Creative software company Adobe (NASDAQ:ADBE) continues to pave the way for the future of digital media. Its products and services, like Adobe Photoshop, Adobe Illustrator, and more, have earned a massive user base worldwide, which is reflected in its strengthening financials. I’m bullish on ADBE due to its innovative products, reliable revenue streams, proven track record of success, and AI-driven prospects, which some analysts are bullish on as well.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

This year’s AI-driven tech rally has sent tech stocks skyrocketing. Adobe is no exception, with its stock up an impressive 73.7% year-to-date, outpacing the S&P 500’s (SPX) surge of 15%. Furthermore, ADBE has delivered value to its shareholders, appreciating by an eye-catching 940% in the last 10 years.

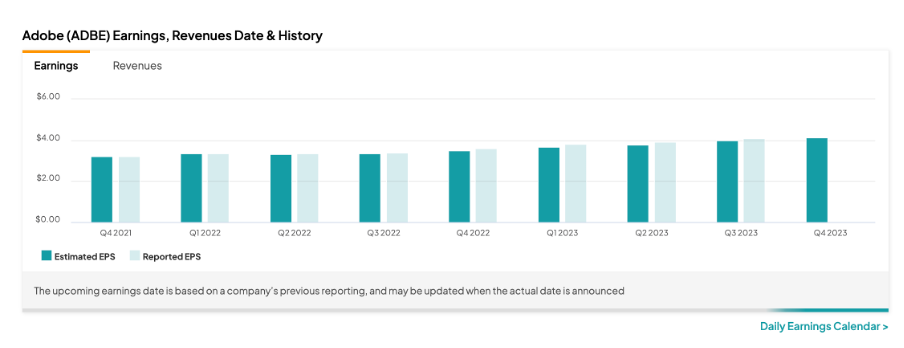

Stellar Q3 Reflects Resilience

Adobe continues to prove its resilience in a challenging macro environment. The firm’s shift to a subscription-based model in recent years has ensured a steady revenue stream. This predictable revenue stream has translated into remarkable profitability and strong cash flows for the company.

In its third quarter of Fiscal 2023, total revenue grew by about 10% year-over-year to $4.89 billion, with subscription revenue accounting for $4.6 billion of that. Meanwhile, adjusted earnings per share (EPS) came in at $4.09 (20.3% year-over-year growth), beating Wall Street’s estimate of $3.98. Adobe has surpassed analysts’ earnings estimates for the last six consecutive quarters.

Moreover, with the increasing demand for digital content creation, augmented reality, and AI, Adobe has been heavily investing in research and development (R&D) to innovate its product offerings. For the nine months ended September 1, it spent $2.58 billion on R&D.

Bright Future with Untapped AI Potential

AI remains a major growth driver for Adobe. In March, it debuted Firefly, a “family of creative generative AI models,” according to the company, made for creating high-quality images and text effects. Firefly has now been integrated into Adobe products such as Document Cloud, Creative Cloud, Experience Cloud, and Adobe Express, according to the company.

Furthermore, in the Q3 earnings call two months ago, the firm stated that it made Adobe Firefly for Enterprise available to businesses “to enable both creative teams and knowledge workers to confidently deploy AI-generated content.”

In June, it also launched Adobe Sensei generative AI services across Adobe Experience Cloud, intending to increase enterprise productivity.

The untapped potential of AI-powered content platforms adds a new dimension to Adobe’s already strong market position. Once monetized, its AI-driven improvements in content curation, creation, and user experience position it to harness significant growth potential.

Talking about AI, Adobe’s CEO Shantanu Narayen stated in the Q3 earnings call, “We are bringing generative AI to life across our portfolio of apps and services to deliver magic and productivity gains.”

Looking ahead, for Q4, Adobe’s management is optimistic about achieving total revenue in the range of $4.975 billion to $5.025 billion, while adjusted EPS is forecast to be in the range of $4.10 to $4.15. Meanwhile, analysts forecast EPS of $4.13 on total revenue of $5.01 billion for Q4.

For Fiscal Year 2023, analysts predict EPS of $15.93 on revenue of $19.4 billion. These figures mark increases of 16.2% and 10.1%, respectively, compared to Fiscal 2022.

Is ADBE Stock a Buy, According to Analysts?

Now, let’s turn to Wall Street. On October 26, Oppenheimer analyst Brian Schwartz upgraded the stock to Buy from Hold, citing Adobe’s strengthening fundamentals, optimistic Fiscal 2024 outlook, and generative AI driving future opportunities. According to the analyst, Firefly has solidified Adobe’s product portfolio, putting it in a good position for consistent growth. The five-star analyst has a price target of $660 for ADBE.

Furthermore, DA Davidson analyst Gil Luria also upgraded the stock to Buy from Hold, citing Firefly as one of the company’s most significant product launches to date, “indicating Adobe’s agility and ability to leverage its scale to defend its moat while introducing a new revenue source.” The analyst also increased the target price to $640 from $500 for ADBE.

Overall, on TipRanks, Adobe stock has a Moderate Buy rating, with 20 Buys, seven Holds, and one Sell rating. The average ADBE stock price target of $609.85 implies upside potential of 4.2% over the next 12 months.

What About Its Valuation?

When it comes to its valuation, Adobe is trading at 32.6 times forward earnings and 12.3 times forward sales for Fiscal 2024. Some investors and analysts believe the stock is overpriced at these levels. However, they may be underestimating the potential that AI could unlock for Adobe in the near future.

The Bottom Line on Adobe

In an era where AI innovation is reshaping industries, Adobe’s subtle but powerful integration of AI within its already successful product portfolio shouldn’t be underestimated. Its strong market position, diverse product portfolio, consistently strong financial performance, and commitment to innovation make it an appealing choice for investors seeking stability and growth in the software industry.