Well, that went pretty well after all. Heading into its Q1 readout on Tuesday, Advanced Micro Devices (NASDAQ:AMD) shares were on a tear, so a lot was riding on the Q1 report for the stock to keep up the momentum. In the end, the worries were misplaced as the semi giant delivered an exceptional readout and guide, with the market reacting accordingly. To wit, shares are up ~19% in Wednesday’s trading.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Revenue climbed 37.8% year-over-year to $10.25 billion, topping Wall Street expectations by $330 million. The Data Center segment once again did much of the heavy lifting, with revenue climbing 57% to $5.78 billion as demand remained strong for MI-series AI accelerators alongside Instinct and EPYC processors. That exceeded analyst expectations of $5.61 billion. Adjusted gross margin expanded 170 basis points y/y to 55%, while adjusted EPS landed at $1.37, beating consensus estimates by $0.08.

And perhaps most importantly for a stock, AMD’s outlook also came in ahead of expectations. For Q2, the company guided for revenue of $11.2 billion, plus or minus $300 million, well above the Street’s $10.52 billion forecast. At the midpoint, that points to approximately 46% year-over-year growth and around 9% sequential growth. AMD also expects adjusted gross margin to improve further to 56%.

On the earnings call, CEO Dr. Lisa Su noted that AMD is experiencing a “meaningful” acceleration in server CPU demand. That, says Jefferies analyst Blayne Curtis, was the “clear highlight,” given the company doubled the TAM to $120 billion by 2030, reflecting 35% annual growth, driven by “agentic AI tailwinds.” “The Server CPU TAM raise was notable, reflecting the structural uplift from agentic AI that is viewed as largely incremental to the GPU TAM and AMD will expand on this further at their AI day in July,” Curtis, who ranks among the top 1% of Street stock experts, went on to say.

Server CPU momentum remains strong, with the guide pointing to more than 70% y/y revenue growth in Q2, and Curtis thinks AMD appears well-positioned to gain additional share through Venice in the second half of 2026 and beyond. The company also noted relatively weaker demand for older SKUs compared with what Intel has indicated, as it continues to ramp newer products.

As for GPUs, MI450/Helios remains on course for a ramp in 2H26, with initial volume expected in Q3 followed by a more significant ramp in Q4. Importantly, the lead customer’s forecasts have now exceeded their original expectations, while the broader customer pipeline continues to expand. AMD also signaled confidence in exceeding its long-term data center AI CAGR target of more than 80% over the next several years.

Now, says Curtis, it’s all about GPU execution. “The Server CPU narrative was strengthened but execution through the MI450/Helios ramp remains the key focus,” the 5-star analyst summed up.

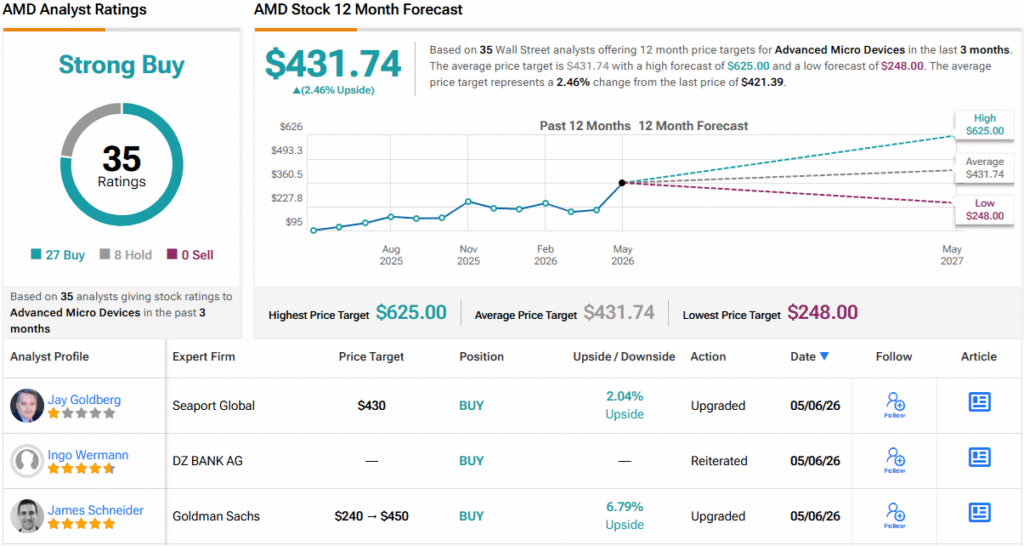

Bottom line, Curtis assigns AMD a Buy rating, while his price target goes from $300 to $415, although today’s surge has now taken the shares beyond that objective. (To watch Curtis’s track record, click here)

26 of Curtis’s colleagues join him in the bull camp, while an additional 8 Holds can’t detract from a Strong Buy consensus view. Still, with AMD’s big surge following the earnings report, the average price target of $431.74 now suggests a modest 2.5% upside from current levels. (See AMD stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.