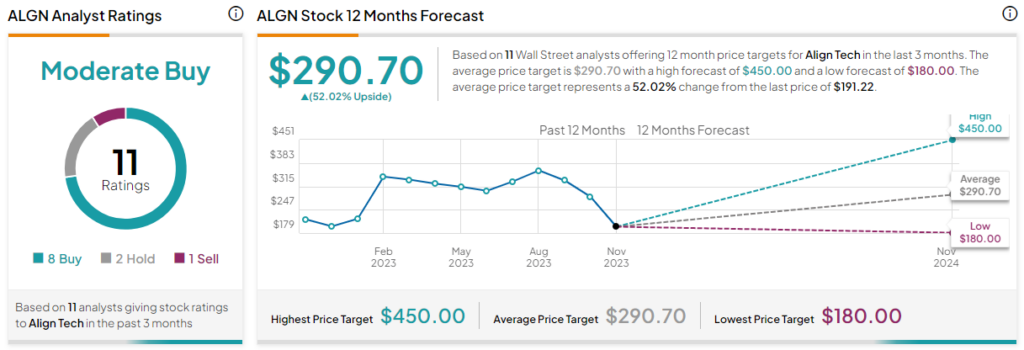

Is ALGN Stock a Buy, According to Analysts?

On TipRanks, ALGN stock comes in as a Moderate Buy. Out of 11 analyst ratings, there are eight Buys, two Holds, and one Sell rating. The average Align Technology stock price target is $290.70, implying upside potential of 52%. Analyst price targets range from a low of $180.00 per share to a high of $450.00 per share.

The Bottom Line on ALGN Stock

Align stock has fallen out of alignment in recent years, but things could turn quickly once the consumer is in better shape. The stock is expected to be a crooked ride for the time being, but if you’re a believer in the technology and the firm’s strong industry positioning, it’s hard to pass up an opportunity to snag shares at multi-year lows.

The stock trades at just north of 20 times forward price-to-earnings, in line with the medical device industry average of 20.65 times. It’s also encouraging that a notable insider, CEO Joe Hogan, has been eating his own cooking, buying about $2 million worth of shares in the past two weeks.