In the investing game, it’s not only about what you buy; it’s about when you buy it. One of the most common pieces of advice thrown around the Street, “buy low” is touted as a tried-and-true tactic.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Sure, the strategy seems simple. Stock prices naturally fluctuate on the basis of several factors like earnings results and the macro environment, amongst others, with investors trying to time the market and determine when stocks have hit a bottom. In practice, however, executing on this strategy is no easy task.

On top of this, given the volatility that has ruled the markets over the last few weeks, how are investors supposed to gauge when a name is flirting with a bottom? That’s where the Wall Street pros come in.

These expert stock pickers have identified three compelling tickers whose current share prices land close to their 52-week lows. Noting that each is set to take back off on an upward trajectory, the analysts see an attractive entry point. Using TipRanks’ database, we found out that the analyst consensus has rated all three a Strong Buy, with major upside potential also on tap.

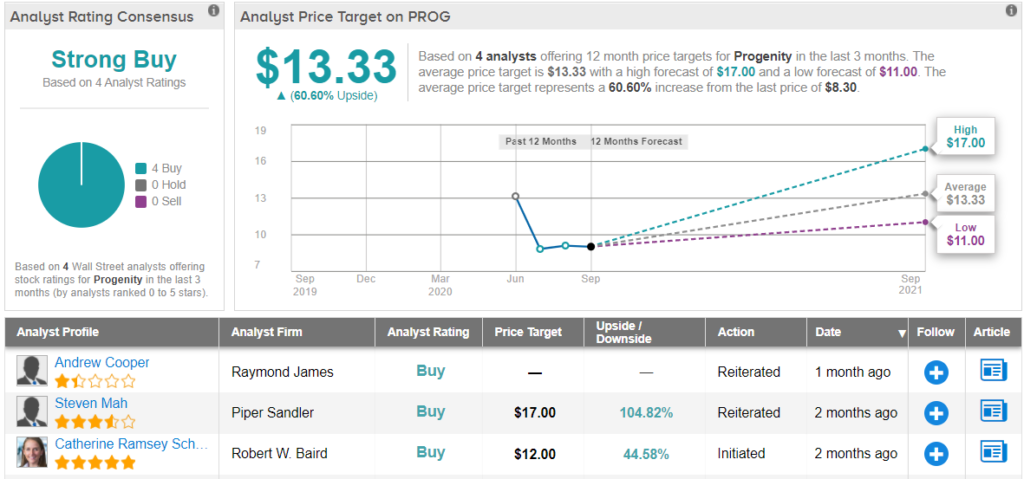

Progenity (PROG)

Offering clear and actionable genetic results, Progenity specializes in providing testing services. The company started trading on Nasdaq in June and saw its shares tumbling 44% since then. With shares changing hands for $8.11, several members of the Street recommend pulling the trigger before it heats up.

Piper Sandler analyst Steven Mah points out that even against the backdrop of COVID-19, PROG managed to deliver with its Q2 2020 performance. “We are encouraged by the recovery in late Q2 2020 with 75,000 accessioned tests (~79,000 in Q1 2020), driven by noninvasive prenatal testing (NIPT) and carrier screening,” the analyst noted.

Expounding on this, Mah stated, “Progenity did not provide guidance, but June test volumes of ~28,000 were strong (Q1 2020 monthly average was ~26,000) which we believe showcases the durability of its reproductive tests and the success that Progenity has in co-marketing and attaching carrier screening to the more essential NIPT. Of note, despite the pandemic disruptions, Progenity was able to maintain its leading pre-COVID test turnaround times.”

Additionally, health insurer Aetna is temporarily extending coverage of average-risk NIPT until year-end as a result of the pandemic, with the American College of Obstetricians and Gynecologists (ACOG) also expected to endorse average-risk in the future given its clinical utility, in Mah’s opinion.

Reflecting another positive, the fourth generation NIPT (single-molecule counting assay) test was able to measure fetal fraction, a key milestone according to Mah, and will continue to be developed into 2021. As the technology could potentially be applied to DNA, RNA, epigenetic markers and proteins for additional clinical applications such as oncology, the analyst is looking forward to the completion of the preeclampsia verification in Q4 2020 and a possible 2H21 launch. “We believe preeclampsia (~2.3 billion serviceable market) is a major differentiator for Progenity, allowing them to cross-sell across the full-continuum of reproductive testing,” the analyst added.

If that wasn’t enough, PROG signed its first GI Precision Medicine partnership agreement with a top-20 Pharma company in August. The Oral Biotherapeutic Delivery System (OBDS), an ingestible drug and device combination designed to precisely deliver biologics systemically through a needle-free liquid jet injection into the submucosal tissues of the small intestine, is set to be utilized as part of the collaboration. Mah commented, “We believe Progenity can sign additional Pharma deals and look forward to the newsflow coming out on this front.”

To sum it all up, Mah said, “We believe Progenity shares are undervalued given the robust recovery in the core testing business and multiple upcoming growth catalysts.”

To this end, Mah rates PROG an Overweight (i.e. Buy) along with a $17 price target. Should his thesis play out, a twelve-month gain of 105% could potentially be in the cards. (To watch Mah’s track record, click here)

Are other analysts in agreement? They are. Only Buy ratings, 4, in fact, have been issued in the last three months. Therefore, the message is clear: PROG is a Strong Buy. Given the $13.33 average price target, shares could climb 60% higher in the next year. (See PROG stock analysis on TipRanks)

Tactile Systems Technology (TCMD)

Developing at-home therapy devices, Tactile Systems Technology wants to provide new treatments for lymphedema, which occurs when the lymphatic system is impaired, disrupting normal transport of fluid within the body, and chronic venous insufficiency. Down 52% year-to-date, its $32.67 share price lands close to its $29.47 52-week low. Thus, with business trends improving, the Street is pounding the table.

Writing for Canaccord, analyst Cecilia Furlong acknowledges that the pandemic has hampered the company, with COVID-19 weighing on both volumes and sales. In the second half of March, volumes were down 50% compared to the first half of the month, and TCMD’s patient volumes in April and May remained challenged. That being said, trends started to improve at the end of May.

“Going forward, given the vast majority of TCMD’s clinician customers practice in outpatient or office-based settings, we remain positive on TCMD’s ability to demonstrate better insulation against COVID impacts and likely experience a greater bounce-back relative to overall med-tech volume trends, with TCMD further benefitting from its expanding using of technology to remotely engage with clinicians and support patients,” Furlong explained.

The analyst added, “Furthermore, recent trends among some providers to prescribe Flexitouch (an advanced intermittent pneumatic compression device to self-manage lymphedema and nonhealing venous leg ulcers) earlier along the therapy process, as a means to reduce in-person contact, could provide upside near term, as well as potentially transition to a longer-term tailwind.”

On top of this, Furlong is also optimistic about new CEO Dan Reuvers and the reprioritization of the company’s investment and market development efforts. TCMD will shift focus away from its acquired Airwear product line, with it redirecting investments toward its Flexitouch and Entre (a pneumatic compression device used to assist in the home management of chronic swelling and venous ulcers associated with lymphedema and chronic venous insufficiency) products.

“Given significant under-penetration in the lymphedema/phlebolymphedema market targeted by Flexitouch alongside the large patient population with limited treatment options today targeted by the firm’s Head & Neck platform, we view the combination of education and clinical data as key to further developing and penetrating these markets… Going forward, we expect management to continue to compile a broad base of clinical data to support reimbursement and drive broad adoption,” Furlong commented.

All of this prompted Furlong to keep a Buy rating and $62 price target on the stock. This target conveys her confidence in TCMD’s ability to soar 90% in the next year. (To watch Furlong’s track record, click here)

In general, other analysts are on the same page. With 3 Buy ratings and 1 Hold, the word on the Street is that TCMD is a Strong Buy. The $62.33 average price target brings the upside potential to 91%. (See TCMD stock analysis on TipRanks)

uniQure N.V. (QURE)

Last but not least we have uniQure, which delivers curative gene therapies that could potentially transform the lives of patients. Even though shares have fallen 44% year-to-date to $40, not much higher than its 52-week low of $36.20, multiple analysts still have high hopes.

Representing SVB Leerink, 5-star analyst Joseph Schwartz acknowledges that shares struggled after news broke of its collaboration and licensing agreement with CSL Behring for AMT-061, QURE’s gene therapy for Hemophilia B, he argues the “shareholder base turnover is likely now complete as investors and QURE shift focus to next-in-line AMT-130, its AAV5 gene therapy for Huntington’s Disease (HD).”

Schwartz further added, “With the M&A premium now out of the stock, we see the QURE’s current level as an attractive buying opportunity for those investors interested in the company’s up and coming CNS gene therapies, internal manufacturing, and robust intellectual property and knowhow.”

Looking more closely at the agreement with CSL Behring, QURE will be tasked with the completion of the pivotal Phase 3 HOPE-B trial as well as the manufacturing process validation and manufacturing supply of AMT-061.

According to management, 26-week Factor IX (FIX) data from all 54 patients enrolled in the trial remains on track, and topline data from the pivotal trial is still slated to read out by YE20. It should be mentioned that in a Phase 2b dose-confirmation study, QURE reported 41% FIX activity out to one year. Additionally, Schwartz points out that with HOPE-B progressing as planned, QURE has continued its manufacturing process validation work ahead of the anticipated BLA/MAA submissions in the U.S. and EU in 2021.

On top of this, as part of the deal, QURE is eligible to receive more than $2 billion including a $450 million upfront cash payment, $1.6 billion in regulatory and commercial milestones and double-digit royalties ranging up to the low-twenties percentage of net product sales.

“With a strengthened cash position, QURE is well funded to rapidly advance CNS assets including AMT-130 (AAV5 gene therapy for Huntington’s Disease (HD)) and AMT-150 (AAV gene therapy for Spinocerebellar Ataxia Type 3/SCA3)…We continue to believe that as QURE’s CNS pipeline assets mature, the company could once again be an attractive partner to larger biopharma companies that have recently acquired many publicly traded gene therapy platforms with substantial manufacturing capabilities,” Schwartz noted.

Everything that QURE has going for it convinced Schwartz to reiterate an Outperform (i.e. Buy) rating. Along with the call, he attached a $67 price target, suggesting 68% upside potential from current levels. (To watch Schwartz’s track record, click here)

What does the rest of the Street have to say? 9 Buys and 3 Holds have been issued in the last three months, so the consensus rating is a Strong Buy. In addition, the $69.89 average price target indicates 75% upside potential. (See QURE stock analysis on TipRanks)

To find good ideas for beaten-down stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.