Apple (AAPL) is having a stronger year than the market may fully appreciate, setting up the potential for a Q2 surprise. The company is gaining share in a tightening smartphone market, with solid iPhone demand and Services growth helping offset cost pressures. That momentum suggests the current cycle may be more durable than expected, even as sentiment remains relatively cautious.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Scheduled to report its results on April 30 after the market closes, consensus estimates call for earnings per share (EPS) and revenue growth of about 17% and 14% year-over-year, respectively, for Apple’s Fiscal Q2 2026. This would mark the second consecutive quarter of mid- to high-teens growth following a 16% revenue increase and roughly 18–19% EPS growth in Q1 2026 reported in January 2026. My bullish stance on Apple is based on a scenario where the company continues to regain favor with investors, building on the recovery already visible since the March lows.

Apple Is Playing Offense amid the Memory Crunch

Since hitting all-time highs in early December 2025, Apple’s stock came under pressure as the memory price crunch started to become more apparent. It fell from the peak of roughly $286 to nearly $247 in January 2026, and again down to the low‑$240s in mid‑ to late‑March before recovering slightly toward the end of the month.

Bernstein analyst Mark Newman, for example, pointed out in mid-February that average mobile dynamic random access memory (DRAM) contract prices had risen by about 237% since Q2 2025. NAND prices had also jumped by about 70%. This was largely driven by demand for artificial intelligence (AI), with high-bandwidth memory (HBM) sucking up supply from smartphones, pushing up the cost of these components. This is also reflected in the chart below, where Micron (MU) — a direct proxy for memory prices — has significantly outperformed Apple year-to-date.

That said, this very scenario could present a meaningful opportunity for Apple. The company has been making moves that run directly counter to this backdrop, essentially playing offense. Apple is reportedly securing memory supply while keeping product prices relatively stable. At the same time, it is introducing more affordable entry-level models. Of course, this likely comes with some margin pressure in the short term, as the company trades off some profitability for share gains.

Meanwhile, the industry as a whole is contracting, with global shipments down about 6% year-over-year according to research reports. Apple, however, still managed to grow about 5% year-over-year and reach roughly 21% market share, highlighting its relative resilience in the face of the cost shock. In other words, Apple is pressing its advantage. It is leveraging its massive cash reserves and comparatively lower sensitivity to memory costs at a time when competitors are most constrained.

Volume on the Low End, Margins on the High End

Apple is also building a lineup of devices that spans from budget, for example, “E” models, to mid-range, premium, and ultra-premium. The iPhone 17E, along with the low-cost MacBook Neo at $599, expands Apple’s presence at the entry level. At the same time, the redesigned iPhone 18 Pro and a foldable iPhone reinforce its position at the high end. This also supports long-term ecosystem monetization, with the iPhone remaining the central piece of the puzzle.

The same Bernstein analyst also notes that Apple appears to be following a proven playbook from Samsung (SSNLF) in the early 2010s. Back then, Samsung expanded into the lower end to drive volume while pushing further into the high end to protect margins. For that reason, I believe recent revisions to Apple’s EPS for FY26 and FY27 have been trending positively over the past three months. Consensus now points to Apple delivering about 14.3% EPS growth in FY26 and roughly 9.5% in FY27 — slightly higher than earlier expectations, even with margin pressures still in focus.

Assuming these long-term EPS targets prove accurate, Apple would currently be trading at a forward P/E of around 28.2x FY27 earnings. That’s a multiple broadly in line with its five-year average and doesn’t exactly scream cheap. However, it also doesn’t look particularly demanding when viewed in the context of a business of this caliber.

Q2 Looks Solid, but Services May be the Real Driver

With Apple set to report its second-quarter results in late April, it’s hard to see iPhone demand not coming in strong, as usual. The iPhone 17 cycle has been very solid, with record levels of upgraders, something that caught many bears off guard. The series has significantly outperformed the iPhone 16, with sales running roughly 20% higher in early 2026. Much of this strength has been driven by demand for both the base model and the Pro Max.

Yet the AI question still hangs over the story. Unlike its Mag 7 peers, Apple has clearly lagged in deeper AI monetization within its ecosystem. In my view, Apple’s biggest AI-related advantage still ties back to the App Store. It essentially takes a cut of incremental revenue as AI-driven apps scale across its 2.5 billion-device installed base.

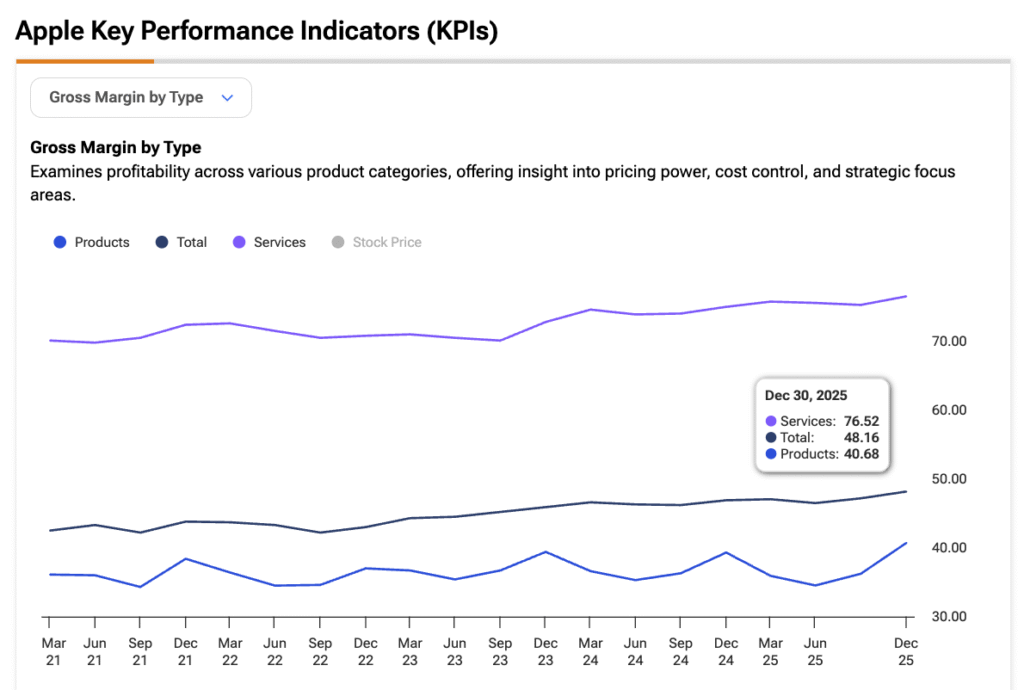

As a result, I see Services as a potentially strong driver of incremental margins this quarter. In Q4 2025, Services accounted for just about 21% of revenue, but drove roughly one-third of total gross profit, reflecting a structurally higher-margin segment. Services’ gross margins are over 76%, compared to the low-40s for Products. While rising DRAM and NAND costs may put some pressure on hardware margins, Services remains largely insulated from these headwinds, effectively acting as a buffer beneath the surface.

Is AAPL a Buy, According to Wall Street Analysts?

Analysts remain mostly bullish on Apple stock. Out of the last 25 ratings issued, 16 are Buy, eight are Hold, and just one is a Sell. Recently revised higher by several analysts, the average price target now sits at $304.85, implying roughly 11.64% upside from current levels.

Playing Offense in a Constrained Market

Apple may not look outright cheap at current levels, but the setup appears increasingly constructive to me — more so than it has over the past several months. With Q2 likely to extend the solid trend in iPhone demand and continued market share gains in a constrained environment, Apple looks well-positioned to navigate near-term headwinds. Services should continue to act as a margin buffer, allowing the company to keep compounding — if not accelerating — earnings.

As such, I view the current risk-reward profile as tilted to the upside and rate the stock a Buy.