Doubtless, we’re in an upward market cycle. The S&P is up ~5% in the last 30 days, and the NASDAQ has gained 6%. Good news has buoyed investors’ spirits – news of upcoming COVID vaccine and the resolution of the November elections.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

But those are in the past, and the markets are forward-looking. These gains must be supported by near-term prospects. What we have in the immediate offing is starting to grow clearer. The Biden Administration will be sworn into the office in January, combined with the likely prospect of a partisan split in Congress and a conservative Supreme Court. It’s a recipe for a divided government unlikely – and likely unable – make any radical shifts in policy direction. Meanwhile, the FDA has gave the green light to the Pfizer-BioNTech coronavirus vaccine last Friday, with shipments expected to reach 636 sites this week.

So, in a growth environment, it’s time to look at growth stocks. These are equities that have shown strong share appreciation in recent months and fit a profile: they all have Strong Buy ratings in the TipRanks database, and show double-digit upside potential for the coming year. We’ve pulled up the details on three such investments.

Niu Technologies (NIU)

We will start with Niu Technologies, a manufacturer based in Changzhou in southern China. The company makes and markets electric scooters, a popular product among China’s rapidly growing urban population. Niu was one of the first e-scooter makers to use lithium-ion batteries. The company now markets three lines of scooters, totaling 7 models.

Niu reported $232.9 million in revenue in 1Q20. For the second quarter, the company brought in $644.9 million. And in the recent Q3 report, Niu showed $894.5 million on the top line. That’s 284% revenue growth in 9 months. Q3 EPS, while below the forecast, was still up 25% year-over-year, and reflected a 70% year-over-year increase in sales volume. The company noted a decline in margins, attributed to the ongoing international COVID crisis.

This name has already soared 231% year-to-date, but some Wall Street analysts believe there’s more fuel left in the tank.

Covering this stock for Needham, Vincent Yu writes, “We believe NIU has a clear path for accelerated unit sales growth going into FY2021, driven by store openings, and ASP recovery backed by international market demand and a stabilized product mix… [We] believe blended e-scooter ASP will improve as international markets recover, evidenced by mgt.’s comment that the international order book is strong for 4Q20. Niu’s expansion into new international markets such as Indonesia will benefit the blended ASP, as e-scooter ASPs in these markets will be higher than that of in China.”

In line with his bullish comments, Yu gives NIU shares a Buy rating with a $36 price target indicating room for 27% upside growth in 2021. (To watch Yu’s track record, click here)

Overall, Niu’s Strong Buy consensus rating is based on 4 recent buy-side calls. The stock’s trading price is 28.38, and the average price target of $34.50 predicts ~23% one-year upside from that level. (See NIU stock analysis on TipRanks)

Mr. Cooper Group (COOP)

Next up is a Dallas-based loan servicer in the mortgage industry. Mr. Cooper Group provides a range of services to the mortgage industry, including loan origination, with a focus on the single-family residence market. The economic shutdown last winter hit Mr. Cooper Group hard, but the company has fully recouped its losses since then.

Q1 revenues were down steeply from the previous quarter, but have grown consistently in Q2 and Q3; the third quarter top line results, of $872 million, were the highest in over a year.

Shares of COOP have rebounded well this year. Since hitting bottom at the beginning of April, COOP is up 413%. Year-to-date, the stock is up 122%.

Even with the major share price appreciation, Wolfe analyst Matt Howlett sees a favorable risk/reward profile.

“COOP’s balanced model in the current environment is poised to grow earnings and generate a sustainable double-digit core ROE. The especially strong mortgage banking environment opens a window for the company to paydown its high cost debt and improve their balance sheet. COOP’s strong earnings outlook solidifies the value of the company’s substantial DTA and should allow the stock to trade at a meaningful premium to tangible book in conjunction with peers,” Howlett opined.

Unsurprisingly, the analyst rates COOP an Outperform (i.e. Buy), and sets a price target of $36, suggesting that the stock will grow 30% in the year ahead. (To watch Howlett’s track record, click here)

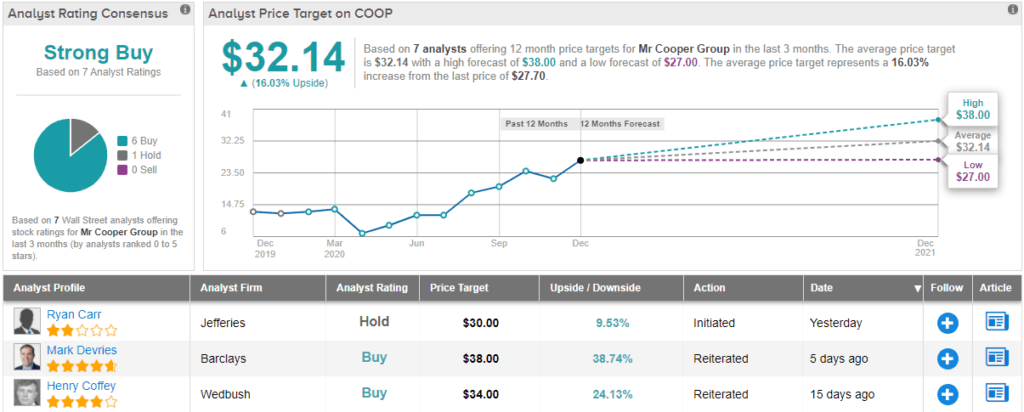

Overall, this mortgage servicing company flashes a strong bullish backing on TipRanks, making this stock a Wall Street favorite. Out of 7 analysts polled in the last three months, six are bullish on COOP stock while only one is playing it safe on the sidelines. With a return potential of 16%, the stock’s consensus target price stands at $32.14. (See COOP stock analysis on TipRanks)

Renewable Energy Group (REGI)

Renewable Energy Group, as its name suggests, is a green economy company, focused on recycled and recyclable alternatives to fossil fuels. The company is based in Iowa – not coincidentally one of the world’s major corn producers – and its main product is biodiesel fuel. The company has operations in the lower 48 states and in Germany.

The policy push toward greener fuels created a market for biodiesel, and REGI has filled it neatly. The company boasted total sales of 176 million gallons in Q3, generating $576 million in revenues. That top line number was up from $545 million in the prior quarter, even though total sales slipped by 2.2%. Fuel production totaled 137 million gallons in the third quarter, up 5.3% sequentially.

REGI’s share performance this year has been impressive. The stock barely registered a blimp when corona tanked the economy, and the shares are up 155% year-to-date.

Wolfe’s 5-star analyst Sam Margolin likes REGI, seeing the company as a market leader in its niche, with plenty of resources to stand on.

“We rate REGI Outperform because of its pure play status as a biofuels manufacturer, deep/diverse relationships with feedstocks suppliers, and logistics capabilities to supply premium markets. The company’s clean balance sheet should enable it to begin returning cash to shareholders even while spending on its large-scale renewable diesel expansion project at Geismar,” Margolin wrote.

Margolin backs his Outperform (i.e. Buy) rating with a $79 price target, implying a one-year upside potential of 22%. (To watch Margolin’s track record, click here)

Overall, Wall Street agrees with Margolin. REGI shares have 6 recent Buy reviews backing the unanimous Strong Buy consensus rating. (See REGI stock analysis on TipRanks)

To find good ideas for growth stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.