Apple (AAPL) is set to report second-quarter earnings after the market close, following strong results from Microsoft (MSFT), Meta Platforms (META), Amazon (AMZN), and Alphabet (GOOGL). Those firms beat estimates and raised AI spending. In contrast, Apple enters the print with a different test. The key issue is not whether the company can post solid numbers, but whether its recent growth can last; can the iPhone 17 cycle last longer with the help of AI features?

Claim 55% Off TipRanks

Trade AMZN with leverageLast quarter set a high bar. Apple reported record revenue of $143.8 billion and earnings per share of $2.84. iPhone revenue rose 23% year-over-year, while Services grew 14%. Management described the period as a “record-breaking quarter” with “strong global demand” and rising margins. At the same time, the company noted supply limits and cost pressure from memory pricing.

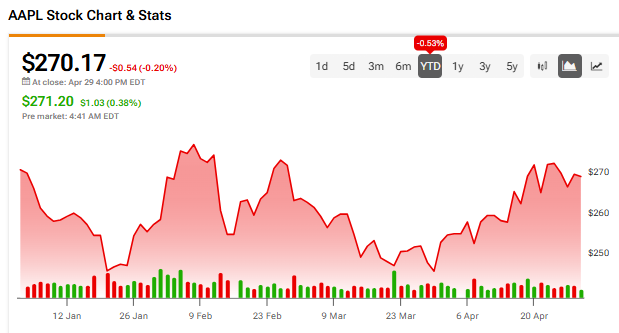

Meanwhile, AAPL shares dropped slightly on Wednesday, closing at $270.17.

The Core Question: Can the iPhone Cycle Continue?

Now, attention turns to the current quarter and what comes next. Wall Street expects revenue near $109 billion and earnings per share of $1.95. However, the stock reaction will depend less on the headline numbers and more on the outlook.

The main focus is whether the iPhone 17 cycle can extend into a longer upgrade wave tied to AI features. Investors want to know if Apple Intelligence is driving real user demand or if recent strength reflects a peak in the cycle. In simple terms, the question is whether growth is slowing or building.

In addition, analysts will look for signs tied to supply and demand. Last quarter included iPhone supply limits. If Apple now reports that supply improved while demand stayed strong, that will support a longer cycle. On the other hand, if demand cooled as supply eased, it may signal that the peak has passed.

Margins, China, and Capital Discipline

Beyond demand, margins will also be in focus. Apple guided gross margin to 48%-49%. Any shift in that range could matter, especially with cost pressure from components. Even a small change in margin outlook can affect sentiment.

Meanwhile, China remains a key region. Apple saw strong growth there last quarter, and investors will want to know if that trend is stable. A steady China outlook could support growth, while any slowdown may weigh on expectations.

Finally, Apple’s approach to AI spending may come into view. Unlike peers, the company continues to return large amounts of cash to shareholders. It also signaled major U.S. investment plans and progress on Apple Intelligence. Investors may look for signs of how Apple balances spending with its capital return strategy.

In summary, Apple’s earnings will not be judged only on recent results. Instead, the call will shape expectations for the next phase of iPhone demand and the role AI may play in sustaining growth.

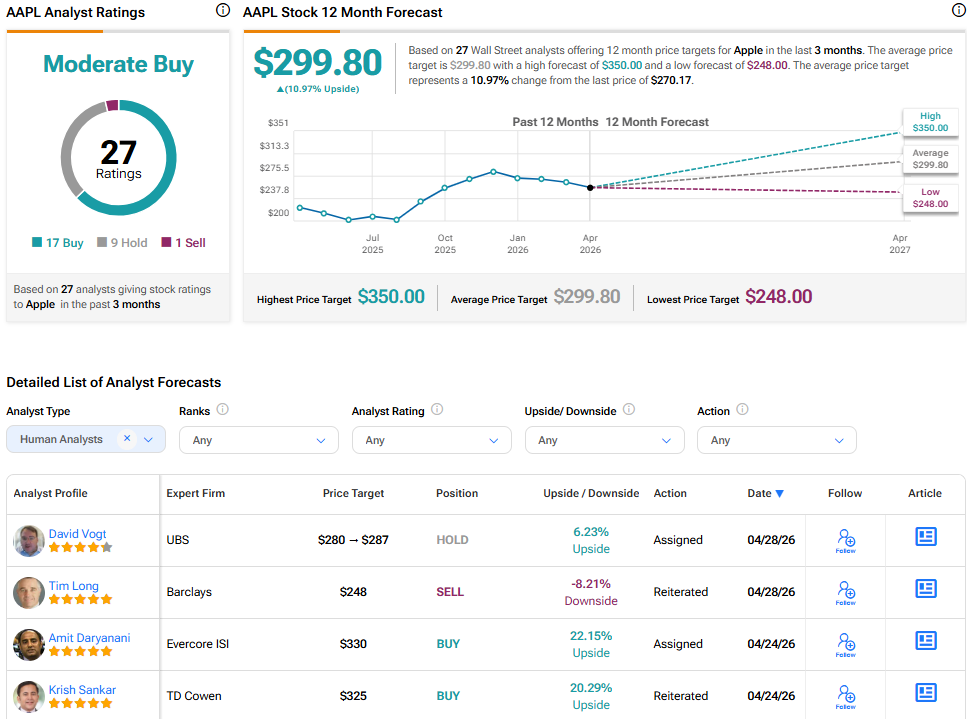

Is AAPL Stock a Buy?

Turning to the Street, Apple has a Moderate Buy consensus, based on 27 analysts’ ratings. The average AAPL stock price target is $299.80, which implies about 11% upside from the current price.