The wheels are certainly turning in the AI space, as the technology continues to develop and advance. One of the biggest shifts now underway is the move from training to inference workloads, which are slated to put CPUs in the front and center of the action.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

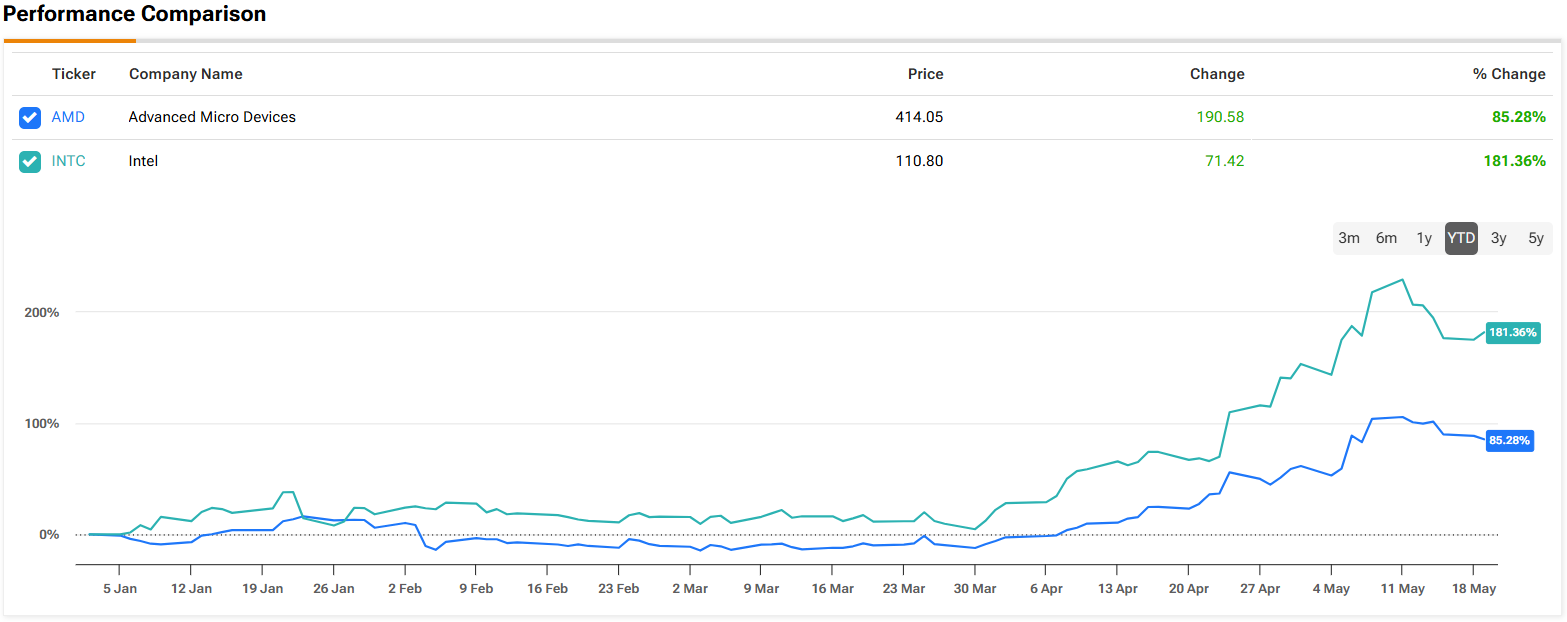

That narrative has received support from two of its biggest beneficiaries: Advanced Micro Devices (NASDAQ:AMD) and Intel (NASDAQ:INTC). In their recent earnings reports, both companies delivered strong AI-powered growth while simultaneously guiding for plenty more.

AMD CEO Dr. Lisa Su now expects the server CPU market to grow by 35% annually through the end of the decade, surpassing $120 billion. That’s a marked increase from the 18% that AMD had previously forecast.

In a similar vein, Intel CEO Lip-Bu Tan shared that demand for the company’s Xeon server CPUs continues to outrun supply. The company’s “top priority” is now working to maximize and optimize factory output to meet this sustained momentum.

Both AMD and INTC have seen their share price catapult up the charts over the past year. AMD stock has climbed more than 290% during the trailing twelve months, while Intel has delivered an even steeper rally, surging about 460% over the same period.

Despite these incredible gains, one investor, known by the pseudonym The Alpha Analyst, believes that neither company has reached “set-it-and-forget-it” status.

“Looking ahead, exposure to this AI CPU theme needs to be guarded, as risks of the narrative outrunning fundamentals are high for both AMD and Intel,” explains the investor.

It’s not that the narrative-led rally is irrational, per se, Alpha Analyst is quick to note. After all, the CPU demand is clearly an ongoing trend. However, the investor is worried that revisions and re-ratings could be on the horizon for each, especially as execution ramps up.

Alpha Analyst argues that AMD has a safer baseline. Not only does its GPU business already give it a foot in the AI bonanza, but its earnings revisions and valuation risks are lower than Intel’s. In that sense, AMD offers a natural hedge while “riding the CPU thesis.”

For Alpha Analyst, execution is where push comes to shove. Though Intel might have a higher ceiling, the investor believes that the execution risks are a bit higher.

“I think a better stance at overheated levels is to stay with the lower floor of AMD while retaining the CPU optionality,” concludes Alpha Analyst, who’s calling AMD a Buy and INTC a Sell. (To watch The Alpha Analyst’s track record, click here)

Wall Street appears to agree with at least part of that thinking. AMD enjoys a Strong Buy consensus rating backed by 28 Buys against 8 Holds. (See AMD stock forecast)

Intel’s picture looks considerably less appealing by comparison. While the Street is not as bearish as Alpha Analyst, confidence in the stock remains limited, with INTC holding only a consensus Hold (i.e., Neutral) rating backed by 11 Buys, 24 Holds, and 3 Sells. (See INTC stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.