Renewable energy installations – mainly wind and solar power systems – have generated their share of controversy, but there is no doubt that the social and political will exists to provide continued support. They are continuing to expand, especially at the utility scale. While inventory surpluses have hurt these sectors, Congress is moving to address permitting regulations, and private enterprises, particularly data centers, are moving to increase their reliance on renewable power.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

This opens up the prospect of a strong expansion in the renewable energy sector going forward, and that prospect opens up a window of opportunity, now, to buy in before the boom. That’s the general thesis behind the stance of Jefferies analyst Julien Dumoulin Smith, who has tagged two renewable energy stocks as Buys. Smith sees them gearing up for gains, and he’s predicting substantial upside for the coming months.

A look at the data from TipRanks shows that both stocks feature positive outlooks from the Street. So, let’s take a look at the details, and at Smith’s commentaries, to find out what else makes them compelling choices in today’s environment.

Sunrun (RUN)

We’ll start with the leading player in the US market for residential solar power installations, Sunrun. This company is a provider of clean energy and energy storage systems and boasts that its products are available to customers with no upfront costs. Sunrun is a full-service provider, able to design solar installations to fit particular houses or other residential sites, install those systems with a custom fit, and add power storage batteries so customers can access energy when they need it. Sunrun’s ‘design to the location’ capability is especially important in the single-family home niche, as many homes, even in ‘cookie-cutter’ development neighborhoods, have been modified by their owners with additions and upgrades.

While solar installations are often thought of as just photovoltaic panels, Sunrun offers much more. The company can connect its installations to the local power grid, allowing customers to make money by selling excess power back to the public utility. It can also provide ‘smart home’ control systems, giving customers options to fine-tune their power generation to meet their needs. Sunrun prides itself on creating custom installations that meet the complete electrical needs of each homeowner.

Sunrun received an overall boost this summer after its competitor, SunPower, declared bankruptcy. Sunrun has the opportunity to snap up some of SunPower’s market share—and sales workers—further bolstering its own leading position in the residential solar market. Additionally, in August, the Federal Reserve indicated that interest rate cuts are imminent. This is also positive for Sunrun, as a large part of the company’s business depends on extending credit terms to customers, which will be made easier by lower interest rates.

In the meantime, Sunrun’s last set of quarterly results, the 2Q24 report, showed a top line of $523.9 million. While down more than 11% year-over-year, this beat the forecast by almost $6.2 million. At the bottom line, the company’s non-GAAP EPS was listed as 55 cents per share, more than double the year-ago value and 80 cents per share above the forecast. Sunrun introduced cash generation guidance in the report, in the range of $350 million to $600 million in the full-year 2025.

Turning to analyst Julien Dumoulin-Smith and his coverage for Jefferies, we find him taking an upbeat view of Sunrun, based partly on the company’s solid position and partly on its potential to increase cash flows. Smith writes, “As the leading clean energy provider under a subscription service, and with over a 60% residential market share of new subscriptions, Sunrun appears well poised to take advantage of the growth in resi-solar after a disappointing 2023. Policy updates from the Inflation Reduction Act (IRA) positions the company to raise even more funding on future assets (via tax equity and non-recourse debt), thereby driving future cash generation and project value. We see upside potential driven by cost deflation, ITC adder monetization, and product mix shift to solar + storage vs. solar only.”

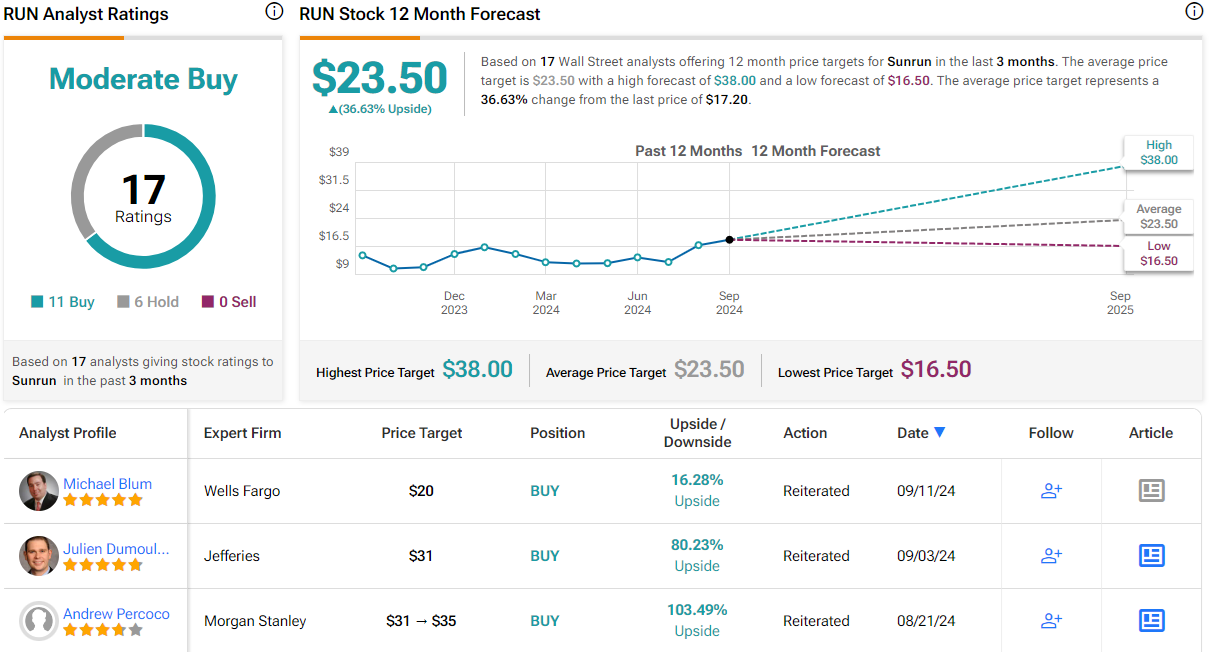

For Smith, this stock is a clear Buy, and his $31 price target implies a one-year upside potential of 80%. (To watch Smith’s track record, click here)

Zooming out, we find that Sunrun gets a Moderate Buy consensus rating, based on 17 recent analyst reviews that include 11 Buys and 6 Holds. The shares are priced at $17.20, and the average price target, $23.50, suggests the stock will gain 36.5% by this time next year. (See Sunrun’s stock forecast)

Fluence Energy (FLNC)

Next up is Fluence Energy, a company that specializes in energy storage. Fluence offers a full ‘ecosystem’ for supporting a clean energy transformation across the economy – a system that includes energy storage products that are modular and scalable; comprehensive service packages to maintain those products; and an AI-enabled software platform, Fluence IQ, to manage and optimize the energy storage system. From a customer perspective, the Fluence system allows for ready customization and easy expansion. The Fluence energy storage system can be installed as small modular units, or as grid-scale systems, or anything in between – and can be readily augmented when necessary. Fluence’s energy storage is also compatible with photovoltaic solar power generation installations.

Fluence offers a wide range of purpose-built energy storage products, so that customers can start their installation at whatever scale is most appropriate. The company makes standard a fully integrated control system good for 2.5 million operating hours. This includes the hardware and software needed to control and monitor the system, and the ability to integrate it with external systems and third-party software applications. Security and firewall capabilities are also included, to maintain a safe system, supported to international cybersecurity standards.

In early August, Fluence reported its fiscal 3Q24 results, showing revenues of $483.3 million. This was down 10% year-over-year – but it did beat expectations by $20.5 million. The company turned a profit in the quarter where a net loss had been anticipated; the quarterly EPS came to 1 cent per share, 13 cents per share better than the forecast.

Two important metrics bode well for Fluence looking forward. The company had a record quarterly order intake, which totaled $1.3 billion. In the same quarter last year, this metric was less than half that value, at $565 million. And, the company’s reported Q3 backlog stood at $4.5 billion as of this past June 30. This represented a significant increase in just three months; the backlog as of March 31 was reported as $3.7 billion. Based on these metrics, Fluence should have plenty of work orders to rely on in the coming months.

Dumoulin Smith sees Fluence in a solid position, and he is impressed by the potential support the company should feel from its backlog. The analyst says, “We believe the backlog acceleration disclosed with the F3Q update implies a significant 2025 revenue acceleration as Fluence launches on domestic content ahead of peers. We expect 2025 to see Fluence pivot to generating real profitability and free cash flow, positioning Fluence for upside earnings and market share gains, justifying a positive rerating.”

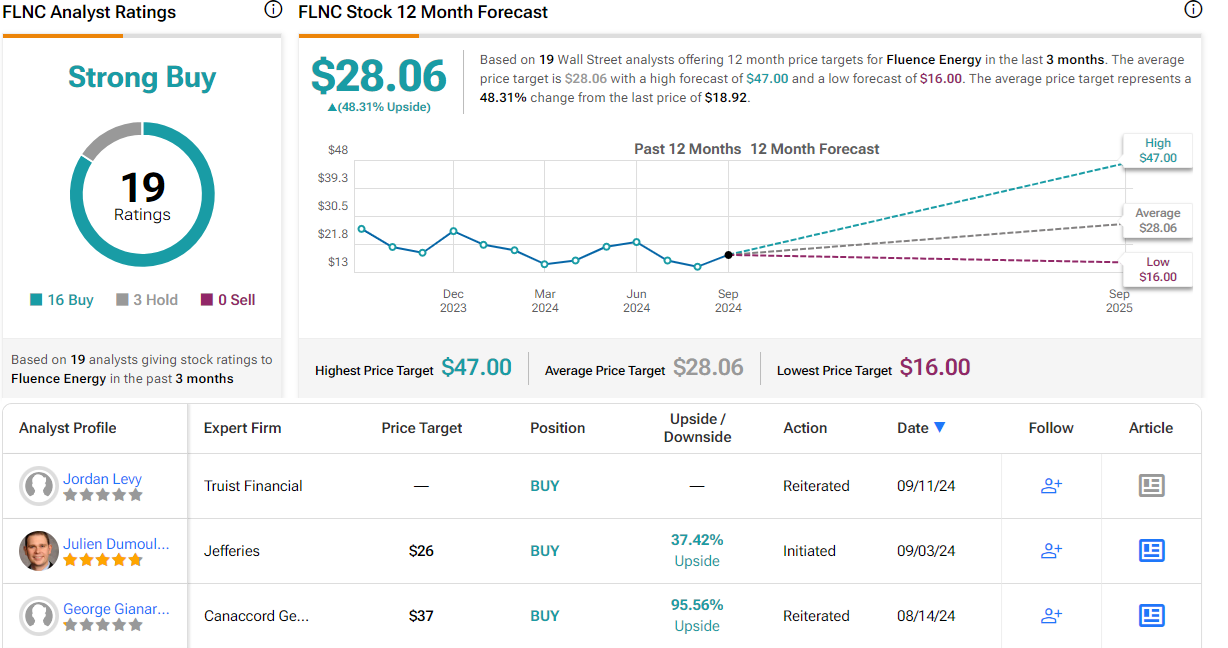

These comments support Smith’s Buy rating, while his $26 price target indicates room for 37.5% share appreciation on the one-year horizon.

Overall, Fluence gets a Strong Buy consensus rating, based on 19 reviews that include 16 to Buy and 3 to Hold. The shares are currently trading for $18.92 and have an average price target of $28.06; these figures imply a potential upside in the next 12 months of 48%. (See FLNC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.