It was not that long ago that Archer Aviation (NYSE:ACHR) was a hot stock, piling on the gains on the prospect of its flying taxi ambitions becoming a reality. However, since peaking in October, shares of the eVTOL maker have shed 63%, as Archer’s progress toward certification of its aircraft has moved at a slower pace than investors had hoped for.

Claim 55% Off TipRanks

Forget margin or options. Here's how the pros trade ACHRCould Ark Invest CEO Cathie Wood be one of those disappointed investors? Known for backing cutting-edge tech, it’s no surprise to see Archer among the forward-thinking names in the Ark portfolio. But now it seems that Wood has begun reducing her ACHR exposure. On Thursday, via the firm’s ARKK fund, she sold 436,322 shares.

Wood’s move is unlikely to be too much of a surprise to J.P. Morgan analyst Bill Peterson, who also understands why investors might be reluctant to get behind Archer right now.

“To become more constructive on the stock, we think investors will need to see significant progress toward piloted transition flight, readiness for TIA testing, Launch Edition aircraft deliveries, and eIPP wins, with further support likely if defense opportunities are pulled forward,” the analyst said.

On its recent earnings call, Archer said regarding certification that the company anticipates a piloted transition flight to take place in the “coming months,” and used similarly vague phrasing regarding the start of TIA testing. This suggests to Peterson a “lack of full visibility on timing and further risk of delays,” which likely does not sit well with investors.

On the plus side, Archer is set to start flying under the eIPP program later this year after being chosen across three states – Texas, Florida, and New York. The program is designed to build operational familiarity for state and municipal authorities while also supporting public acceptance, which would come at an opportune time ahead of the 2028 LA Olympics, where Archer expects to run commercial flights.

But although Archer has recently strengthened its balance sheet, Peterson expects cash burn to pick up over the year, driven by investment in its hybrid program, increased aircraft production, ongoing flight testing, and additional hiring, as reflected in the wider EBITDA loss indicated by the first-quarter guide. Accordingly, further capital raises would not surprise Peterson, as revenue recognition and cost offsets from various programs and awards are likely to remain modest relative to Archer’s continued resource-intensive operations.

“While Archer is building a road map for eVTOL commercialization, we think the market will be slow to ramp, with limited visibility into when FAA certification will occur (despite the goal of ahead of the 2028 Summer Olympics),” Peterson summed up.

To this end, due to the “high risk, but potentially high reward for this story,” Peterson assigns a Neutral rating for ACHR shares, although his $7 price target now offers one-year upside of 37%. (To watch Peterson’s track record, click here)

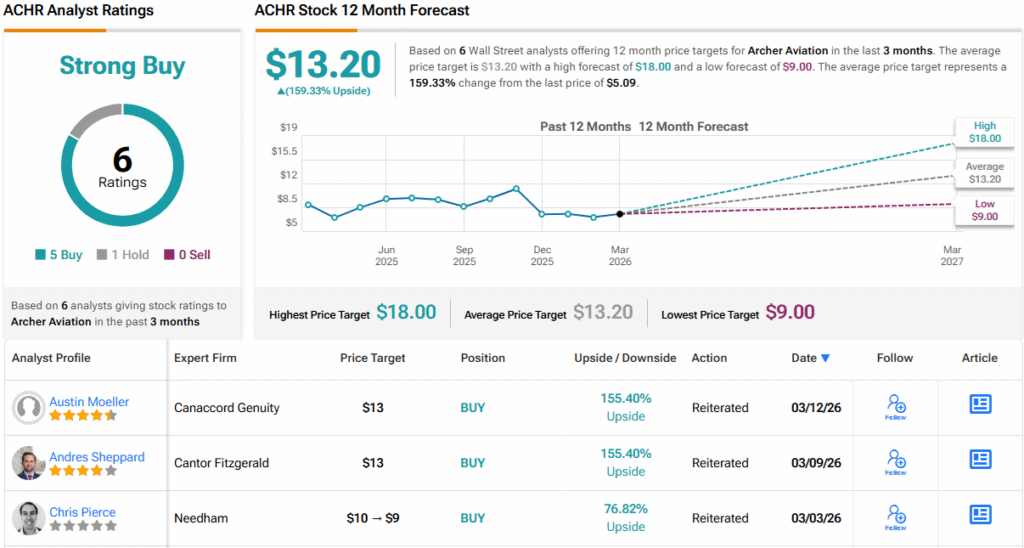

Among his colleagues, Peterson is outnumbered by 5 ACHR bulls boasting Buy ratings, all adding up to a Strong Buy consensus view. The forecast calls for a 12-month upside of 159%, considering the average price target clocks in at $13.20. (See ACHR stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.